- Exports to EU up 32% on brisk restocking ahead of CBAM

- Semis exports increase manifold, longs up 26%

- EU initiates anti-dumping probe into CRC imports

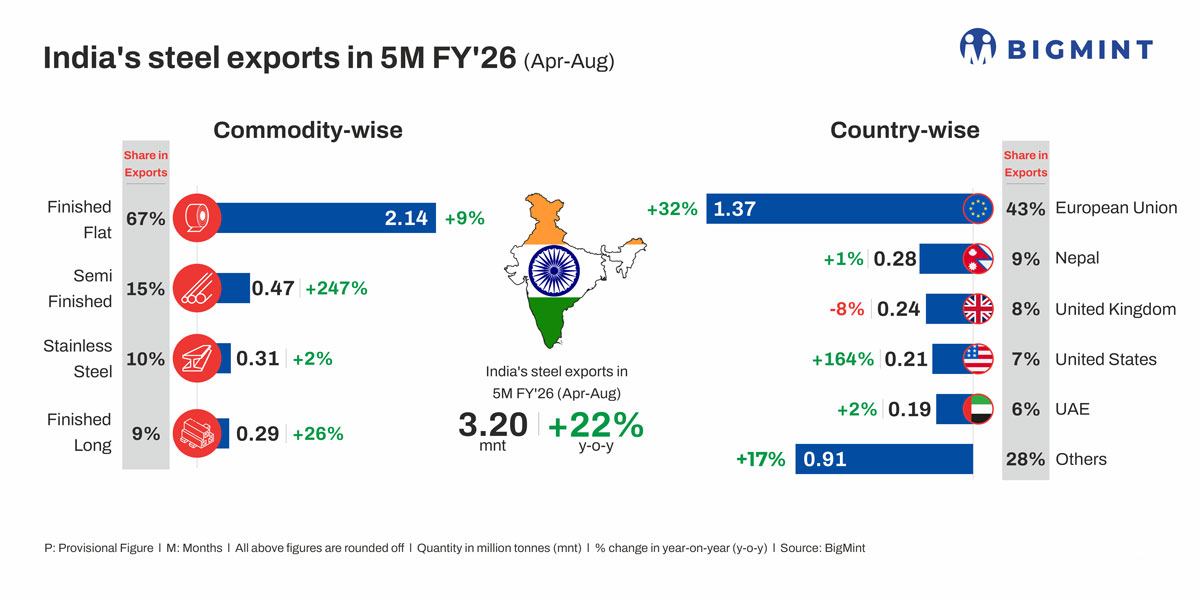

Morning Brief: India’s steel (including stainless steel) exports climbed up by a robust 22% y-o-y in April-August 2025 (5MFY’26) to 3.20 million tonnes (mnt), as per provisional data maintained with BigMint. The rise comes on the back of a 32% increase in exports to the EU, as Indian mills pushed to complete their quotas ahead of the CBAM implementation in January 2026.

Commodity-wise exports

India’s finished flats (carbon steel) exports rose 9% y-o-y to 2.14 mnt.

Among sub-commodities, hot-rolled coil (HRC)/plate exports increased by 12% y-o-y to 0.67 mnt in 5MFY’26. Volumes remain moderate, considering that they are lower by over 50% compared to 2023. Pipes and tubes exports were also higher by 26% at 0.80 mnt. These two were the only flats categories to register an increase.

Galvanised steel shipments were lower by a modest 6% y-o-y at 0.45 mnt, while CRC exports dropped by 10% to 0.19 mnt.

India’s semi-finished steel exports surged manifold to 0.47 mnt in 5MFY’26. Longs witnessed a 26% uptick to 0.29 mnt, led by a notable uptick in wire rod exports.

Total stainless steel exports edged up by 2% to 0.30 mnt, remaining largely stable.

Country-wise exports

The EU was the largest export destination for India, receiving 1.37 mnt, up by a robust 32%. Exports to Nepal edged up by 1% at 0.28 mnt, while those to the UAE were at 0.19 mnt, up 2%. Shipments to the UK dropped by 8% to 0.24 mnt, and volumes to Vietnam and Saudi Arabia plunged by 36% and 85% to minor levels.

Factors influencing India’s steel exports

CBAM anxieties push EU importers to ramp up procurement: With the January 2026 implementation deadline for the Carbon Border Adjustment Mechanism (CBAM) fast approaching, uncertainty regarding future steel pricing and procurement has intensified. As a result, EU-based buyers have been stocking up on lower-priced imports before the expected increase in costs due to additional tax liabilities.

With regard to HRCs, due to the prevailing uncertainty, it is heard that importers have been booking selectively, for cargo arriving by October. Indian steelmakers, concerned about the harm to their price competitiveness, are also trying to secure bookings actively.

Notably, as per EU customs data, Indian mills shipped 54,000 tonnes (t) of “non-alloyed and other alloyed hot-rolled sheets and strips” in Q1FY’26, while in Q2FY’26, till 26 August, 53,000 t have been shipped, with one month left for the quarter to end.

HRC exports to ME remain on pause: Indian mills have been reluctant to offer HRC exports to the Middle East since March, leading to a sharp decline in volumes to Saudi Arabia.

While HRC offers resumed in mid-August at $530-535/t CFR UAE against China’s $515/t, offers remained absent in the subsequent weeks. While rising Chinese prices prompted this brief return, overall trade has remained subdued due to the summer season slowdown and China’s market dominance in the region. Chinese exports to the UAE increased by 10% y-o-y, while volumes to Saudi Arabia surged 24%.

Indian steelmakers were also unwilling to match competitive Chinese levels amid better realisations at home.

Outlook

Exports to the EU may moderate after October. Overall, the market has adopted a wait-and-watch stance ahead of the CBAM implementation. While the EU-India trade deal offers a glimmer of hope, steel remains a key sticking point for both parties, due in part to CBAM.

Indian exporters also resumed offers to Vietnam in September, with a 30,000-t deal heard. However, this may end up being an isolated occurrence, as demand remains tepid. Another hurdle is the EU’s initiation of an anti-dumping probe into cold-rolled flat steel imports from five nations: India, Japan, Taiwan, Turkiye, and Vietnam.

Leave a Reply