- Power sector emissions dip in H1CY’25, for 2nd time in 50 years

- Clean energy sources to meet entire demand growth over 2025-30

- Non-fossil capacity expected to rise to 482 GW from 243 GW in end-Jun,25

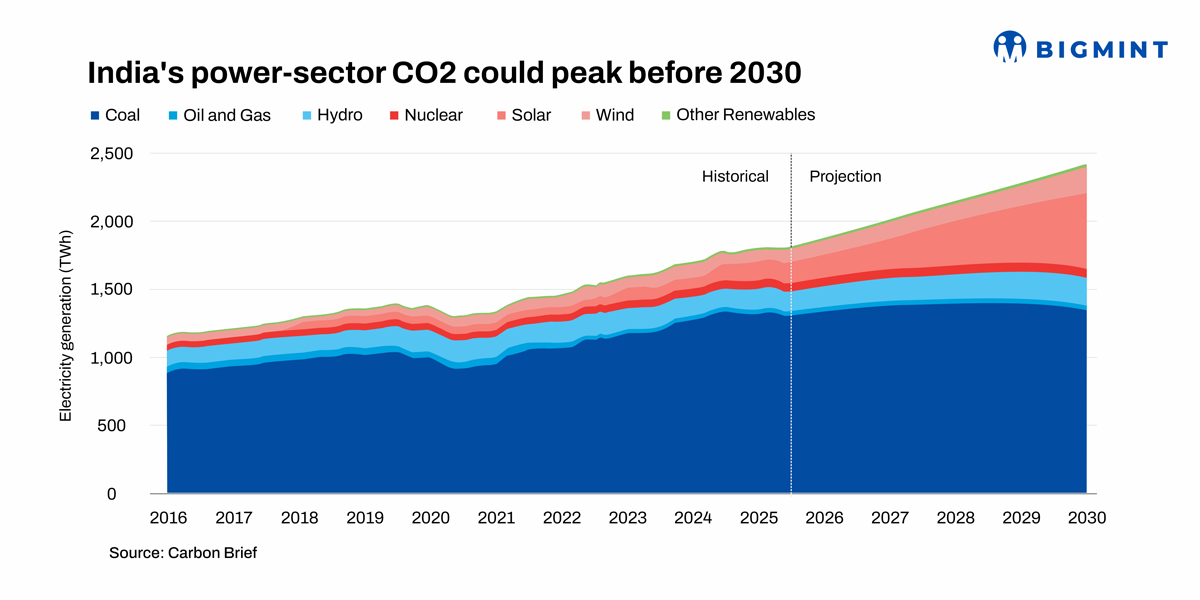

Morning Brief: Carbon dioxide emissions from India’s power sector are set to peak by 2030, suggests Carbon Brief in a recent analysis, drawing from NITI Aayog, Central Electricity Authority (CEA), and Centre for Research in Energy and Clean Air (CREA) data.

Power sector emissions dip in H1CY’25

The power sector is the primary contributor to India’s overall emissions growth, responsible for half of its recent increase. However, emissions from the power sector edged down by 1% y-o-y in January-June 2025, after consistently growing 10% per year during 2021-23. This is the second such drop in around 50 years.

In contrast, emissions from coal consumption in cement and steel production rose by 10% and 7%, respectively. Coal usage outside of these sectors fell 2% y-o-y.

This dip comes amid a fall in fossil fuel power generation in the first half of 2025. While total power generation climbed up by 9 terawatt hours (TWh) y-o-y, fossil power generation decreased by 29TWh. Conversely, power generation via solar grew 17TWh, by wind 9 TWh, by hydropower 9 TWh, and by nuclear 3 TWh.

Further downtrend to be seen by 2030

By 2030, growth in non-fossil power generation will outpace overall demand growth. Parallelly, power generation from fossil fuels would moderate.

However, the recent downtrend is unlikely to consolidate immediately, given that the country is expected to see substantial additions in new coal-fired generating capacity (12.8 GW announced in H1CY’25, 80-100 GW planned by 2030-32).

In fact, so far, clean energy additions have been far lower than the growth in total electricity demand, enabling fossil-fuel demand and emissions to rise.

However, the turning point has arrived. Over 2025-30, growth in power demand, averaging 6% per year, will be covered entirely from clean sources. In FY’30, the share of non-fossil power generation is estimated to rise to 44% against 25% in FY’25.

Lower costs of solar and wind power generation, enabled by technological advancements, will help boost their contributions to meeting peak energy loads. Recent steep reductions in the cost of solar power with integrated battery storage will be a key factor.

Renewable capacity additions picking up

However, the expected moderation hinges on the timely completion of contracted projects. Clean energy growth needs to be maintained or accelerated beyond 2030, and demand growth needs to align with government projections.

In 2021, India aimed to achieve 500 GW of non-fossil power generation capacity by 2030. In July 2025, India’s non-fossil power capacity surpassed 50% of its total, five years ahead of schedule.

Government data shows that as of April 2025, there was 234GW of renewable capacity in the pipeline. This comprises 169 GW of already awarded contracts, of which 145 GW is under construction and an additional 65GW put out to tender. Additionally, 5.2 GW of new nuclear capacity is under construction.

Total non-fossil capacity is expected to rise to 482 GW from 243 GW in June-end, if all these projects commence operations by 2030. This would leave only 18 GW to be filled with new projects.

Outlook

India is likely to easily achieve its previous nationally determined contribution (NDC) of reducing its economy’s emissions intensity to 45% lower than 2005 levels by 2030. Thus, this goal is unlikely to count as an active effort to achieve meaningful emissions reductions.

Additionally, India is yet to announce its NDC for 2035 under the Paris Agreement despite the end-September 2025 deadline nearing. This has cast doubt on its future emissions path up to its 2070 net-zero goal.

The country also needs to slash carbon emissions from the industrial and transport industries to peak its emissions overall.

Leave a Reply