- Active fixtures post Dussehra holidays lift Australia-India rates

- Near-term outlook remains uncertain on rising bunker costs

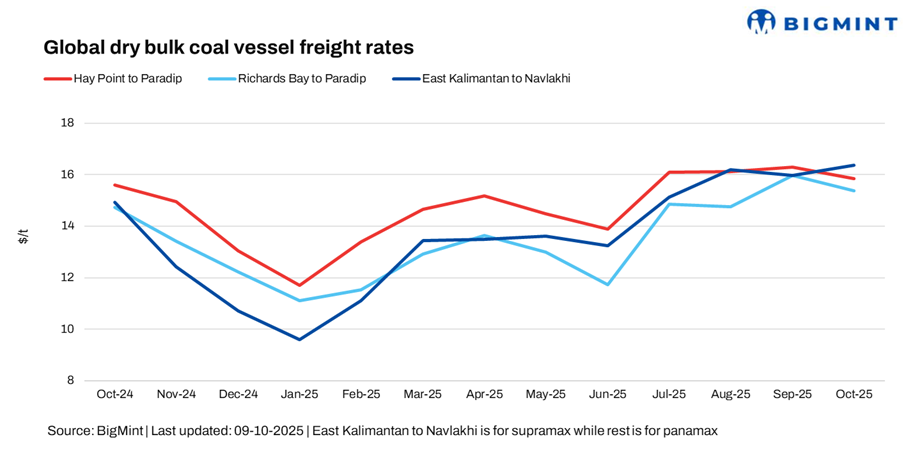

Dry bulk coal freight rates continued to display a mixed trend this week. The Indonesia-India and South Africa-India routes witnessed a notable decline, largely due to a lack of fresh fixtures and subdued market activity.

In contrast, the Australia-India route emerged as the only active lane, supported by renewed buying interest from Indian steelmakers resuming spot inquiries and fixtures after the holiday break. Overall market sentiment remained cautious, with selective chartering activity and limited cargo flow shaping freight movements across key routes.

A source said, “Australia-China Panamax freight rates strengthened this week, supported by steady market sentiment and tight vessel availability, particularly for the first half of October. Although fresh cargo volumes remained limited, market participants grew more optimistic about near-term prospects as Indian holidays drew to a close. Adding to the positive tone, freight derivative rates edged higher during Asian trading hours, while bunker prices continued to rise on a day-to-day basis, further underpinning market sentiment.

On the contrary, South Africa-India dry bulk coal freight rates declined this week, reflecting weak market activity and a lack of fresh fixtures. However, with deals getting concluded this week, we may see fixtures in the coming week that may support freight rates.

Following a similar trend, Indonesia-India Supramax freight rates came under pressure amid limited cargo availability, which kept market levels subdued. In the Indian Ocean, rates weakened further as vessel supply outpaced demand, while overall trading activity remained sluggish.

“Trading activity remained muted on the Indonesia-India coal route, despite Indian market participants returning after the festive holidays,” a shipbroker noted.

Meanwhile, rising bunker prices added additional pressure on the freight market, increasing voyage costs and squeezing charterers’ margins. The consistent upward movement in fuel prices made shipowners more cautious in fixing new deals, while charterers remained hesitant amid elevated operating expenses. This imbalance between rising costs and subdued demand further contributed to the overall softness and uncertainty in the dry bulk freight market.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up by around 0.37/dry metric tonne (dmt) to $16.03/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route fell significantly by $1.3/dmt w-o-w to $14.72/dmt, hitting around 2-month low.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $16.25/dmt, a w-o-w decrease of $0.22/dmt.

Market highlights

- Baltic index exhibits mixed trend w-o-w: The Baltic Exchange’s main dry bulk index recovered by 54 points w-o-w to 1,963 on 08 October 2025. The Panamax segment increased marginally by 10 points w-o-w to 1,695, while the Supramax segment fell 45 points w-o-w to around 1,411. Panamax rates rose on improved vessel demand and stronger cargo activity, while Supramax freights fell amid oversupply and limited fixtures.

- Brent crude oil futures rise w-o-w: Brent crude oil futures increased by around $1.43/barrel (bbl) w-o-w to $65.47/bbl. Brent crude oil futures climbed this week as OPEC+ announced a smaller-than-expected output hike for November, easing oversupply concerns. Support also came from geopolitical risks to Russian supply and strong U.S. demand, though gains were capped by a rise in U.S. crude inventories.

Outlook

The near-term outlook for dry bulk coal freight rates to India from key origins such as Australia, South Africa, and Indonesia remains mixed. The Australia-India route is likely to stay supported amid steady demand and tight vessel availability, particularly for Panamax segments, as Indian buyers continue post-holiday procurement. However, upside potential could be limited by restricted fresh cargo inflow and rising bunker costs.

In contrast, Indonesia-India routes may face continued pressure due to weak fixture activity and an oversupply of tonnage in the Indian Ocean. Limited demand for prompt cargoes and cautious charterer sentiment could keep rates subdued in the short term. Overall, freight market movement is expected to stay range-bound, with selective improvements on active routes while others remain weighed down by muted trade and cost pressures.

Leave a Reply