- Sponge iron prices remain steady w-o-w

- Semis, finished steel prices dip by INR 630-765/t w-o-w

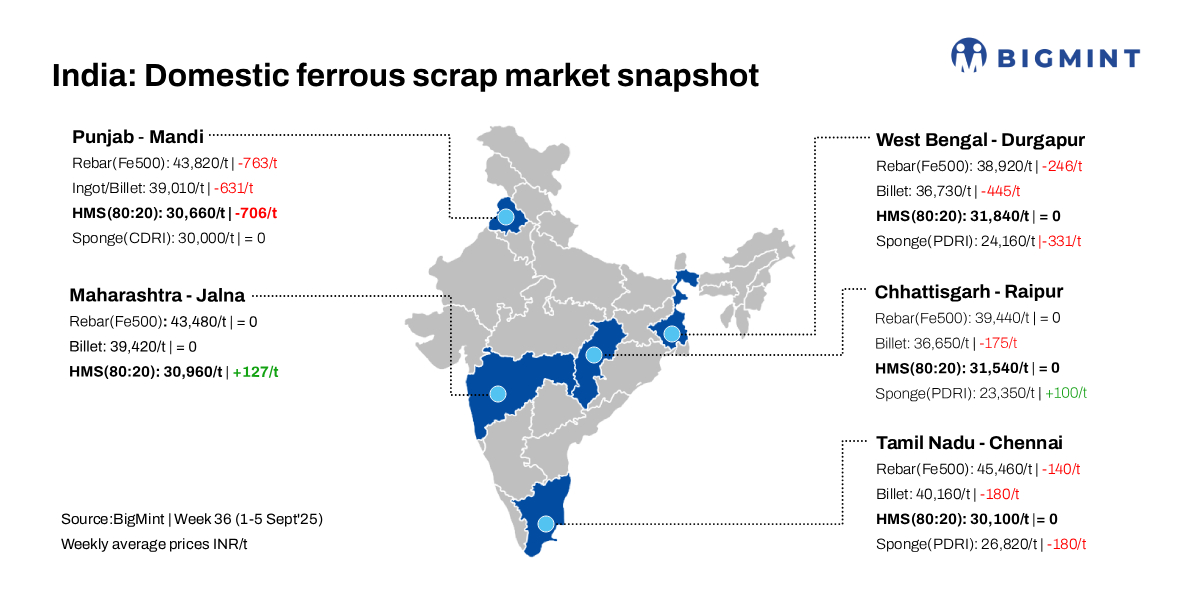

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, edged up by INR 100/tonne (t) to INR 34,300/t DAP on 5 September 2025. As per weekly basis scrap, prices in the region dipped by INR 670-700/t.

After the GST Council’s decision to maintain the 18% tax rate on steel scrap, the Mandi steel market witnessed a slight uptick in scrap prices. Suppliers responded to the continued tax burden by raising offers in yesterday’s trading session, reflecting an attempt to protect margins amid sustained costs. This increase highlights sellers’ efforts to navigate an unchanged tax environment while capitalizing on local demand dynamics.

The northern region is contending with seasonal challenges and localized flooding, which are disrupting logistics and suppressing demand in key hubs such as Mandi Gobindgarh. Market participants report that these adverse conditions are limiting trade activities, further weighing on an already fragile demand outlook.

A mill owner informed, “The ample availability of local scrap has made domestic sourcing more cost-effective compared to imports. The price gap between local and imported scrap currently ranges between $10 and $15/t, encouraging mills to favour local procurement. Furthermore, the recent appreciation of the US dollar against the Indian rupee has increased import costs, making overseas purchases less viable. With the domestic secondary steel market remaining sluggish, mills are increasingly dependent on local scrap to control production expenses.”

Raw material

The sponge iron (CDRI) market in Mandi Gobindgarh remained stable for the sixth consecutive day, holding steady at INR 30,000/t DAP, with prices unchanged on a week-on-week basis. In contrast, steel-grade pig iron prices in Ludhiana slipped by INR 50/t to INR 35,400/t DAP, marking a weekly decline of INR 113/t.

Steel market

Semi-finished steel (ingot) prices in Mandi Gobindgarh increased by INR 200/t d-o-d, reaching INR 39,200/t DAP. This upward movement was reflected across major production centres, with price gains ranging from INR 100 to 400/t. However, on a weekly basis, prices have corrected downward by INR 630/t.

In the rebar (Fe500) segment, prices in Mandi declined by INR 200/t to INR 43,600/t ex-works, driven by subdued demand conditions. Weekly prices also registered a notable drop of INR 763/t. Conversely, HR strip (patra) segment exhibited stronger demand momentum, with prices rebounding by INR 800/t to INR 42,000/t ex-works following increased buying interest in yesterday’s trading session.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $332-$333/t, which equates to approximately INR 31,546/t (including freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 31,000/t DAP today. Indicative prices of shredded from Europe stood at $364/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,350/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply