- LME copper steady at $9,870/t, touches nearly $9,950/t

- China Sept output down 4–5% m-o-m; first drop since 2016

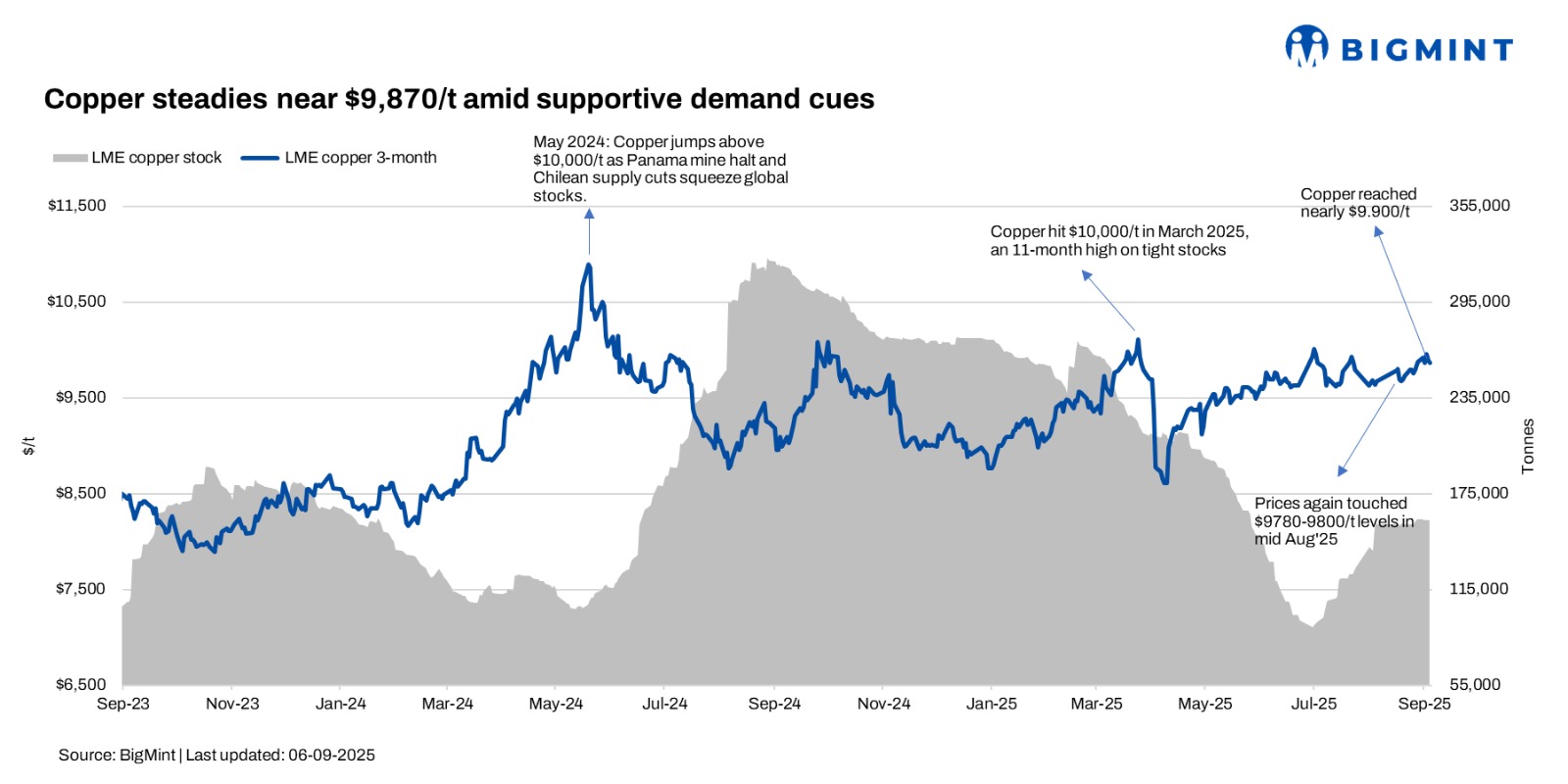

The benchmark three-month copper contract on the London Metal Exchange (LME) closed at $9,870/t on 5 September 2025, holding largely stable compared with its settlement on 29 August. While prices ended flat week-on-week, intraday momentum briefly lifted the red metal above the $9,920/t mark, highlighting underlying bullish sentiment in the market.

The sharp test towards the $9,920/t level underscores the influence of tightening supply dynamics and robust investor interest. Inventories across LME warehouses remain relatively high compared with mid-year levels, but recent drawdowns in Asia suggest a pick-up in physical demand. Traders also expect seasonal restocking ahead of year-end, particularly from the construction and power cable sectors.

Another important driver has been currency movements. The U.S. dollar’s recent softening provided a mild boost to dollar-denominated commodities, aiding copper’s attempt to edge higher. However, broader market caution capped follow-through buying, leading to the flat closing levels.

Looking ahead, analysts suggest that copper is likely to stay range-bound in the near term, with $9,800–$10,000/t acting as a key band of support and resistance. A sustained break above $10,000/t could re-ignite bullish momentum, though downside risks tied to demand softness cannot be overlooked.

China’s refined copper production for September 2025 is projected at 1.138–1.168 million tonnes, marking a rare month-on-month decline of about 4–5% from August levels, according to Shanghai Metals Market and industry analysts. This is the first such September drop since 2016 and is attributed to new tax regulations constraining copper scrap supply, plus maintenance at five major smelters, as per reports.

In August 2025, China’s copper cathode production was around 1.168 million tonnes; so September’s output could fall by approximately 50,000–60,000 tonnes from that figure. Despite this dip, cumulative production for 2025 remains at a record-setting pace, up about 12% year-on-year over the January–August period.

Copper is expected to remain range-bound at $9,800–$10,000/t in the near term, aided by lower Chinese output and seasonal restocking. As per Goldman Sachs, prices could still average around $9,890/t in H2 2025, before easing toward $9,700/t by December, with upside capped near the $10,000/t mark.

Leave a Reply