- Grasberg loss, disruptions in Chile and Peru shift market into deficit

- EVs, renewables keep demand strong; prices seen near $10,200–10,500/t

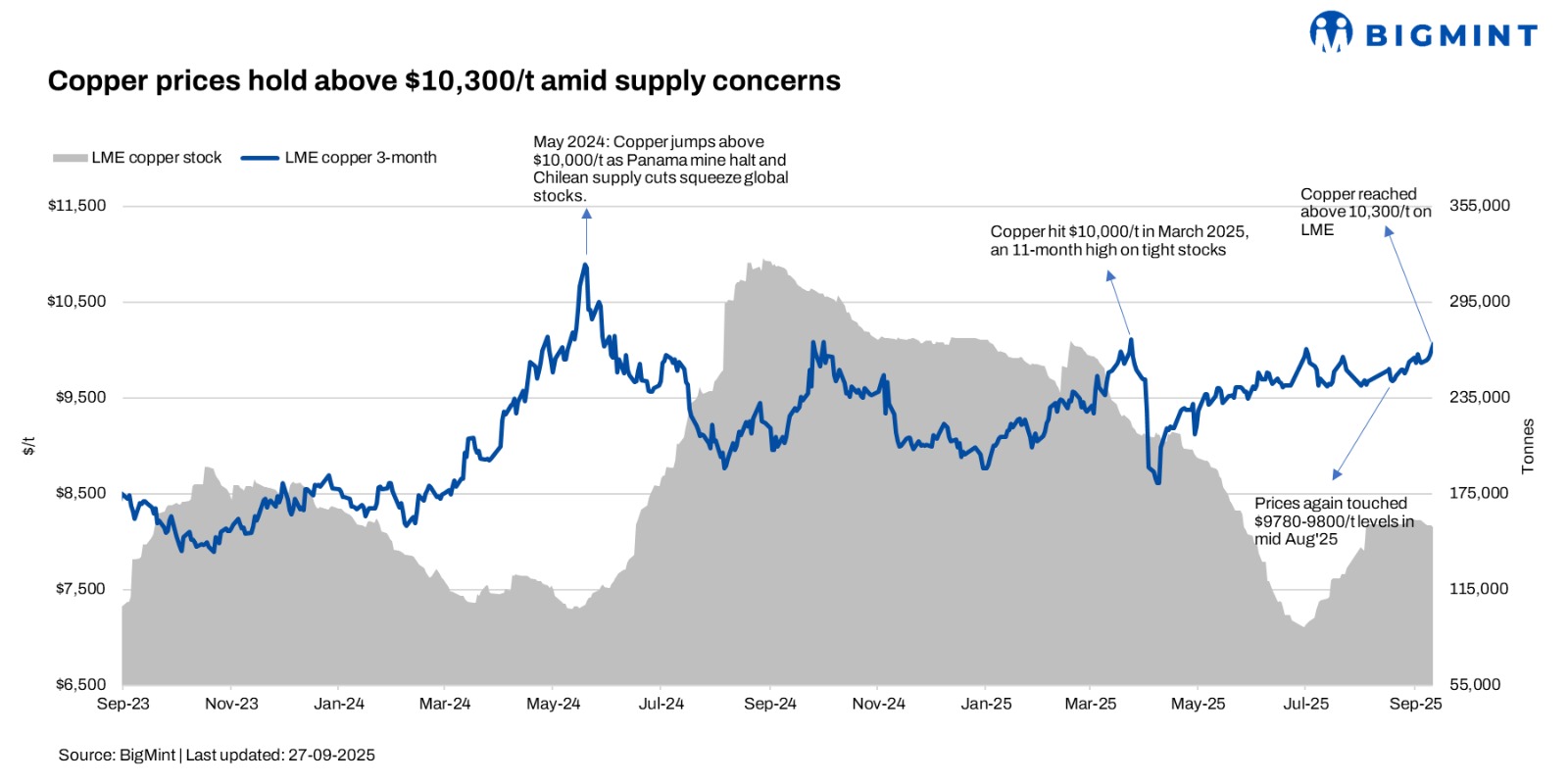

The benchmark three-month copper contract on the London Metal Exchange (LME) closed at $10,300/t on 26 September 2025, down by $300 compared to 19 September. This price movement follows a period of sharp increases earlier in September, justified by significant supply disruptions at key global copper mines, particularly the suspension of production at Freeport McMoRan’s Grasberg mine in Indonesia due to a mudflow accident. This event significantly curtailed output from one of the world’s largest copper producers, tightening global supply.

Additionally, production slowdowns in Chile and Peru due to labour strikes and regulatory restrictions have exacerbated supply deficits. On the demand side, global economic recovery, especially in the renewable energy and electric vehicle sectors that rely heavily on copper, sustained strong consumption levels. These dynamics pushed copper prices upwards during the early part of September, peaking near $10,600 per tonne.

Recent analysis from Goldman Sachs has added urgency to the supply story: the bank revised its global copper mine supply forecasts downward for both 2025 and 2026 after estimating that Grasberg may lose around 250,000-260,000 t in 2025 and another 270,000 t in 2026. The adjustment shifts the market from a projected small surplus into a deficit.

Meanwhile, India is also moving to shore up its supply of critical minerals, including copper, through partnerships with countries like Chile, Peru, and Argentina. This is part of a broader strategy to mitigate supply chain disruption risks amid growing demand for EVs, battery storage, and renewable energy systems.

Putting it all together: while $10,300/t represents a retreat from recent highs, the fundamentals remain tight. Supply continues to be under strain from multiple fronts, and demand remains robust across green tech and infrastructure. Unless one of these disruption points eases — like Grasberg returning to full output or regulatory clarity in Chile/Peru — copper is likely to remain volatile, with risk skewed toward further upside.

Price outlook: volatile, with upward bias

Copper prices may face short-term softness in Q4CY’25 due to seasonal demand swings, inventory adjustments, or macroeconomic headwinds. However, consensus among some analysts (e.g. Goldman Sachs) is that the market may shift further into a deficit, pushing price targets toward the $10,200-10,500/t range toward end-2025.

Leave a Reply