- Demand remains weak amid high inventories, seasonal slowdown

- Festive season expected to stimulate demand, support prices

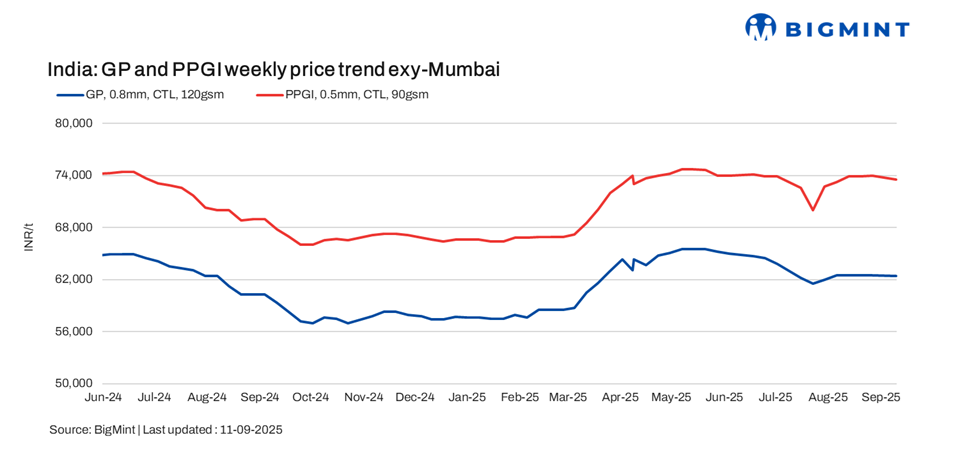

The Indian coated flat steel market continued to face headwinds this week, with prices largely under pressure due to muted demand and ample inventories. Galvanised plain (GP) prices declined by INR 700/t week-on-week (w-o-w), while PPGI saw a reduction of INR 500/t. Market participants attributed the continued softness to sluggish buying interest, contributing to the ongoing market slowdown.

The latest weekly assessment on 11 September showed GP coil (0.8 mm/CTL, 120 gsm, IS277) prices at INR 62,400/tonne(t) ($706/t) exy-Mumbai, declining by INR 700 w-o-w, with offers ranging between INR 62,000-63,000/t ($701-712/t).

Meanwhile, PPGI (0.5 mm/CTL, 90 gsm, IS14246) was assessed at INR 73,500/t ($832/t) exy-Mumbai, with offers hovering between INR 73,000-74,000/t ($826-837/t). Prices are exclusive of 18% GST. (USD 1 = INR 88.4170) (INR 1 = USD 0.0113100)

Market updates

Market sentiment across India’s coated flat steel segment remained weak this week, with subdued demand and cautious buying activity prevailing across regions. Material remains readily available, and despite recent price corrections, overall trading volumes stayed limited. Some sellers are continuing to offer at discounted levels to generate liquidity amid sluggish demand.

While inquiry levels held relatively steady, procurement has been minimal due to ongoing uncertainty around price direction. Mills are seen taking a wait-and-watch approach, as recent price hike attempts have met with limited acceptance. Looking ahead, sentiment may begin to shift with the onset of the festive season, particularly with Navratri and Diwali approaching back-to-back.

North:

The market remained dull, with weak demand prevailing across the region. Buying activity was minimal, as many participants cited the ongoing monsoon season as a dampener. Market players expect demand to improve only after the monsoon ends, with a more positive outlook for coated steel in Q4.

South:

Conditions were sluggish to stable, with limited demand across key consuming sectors. Market sentiment remains cautious, with procurement driven only by immediate need. “Participants noted that price recovery is unlikely unless domestic consumption strengthens and international sentiment — particularly from China — turns more supportive. Additionally, uncertainty ahead of upcoming elections is expected to delay major new project orders, further slowing demand.”

West:

Demand remained soft, despite attempts by mills to push through price increases. Participants attributed the weak buying interest to overall sluggish market sentiment. With overall consumption still muted, many believe current prices may not be sustainable unless market conditions improve in the coming weeks.

Outlook:

The coated flat steel market is expected to remain subdued in the near term due to weak demand, ample availability, and seasonal slowdown. Prices may remain under pressure as buying activity stays limited.

A potential recovery is anticipated post-monsoon, with demand likely to improve around the festive season (Navratri-Diwali), which could offer some support to pricing.

Leave a Reply