- Australian exports up 22% on stronger vessel activity, steady port throughput

- South African, Colombian shipments fall due to logistics, demand issues

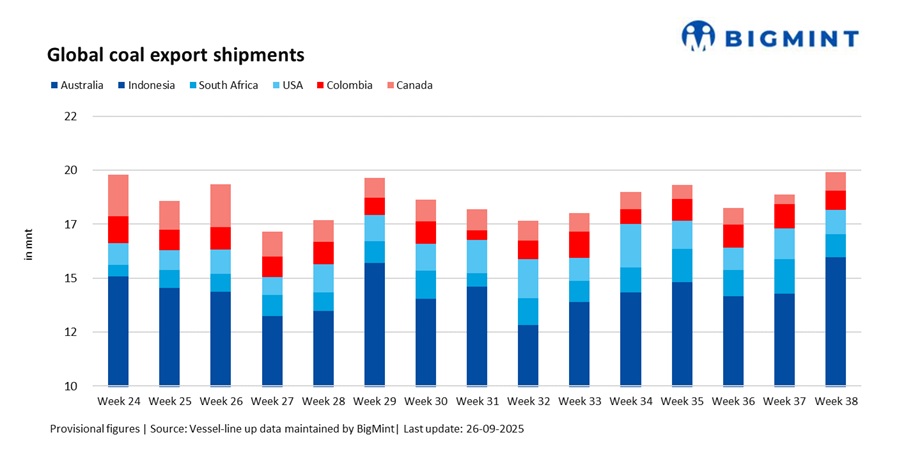

Global seaborne coal exports rose 5.5% w-o-w to 19.54 million tonnes (mnt) in week 38 (13-19 September 2025) from 18.51 mnt in week 37, according to BigMint’s vessel line-up data. The increase was driven by robust shipments from Australia, Indonesia, and Canada, which more than offset declines from the US, South Africa, and Colombia.

The rebound reflected improved vessel activity in Australia, steady loadings in Indonesia, and opportunistic Canadian fixtures. However, muted South African flows underscored ongoing logistical challenges, while weaker procurement from selective markets weighed on US and Colombian shipments. Tepid Indian demand amid elevated landed costs also capped upside momentum.

Country-wise trends

Indonesia: Coal exports from Indonesia rose 2.3% w-o-w to 7.88 mnt in week 38 from 7.70 mnt in week 37, supported by favourable weather and steady vessel scheduling. Loadings were led by Taboneo (1.53 mnt), Samarinda (1.19 mnt), and Bunati (1.10 mnt), reflecting consistent port activity after earlier monsoon-related disruptions.

On the demand side, China (2.16 mnt) and India (1.81 mnt) remained the largest buyers. While Chinese procurement stayed firm amid stable power sector demand, Indian volumes were constrained by elevated landed costs and muted industrial buying, which capped upside despite overall stable flows.

Australia: Coal shipments surged 22.7% w-o-w to 7.86 mnt in week 38 from 6.40 mnt in week 37, rebounding strongly after two consecutive weeks of decline. Loadings were led by Newcastle (3.47 mnt), DBCT (1.34 mnt), and Hay Point (1.18 mnt), as smoother vessel turnaround and improved port scheduling boosted throughput.

On the demand side, Japan (2.15 mnt) and China (1.44 mnt) maintained steady intake, while Indian buying stayed muted due to higher landed costs and cautious procurement. Market participants attributed the rebound mainly to operational improvements and a catch-up in vessel activity, though they cautioned that sustaining the momentum will depend on consistent demand, particularly from Asian utilities.

United States: Exports declined 19.1% w-o-w to 1.10 mnt in week 38 from 1.36 mnt in week 37, as weaker overseas demand weighed on shipments. Loadings were led by Baltimore (0.35 mnt), New Orleans (0.28 mnt), and Norfolk (0.27 mnt).

On the demand side, India (0.53 mnt) remained the largest buyer, while European intake was subdued, with Germany and The Netherlands each taking 0.08 mnt. Market participants noted that elevated freight costs and cautious industrial demand in both India and Europe limited fresh bookings, while selective procurement strategies among utilities further dampened volumes.

South Africa: Shipments slumped 34.1% w-o-w to 1.01 mnt in week 38 from 1.54 mnt in week 37, with all volumes routed through RBCT. The sharp drop was primarily driven by reduced railings and weaker Indian offtake, which fell to 0.43 mnt.

Market participants highlighted that recurring rail bottlenecks and port inefficiencies continued to disrupt supply chains, limiting the consistency of exports. Even though opportunistic demand occasionally supports flows, structural logistics challenges remain the key obstacle to sustaining higher shipment levels.

Colombia: Colombian coal exports fell 22.8% w-o-w to 0.85 mnt in week 38 from 1.10 mnt in week 37, as softer demand weighed on shipments. Loadings were led by Puerto Nuevo (0.67 mnt) and Puerto Bolivar (0.16 mnt), but European utilities cut back purchases amid elevated freight costs and cautious buying strategies.

On the demand side, South Korea (0.18 mnt) emerged as the largest importer, followed by Spain (0.17 mnt) and The Netherlands (0.16 mnt). Market participants noted that with European buyers scaling back and freight economics remaining unfavorable, Colombian exports are likely to stay volatile unless stronger regional demand emerges.

Canada: Canada’s coal exports more than doubled, rising 105% w-o-w to 0.83 mnt in week 38 from 0.41 mnt in week 37, marking the strongest rebound among major suppliers. Loadings were led by Roberts Bank (0.43 mnt) and Prince Rupert (0.32 mnt), as improved vessel arrivals and smoother port operations supported higher shipments.

Japan (0.60 mnt) remained the dominant buyer, underscoring its reliance on Canadian coal. However, market participants cautioned that exports remain highly vulnerable to supply chain disruptions, with operational reliability continuing to dictate weekly fluctuations.

Freight trends: Dry bulk coal freights showed mixed movements during the week, with rates on Indonesia-India routes softening while South Africa-India and Australia-India remained firm. Ample vessel availability, muted Indian demand, and cautious procurement strategies kept overall trade activity subdued.

Elevated landed costs discouraged aggressive buying, particularly in India, capping upside for exporters even as Australian and Indonesian flows remained steady.

Outlook

Global coal exports are expected to remain range-bound in the near term. Indonesian shipments should stay steady on stable weather and port activity, while Australian exports may continue to benefit from improved vessel flows.

South African volumes hinge on rail and port reliability, whereas US and Colombian shipments remain under pressure from selective demand. With freight sentiment mixed and Indian buyers showing resistance to higher landed costs, trade momentum is likely to stay cautious in the coming weeks.

Leave a Reply