- Softer vessel activity, slower clearances hit Australian exports

- Outlook remains cautious amid subdued Indian demand

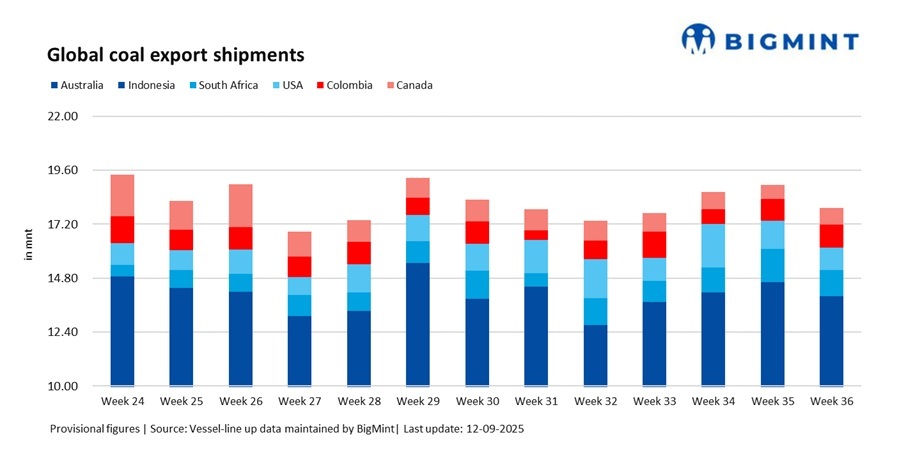

Global seaborne coal exports declined 5.1% w-o-w to 17.93 million tonnes (mnt) in Week 36 (30 August-5 September 2025) from 18.94 mnt in Week 35, according to BigMint’s vessel line-up data. The fall was driven mainly by weaker shipments from Australia and South Africa, which outweighed modest gains from Indonesia, Colombia, and Canada.

The downturn reflected softer vessel activity in Australia and renewed rail bottlenecks in South Africa, even as Indonesian flows edged higher. On the demand side, Chinese restocking continued steadily, but Indian utilities kept imports subdued, relying on sufficient domestic coal inventories. European demand was selective, with a tilt towards Colombian and South African cargoes.

Country-wise trends

Australia: Coal exports dropped 10% w-o-w to 6.79 mnt in Week 36 from 7.55 mnt in Week 35. Loadings were led by Newcastle (3.01 mnt), followed by Gladstone (1.09 mnt), Abbot Point (1.02 mnt) and DBCT (0.87 mnt). The decline reflected reduced vessel activity and slower clearances after a strong August. Market sources noted that heavy rains and flooding in New South Wales disrupted coal flows to the Port of Newcastle, creating vessel backlogs and contributing to the decline in shipments.

On the demand side, Japan emerged as the top buyer with 1.76 mnt, followed by China at 1.42 mnt. Together, these two markets provided a buffer against weaker Indian buying, which weighed on overall shipments.

Indonesia: Shipments edged up 1.8% w-o-w to 7.20 mnt in Week 36 from 7.07 mnt in Week 35. Loadings were led by Samarinda (1.59 mnt), followed by Taboneo (1.43 mnt) and Bunati (1.04 mnt), with other smaller ports contributing the balance. Despite ongoing monsoon-related constraints, overall flows held steady.

On the demand side, India remained the largest buyer at 1.85 mnt, followed by China at 1.71 mnt and South Korea at 0.54 mnt. Strong interest from these core Asian buyers helped Indonesia maintain export stability, although sustained gains were still capped by weather disruptions and logistical constraints.

South Africa: Exports fell sharply by 21% w-o-w to 1.16 mnt in Week 36 from 1.49 mnt in Week 35. All shipments were handled through Richards Bay Coal Terminal (RBCT) at 1.16 mnt, with rail bottlenecks once again restricting flows.

On the demand side, India emerged as the largest buyer at 0.59 mnt, supported by sponge iron and cement industries, while smaller volumes moved to European utilities. South Africa’s export outlook remains highly contingent on consistent railings to RBCT, which continued to face recurring disruptions.

US: Coal exports declined 14.7% w-o-w to 1.02 mnt in Week 36 from 1.24 mnt a week earlier. Loadings were concentrated at Norfolk (0.41 mnt), while New Orleans and Mobile ports handled 0.31 mnt each. Reduced transatlantic flows and softer fixture activity weighed on overall shipments.

On the demand side, India was the largest buyer at 0.25 mnt, though volumes remained subdued as Indian utilities limited imports amid healthy domestic stock levels. Persistent logistical challenges and weaker European appetite further curtailed US exports during the week.

Colombia: Coal exports rose 5.7% w-o-w to 1.01 mnt in Week 36 from 0.96 mnt a week earlier. Loadings were led by Puerto Nuevo at 0.67 mnt and Puerto Bolivar at 0.26 mnt, reflecting a steady recovery in activity compared to earlier weeks.

By shipper, the Prodeco Group contributed 0.68 mnt, while Cerrejon Mines handled 0.26 mnt, underscoring their dominant role in Colombia’s export flows. Strong demand from Brazil and European utilities helped stabilise shipments, though logistical bottlenecks and limited vessel availability continue to cap export potential.

Canada: Coal exports improved 16.6% w-o-w to 0.74 mnt in Week 36 from 0.64 mnt in Week 35. Loadings were split between Vancouver (0.41 mnt) and Roberts Bank (0.34 mnt), marking a rebound in port activity after earlier weakness.

On the demand side, China was the largest buyer at 0.41 mnt, followed by Japan (0.18 mnt) and South Korea (0.16 mnt). By shipper, Elk Valley Resources accounted for 0.41 mnt, underscoring its leading role in Canadian exports. Despite the w-o-w rise, participants noted that Canadian shipments remain volatile, constrained by logistical bottlenecks and fluctuating Asian demand.

Freight trends: Dry bulk coal freights displayed mixed movements during the week. Rates on the Australia-India route softened amid weak cargo demand and rising tonnage in the Asia-Pacific, while freights on the South Africa-India and Indonesia-India routes edged higher, supported by limited vessel availability and firmer bunker prices. Overall trading activity stayed muted, with market participants suggesting rates are likely to face pressure in the weeks ahead.

Outlook

Global coal exports are expected to remain range-bound to slightly weaker in the near term. Australian volumes may stay under pressure after the Week 36 decline, while South Africa’s performance depends on rail stability. Indonesian flows are likely to hold broadly steady, constrained by seasonal weather, while US and Canadian shipments remain volatile.

Freight sentiment is expected to remain soft-to-range-bound in the near term, with weak Indian demand and abundant vessel supply continuing to weigh on rates. While bunker costs and occasional fixtures may offer limited support, the upcoming GST revision and removal of the INR 400/tonne coal cess are likely to increase import costs. As a result, traders are expected to offload existing inventories before the policy change while limiting fresh bookings thereafter, which could further dampen India’s coal trade flows in the coming weeks.

Leave a Reply