- Container trade remains thin amid wide bid-offer gaps

- Mills wary amid tight liquidity, stagnant steel demand

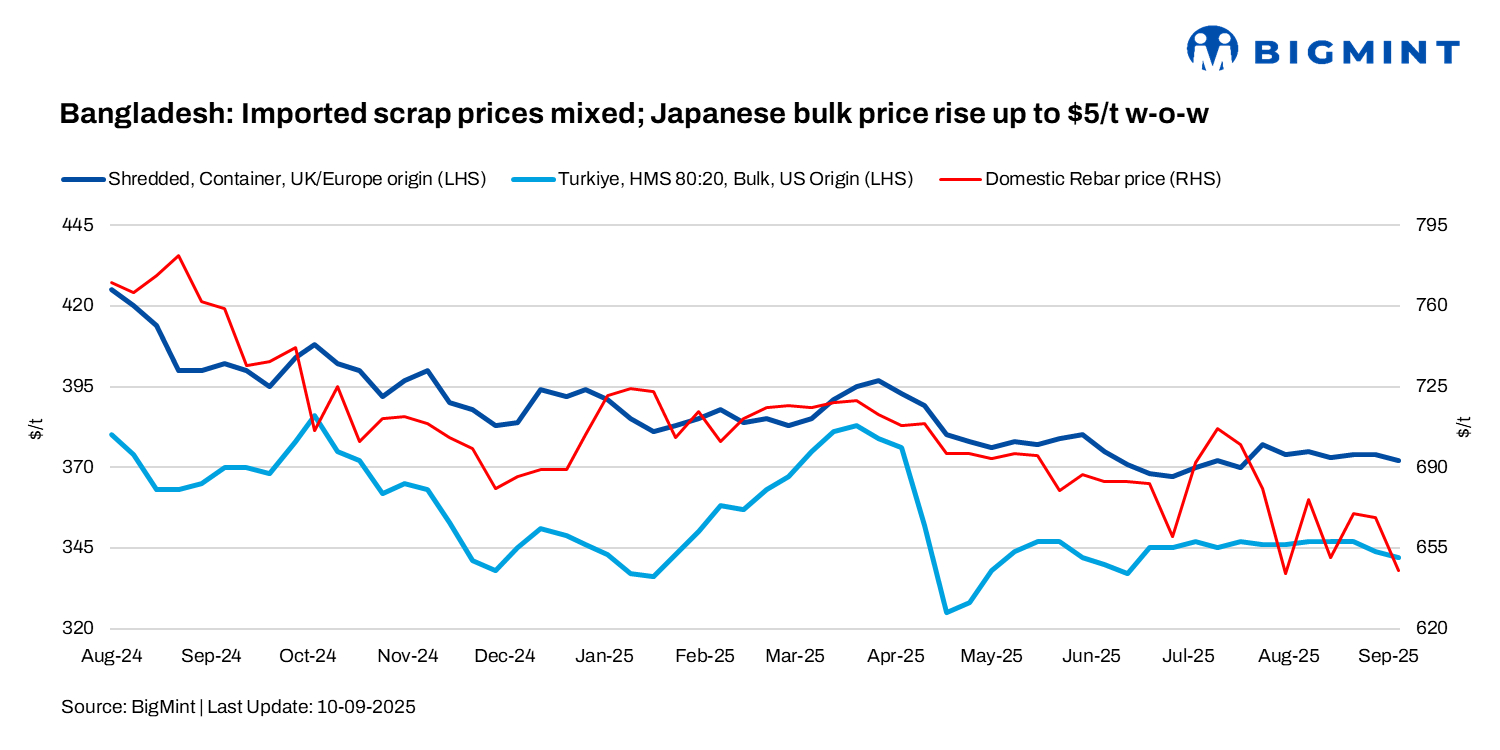

Bangladesh’s imported scrap prices witnessed a mixed trend in the last seven days, with most large buyers staying on the sidelines after completing September bookings.

Notably, the September 2025 Kanto scrap export tender witnessed a 15,000-t H2 lot reportedly awarded via a Japanese trading firm to a Chattogram-based mill at JPY 41,970/t ($285/t) FAS Japan. The tender witnessed the participation of a key Chattogram-based mill, which returned to the market after a month.

As per a major Chattogram-based trader, selective bulk purchases were heard in the last two weeks, while container trade remained sluggish amid wide bid-offer mismatches. Liquidity constraints and stagnant steel demand kept mills cautious, curbing fresh commitments.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched down by $3/tonne (t) w-o-w to $351/t.

- European-origin containerised shredded dropped by $2/t w-o-w to $372/t.

- Japanese-origin H2 bulk prices stood at $345/t, an increase of $5/t w-o-w.

- US-sourced HMS (80:20) bulk prices stood at $355/t, a rise of $4/t w-o-w.

Bulk trades in last 2 weeks

- 20,000-t Japanese H1/H2 (30:70) bulk cargo sold at $352-355/t CFR Chattogram.

- 10,000-t Japanese H2 bulk cargo sold at $338-340/t, HS at $368-370/t, two weeks ago.

- Japan’s September Kanto Tetsugen tender awarded 15,000-t H2 at JPY 41,970/t ($285 FAS), equivalent to $345-350/t CFR Chattogram.

- A Chattogram mill booked 30,000-t Australian bulk cargo at $343-345/t CFR late August.

- Two US West Coast-origin bulk cargoes (32,000 t) sold at $352/t CFR Chattogram.

Containerised market

Offers

- Australian shredded – $372-375/t CFR (bids $365-366/t).

- Australian HMS 90:10 – $355/t CFR (bids $345-346/t).

- Australian HMS 80:20 parcels sold at $345/t CFR.

As per market insiders, European suppliers remained absent, while US suppliers focused only on major Chattogram-based mills. Meanwhile, Australian container cargoes continued moving to Indonesia, where demand was stronger.

Trades

- Around 3,000-t shredded scrap (Australia) traded at $370/t CFR Chattogram.

- Around 1,000-t HMS 90:10 (Australia) booked at $351/t CFR.

- Nearly 1,000-t GI bundles (Philippines) sold at $312/t CFR

- 2000-t Australian HMS 90:10 booked at $355-360/t CFR.

Steel market update

Bangladesh’s local steel market saw slight gains, though tradable levels dropped BDT 2,000-2,500/t ($16-21/t). Rebar from Chattogram mills was quoted at BDT 78,000-80,000/t ($641-657/t), while Dhaka mills offered material at BDT 75,000-76,000/t ($616-624/t).

Premium offers exceeded BDT 80,000/t ($657/t), but workable levels remained at BDT 79,000-80,000/t ($649-657/t), reflecting selective buying. Billet prices rose by BDT 1,500/t ($12/t) to BDT 68,000-69,000/t ($558-567/t).

Scrap prices increased to BDT 47,000/t ($386/t) in Dhaka and BDT 49,000-50,000/t ($403-411/t) in Chattogram.

Chattogram ship-breaking market remains quiet

The ship-breaking sector stayed largely inactive, with no fresh arrivals. Steel plate prices fell $21/t w-o-w to $520/t due to weak demand, cheaper imports, and BDT depreciation. Active yards dropped 40%, and despite 18 Hong Kong Convention (HKC) accreditations, Chattogram recyclers faced a weak outlook. Ship demolition declined 57% to 43,830 LDT in August, with only 4 units dismantled versus 8 in July.

Outlook

Bangladesh’s imported scrap market is expected to remain selective in the near term, with bulk activity driven by need-based purchases from major mills. Container trade is likely to stay thin, and Dhaka-based mills are likely to dominate more over Chattogram mills.

On the domestic side, while local scrap and billet tags have shown an uptick, sluggish rebar demand may prevent mills from raising sales prices further.

Leave a Reply