- Chattogram port ship recycling dropped to 14,861 LDT this week

- Construction sector sluggish; mills running below 50% capacity

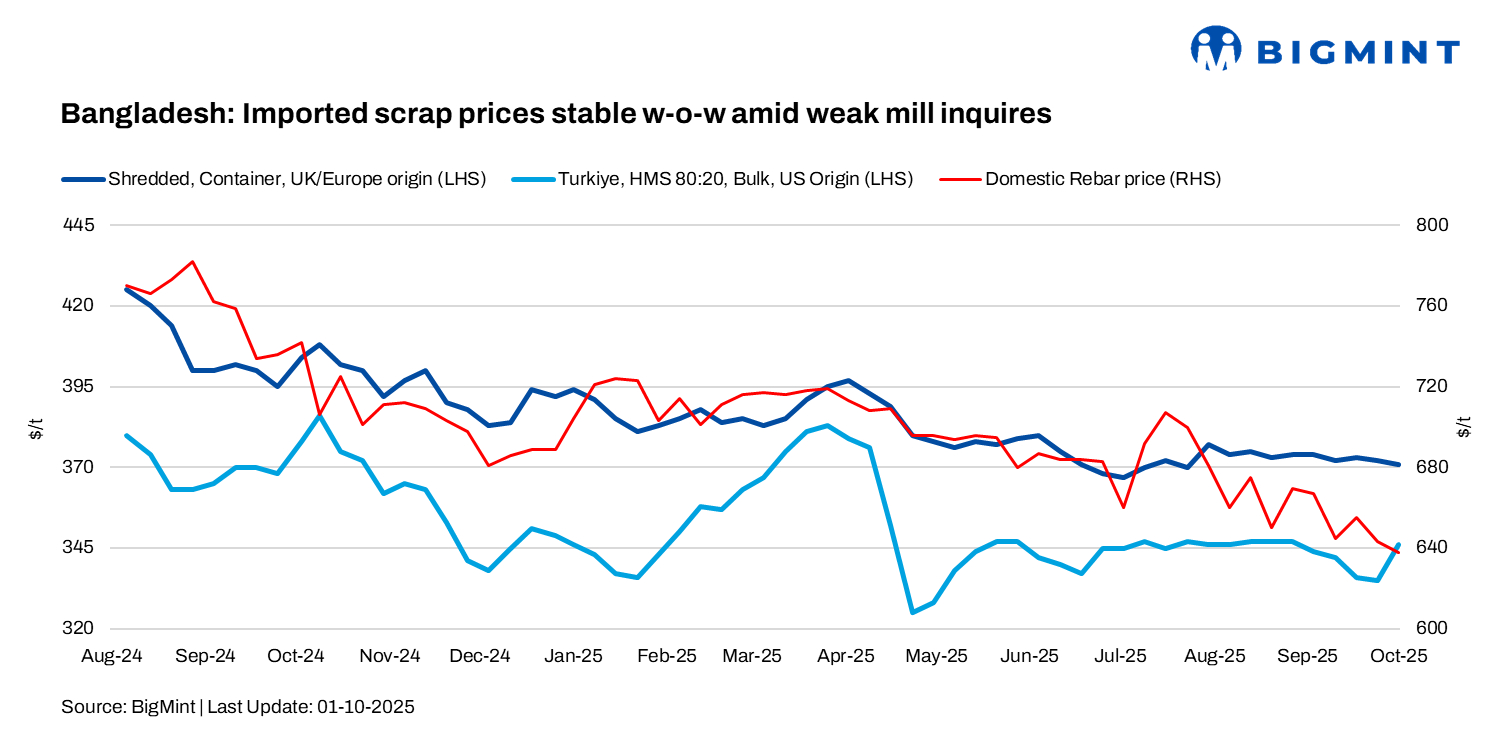

Bangladesh’s imported ferrous scrap prices witnessed a largely stable trend in the last seven days, with limited buying interest from major mills.

Overall sentiment is weak–construction is slow, the economy is struggling, and mills are operating below 50% capacity. No new projects are driving demand, and investors are holding back.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched down w-o-w to $350/t.

- European-origin containerised shredded inched down by $1/t w-o-w to $371/t.

- Japanese-origin H2 bulk prices stood at $342/t, stable w-o-w.

- US-sourced HMS (80:20) bulk prices dropped by $1/t to $351/t.

“Bangladesh’s scrap market remains dull as mills stocked up in early September, so there’s little fresh buying. US HMS 80:20 bulk is offered at $355/t CFR, with bids around $345/t and recent deals settled near $352/t. Some Japanese bulk was booked mid-last month. On the container side, buyers want Malaysia PNS at $370-375/t, but sellers are asking $10/t higher,” said a major Chattogram-based importer.

“PNS from Singapore is being offered at $378/t, with bids around $370/t. Buyers are looking for Malaysia PNS at $370-372/t, while offers hover near $380/t. HMS 80:20 from Australia is trading at $340-342/t, but interest remains low. Overall sentiment is weak as the construction sector is sluggish and mills are operating below capacity,” said a Dhaka-based market insider.

“Bangladesh’s scrap and steel market remained mostly stable, but overall finished steel demand stayed weak due to a lack of new government projects. Local scrap is hovering around BDT 42,000-45,000/t ($345-370/t), while rebar prices are at BDT 74,000-75,000/t ($608-616/t) in Dhaka and BDT 78,000-80,000/t ($641-657/t) in Chattogram,” said a Chattogram-based trader.

Bangladesh’s ship recycling market remains quiet. Stagnant steel prices and a weaker BDT are limiting activity. Smaller LDT units dominate, while demand for larger Capesize and Panamax vessels is scarce, often redirected elsewhere. There are 18 HKC-compliant yards, with three more expected, but activity remains slow due to limited support and delayed upgrades. Chattogram Port received 14,861 LDT this week, down from 44,802 LDT last week.

Outlook: Bangladesh’s scrap and steel markets are expected to remain subdued as mills operate below capacity and demand is weak. Ship recycling activity is likely to stay slow, while buyers remain cautious on bulk volume imports.

Leave a Reply