- Tight domestic scrap availability supports prices

- Billet demand improves but rebar market softens

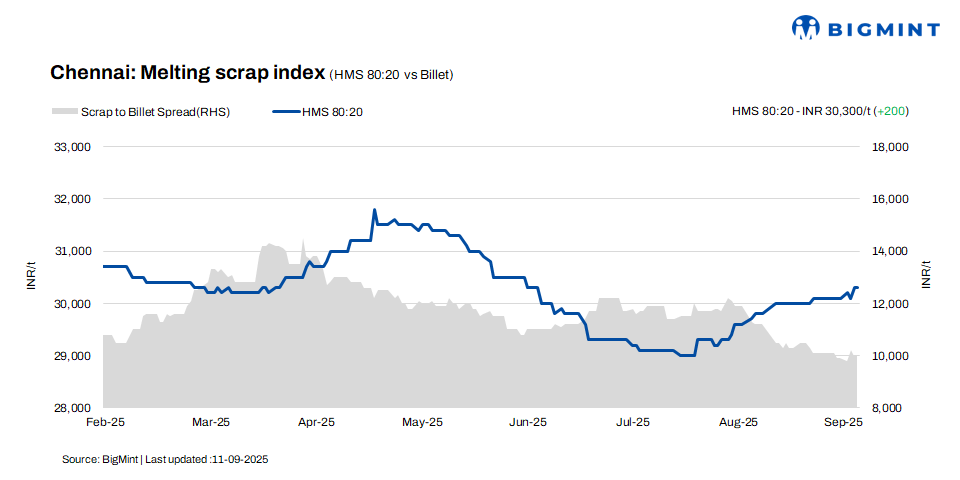

In Chennai, HMS (80:20) scrap prices saw a w-o-w increase of INR 200/t to INR 30,300/t, though prices remained stable on a d-o-d basis. Similarly, billet prices rose by INR 100/t w-o-w, stabilising at INR 40,300/t d-o-d. Conversely, Rebar prices declined by INR 700/t w-o-w, now assessed at INR 44,800/t. A similar drop of INR 200/t was noted d-o-d. The overall market sentiment indicates a mixed trend, with price stability dominating on a d-o-d basis and marginal fluctuations seen over the course of the week.

Imported, domestic price trends

According to a scrap trader, Australian shredded scrap is offered at $364-365/t, with buyers reportedly negotiating closer to $360/t. HMS 80:20 was quoted at $335-340/t, while a recent deal for HMS 60:40 was concluded at $315/t. African HMS was booked at $350/t (hand-loaded) for 500 t. Additionally, NTP bales from Malaysia, Korea, and the UK were heard booked at around $365/t CFR Chennai, with 500 t per origin, totaling 1,500 t.

In Chennai, domestic HMS (80:20) was traded at INR 30,000-30,500/t for spot deals with immediate payment, while trades on extended credit terms were slightly higher at INR 30,500-31,000/t. Overall, market activity largely remained within the INR 30,000-31,000/t band.

Buyer-supplier sentiments

According to market sources, sponge iron offers remained stable on a w-o-w basis. Mill owners increasingly preferred booking local sponge, particularly from Chennai, due to its superior quality compared to material from neighbouring states.

Billet prices showed improvement, driven by a slight uptick in demand. However, the rebar market faced a downturn in the past few days, leading to a softening in offers. Inventory levels at rebar mills were at around 10-15 days, indicating a short-term buffer but potential pressure if demand does not recover soon.

According to a local supplier, domestic HMS (80:20) prices were between INR 30,000-31,000/t, with slight variations based on payment terms. While domestic scrap availability remained tight, supporting prices, the recent slowdown in finished steel trade led to a cautious market sentiment. As a result, prices are expected to remain range-bound in the short term, though external factors such as steel demand may influence longer-term trends.

Regional comparison

In the Jalna market, western India, rebar prices decreased by INR 500/t d-o-d to INR 44,000/t, while billet prices saw a sharper drop of INR 400/t to INR 39,400/t. HMS 80:20 prices also declined by INR 100/t d-o-d to INR 31,000/t. The market experienced a slowdown in finished steel demand compared to the previous week, which impacted offers for steel materials. Buyers attempted to push scrap prices lower to control conversion costs, but suppliers showed resistance to offering material at reduced prices.

Outlook

Sources indicate that scrap prices are expected to remain range-bound in the near term, with fluctuations likely confined to INR +/-500/t. This stability is driven by ongoing uncertainty in the finished steel trade, where cautious sentiment among both buyers and sellers is curbing market activity. As a result, price volatility is expected to be limited, keeping prices within a narrow trading range.

Leave a Reply