- Domestic Tense scrap softens amid improved availability

- ADC12 alloyed ingot prices stable across the country

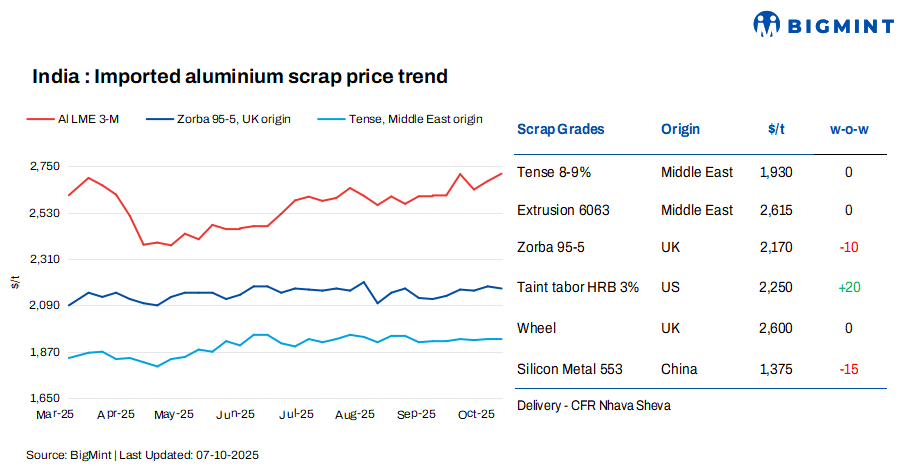

India’s imported aluminium scrap prices remained rangebound w-o-w, despite positive trends on London Metal Exchange (LME) benchmarks. BigMint assessed UAE-origin Tense scrap at $1,930/tonne (t), stable w-o-w, while US-origin Taint Tabor HRB (2-3%) rose by $20/t to $2,250/t.

UK-origin Zorba 95/5 decreased by $10/t w-o-w, UAE Extrusion 6063 and UK-origin Wheel both remained stable w-o-w.

LME prices increase w-o-w; inventories decline

At the time of reporting, LME aluminium prices stood at $2,725/t, up by around $50/t as compared to $2,675/t last week.

Meanwhile, aluminium inventories at registered warehouses posted a notable decline of 8,300 t to 507,300 t from 515,600 t in the previous week.

LME aluminium prices inched higher, supported by ongoing supply-side risks amid uneven demand. China’s annual production cap of 45 mnt continues to restrict output growth, while supply concerns deepened after Guinea Alumina lost its mining licences, threatening ore availability for Emirates Global Aluminium. LME aluminium inventories also declined sharply by nearly 100,000 t to 375,000 t in early September. Although demand softened during the Chinese holidays, persistent supply constraints have kept aluminium prices relatively firm.

Market insights

Imported aluminium market conditions remained largely unchanged from last week, with no major price increases reported from shippers. Trading activity stayed muted, as buyers showed limited interest at prevailing offer levels and continued to place lower bids. No major deals were concluded, and buying from India has slowed noticeably ahead of the Diwali holidays.

Imported aluminium scrap offers largely mirrored the rangebound LME trend despite prices rising to $2,720-2,730/t. UAE-origin Taint Tabor was offered around $2,330-2,350/t CFR Mundra, while UK-origin Wheels were heard near $2,610/t CFR Mundra.

Similarly, US-origin Taint Tabor HRB (3%) offers were reported at $2,240-2,250/t, with sellers unwilling to go below $2,220/t amid firm LME support.

Domestic Tense scrap prices edged slightly lower to INR 191,000-192,000/t across northern and southern India, pressured by improved supply as scrap yards liquidated inventories before the quarter-end.

In the extrusion segment, prices softened by INR 2,000/t to INR 215,000/t ex-Delhi, though steady demand from the automotive and construction sectors offered some support. However, ongoing BIS inspections at extrusion units kept buyers cautious about large-volume commitments.

India’s aluminium ADC12 alloy ingot prices remained stable w-o-w at INR 228,000/t in Delhi and INR 230,000/t in Chennai, according to BigMint’s benchmark assessments.

Silicon price trends

According to BigMint’s assessment, silicon 553 prices from China declined by $15/t w-o-w to $1,380/t CFR Mundra, due to softening demand amid the ongoing Chinese holidays, along with improved availability from Chinese producers.

Outlook

Sentiment in the imported and domestic aluminium markets is expected to remain cautious in the near term. While LME-led import prices are likely to stay firm, domestic scrap prices may see limited upside due to ample inventory and subdued buying ahead of Diwali. Post-holiday seasonal demand could provide some support, but overall market momentum is expected to remain moderate.

Leave a Reply