- Wide bid-offer spreads limit fixture activity in Pacific

- Trading out of Atlantic stays tepid during Asian hours

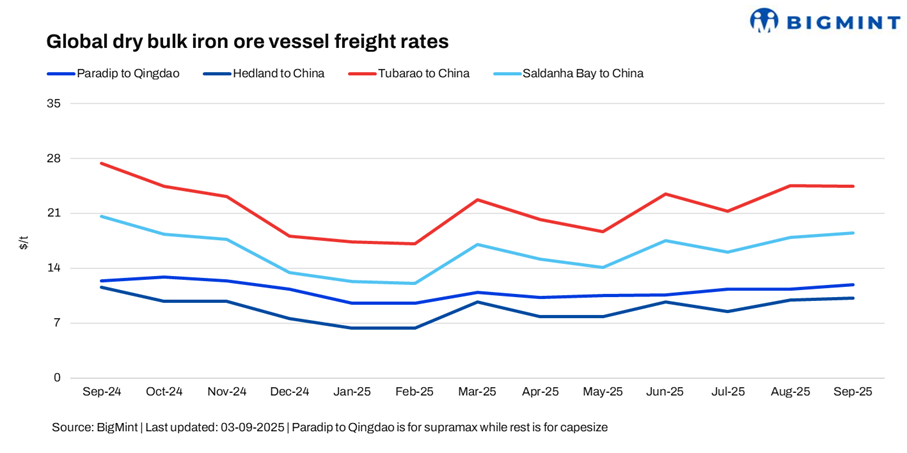

Dry bulk iron ore freights showed mixed trends this week. While Australia-China and Brazil-China routes edged lower, India-China and South Africa-China routes firmed up, reflecting varied demand and supply dynamics across basins.

Some sources claimed that in the Asia-Pacific Supramax market, freight sentiments were weak, weighed down by elevated tonnage supply and limited fresh cargoes in the Pacific. A similar pattern persisted in the Indian Ocean, where sluggish activity and ample vessel availability kept rates under pressure.

Meanwhile, Capesize rates also eased this week as sentiment weakened further. Market participants noted weak confidence, with spot tonnage demand slipping and freight derivatives rates (FFAs) posting deeper losses during Asian trading hours, leaving overall market direction uncertain.

Among Western Australian mining majors, BHP, FMG, and Rio Tinto were reported to be actively seeking tonnage.

Additionally, fixtures remained limited, as activity out of the Atlantic basin was also subdued. Sources noted that market participants were keeping a close watch on ballaster supply for Brazil loadings, though firm trading activity was scarce during Asian hours.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China inched up by $0.69/dry metric tonne (dmt) w-o-w to $11.94/dmt. India’s iron ore export prices held largely steady this week, with seaborne trading activity remaining thin. A few deals were concluded, but overall sentiment stayed muted amid wide bid-offer gaps. Participants expect the near term to remain muted unless Chinese buying picks up or domestic procurement costs ease.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China decreased by $0.5/dmt w-o-w to $10.20/dmt. Initial indicative Capesize offers on the Australia-China route were heard at around $10.25-10.45/dmt. As the week progressed, offers slipped to the low $10-10.20/dmt range, with sentiment weakening and charterers pushing back against owners’ expectations.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments also witnessed a drop of $0.5/dmt w-o-w, settling at $24.50/dmt. On the Tubarao-Qingdao route, only one fixture was reported this week at around $24.7/dmt. Vessel movement from Tubarao-Qingdao remained very low as weak Chinese demand and soft steel margins curbed fresh bookings, while elevated tonnage availability gave charterers little urgency to fix.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao rose by $0.25/dmt w-o-w, settling at $18.5/dmt. Activity on the South Africa-China route improved slightly from the previous week, with two fixtures reported. The first was concluded at around $19.38/dmt, but rates slipped sharply on the second to nearly $18.55/dmt. The drop underscored subdued demand and limited charterer competition, keeping overall sentiment weak on the route.

Market highlights

- Baltic index heads south w-o-w: The Baltic Exchange’s main dry bulk sea freight index dropped w-o-w on 3 September 2025 on weaker demand across vessel segments. The overall index decreased around 55 points w-o-w to 1,986, with the Capesize index falling sharply by around 157 points to 2,874. However, the Supramax segment provided some support to the overall index, rising by 29 points w-o-w to 1,466.

- Crude oil futures drop w-o-w: Brent crude oil futures dropped this week as supply concerns resurfaced, with OPEC+ signalling potential output hikes that could unwind earlier production cuts. Expectations of higher supply, combined with sluggish demand growth in key markets such as the US and China, fuelled oversupply worries and outweighed any geopolitical support, keeping market sentiment bearish. Reflecting the bearish sentiment, Brent crude futures decreased w-o-w to $68.62/barrel (bbl) on 3 September 2025.

- DCE iron ore futures unchanged w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract remained unchanged at RMB 777/t ($109/t) on 3 September. DCE iron ore futures remained flat w-o-w as market participants weighed steady supply against subdued demand signals. While expectations of restocking after China’s military parade lent some support, persistent caution from mills amid weak steel margins and limited spot activity kept prices broadly flat.

Outlook

In the near term, dry bulk iron ore vessel freights are likely to remain under pressure, with muted demand from China and ample vessel availability capping upside momentum. While occasional fixtures may lend temporary support, sentiment is expected to stay cautious as charterers resist higher offers and freight derivatives continue to signal weakness.

Leave a Reply