- Stocks declines at Vizag, Gangavaram, and Mangalore

- South African and Indonesian coal markets stay cautious

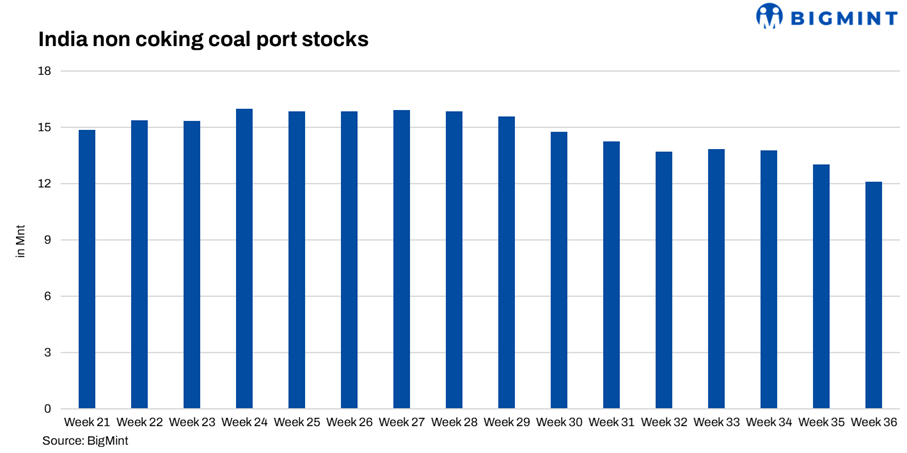

India’s portside thermal coal inventories slipped 7.1% w-o-w to 12.1 mnt in Week 36, down from 13.03 mnt in Week 35. Arrivals stayed muted as elevated import offers and higher freight rates inflated landed costs, while weak domestic demand continued to weigh on fresh bookings from traders and steelmakers.

Port-wise trends

In the east, Paradip slipped to 1.52 mnt from 1.57 mnt, down 3.4%, while Vizag fell to 1.07 mnt from 1.18 mnt, marking a 9.5% decline. Gangavaram dropped further to 0.20 mnt from 0.25 mnt, down around 20%, and Haldia eased to 0.09 mnt from 0.11 mnt, lower by 16.4%. Dhamra declined to 0.82 mnt from 0.99 mnt, falling 17.3%, while Kakinada moved down to 0.34 mnt from 0.42 mnt, down 17.3%.

In the south, Mangalore slumped to 0.16 mnt from 0.55 mnt, a sharp fall of 71.6%, and Krishnapatnam halved to 0.14 mnt from 0.34 mnt, down 58.2%. Karaikal reduced to 0.09 mnt from 0.15 mnt, down 40%. Tuticorin, however, remained steady at 0.83 mnt compared to 0.83 mnt last week, edging up by 0.9%.

On the west coast, Mundra surged to 0.88 mnt from 0.49 mnt, rising 80.8% on fresh replenishment at Adani’s terminal. Navlakhi inched up to 1.24 mnt from 1.23 mnt, up 1%, and Kandla rose to 0.86 mnt from 0.79 mnt, higher by 8.8%. In contrast, Hazira fell to 2.07 mnt from 2.16 mnt, slipping 4.2%, while Magdalla moved down to 0.54 mnt from 0.70 mnt, down 22.8%.

Company-wise movements

Adani Enterprises’ inventories eased to 2.88 mnt from 2.95 mnt, a fall of 2.1%, while Agarwal Coal’s stock reduced to 1.25 mnt from 1.32 mnt, down 5.3%, showing slower restocking by both players.

Market overview

South African RB2 export offers stayed stable w-o-w at $74/t FOB, while RB3 held at $61/t. Prices remained steady as muted demand kept importers cautious. High offers, partly driven by freight costs, are now also influenced by the GST slab change, limiting fresh bookings from Indian buyers.

South African RB2 and RB3 coal prices at Gangavaram held steady w-o-w at INR 8,300/t and INR 7,200/t. Sellers focused on clearing limited portside stocks before the 22 September GST deadline, while buyers stayed cautious, preferring to wait for new offers. The GST hike to 18% alongside cess removal has kept sentiment subdued, with participants awaiting its impact on steelmaking costs.

In the Indonesian coal market, sellers also pushed to liquidate inventories ahead of the GST shift. Prices for 5000 GAR slipped INR 50/t at Kandla and Vizag, while 4200 GAR remained steady and 3400 GAR eased at Navlakhi. Market activity stayed muted as rupee depreciation and firmer freight rates added pressure, while international prices registered only marginal corrections.

Leave a Reply