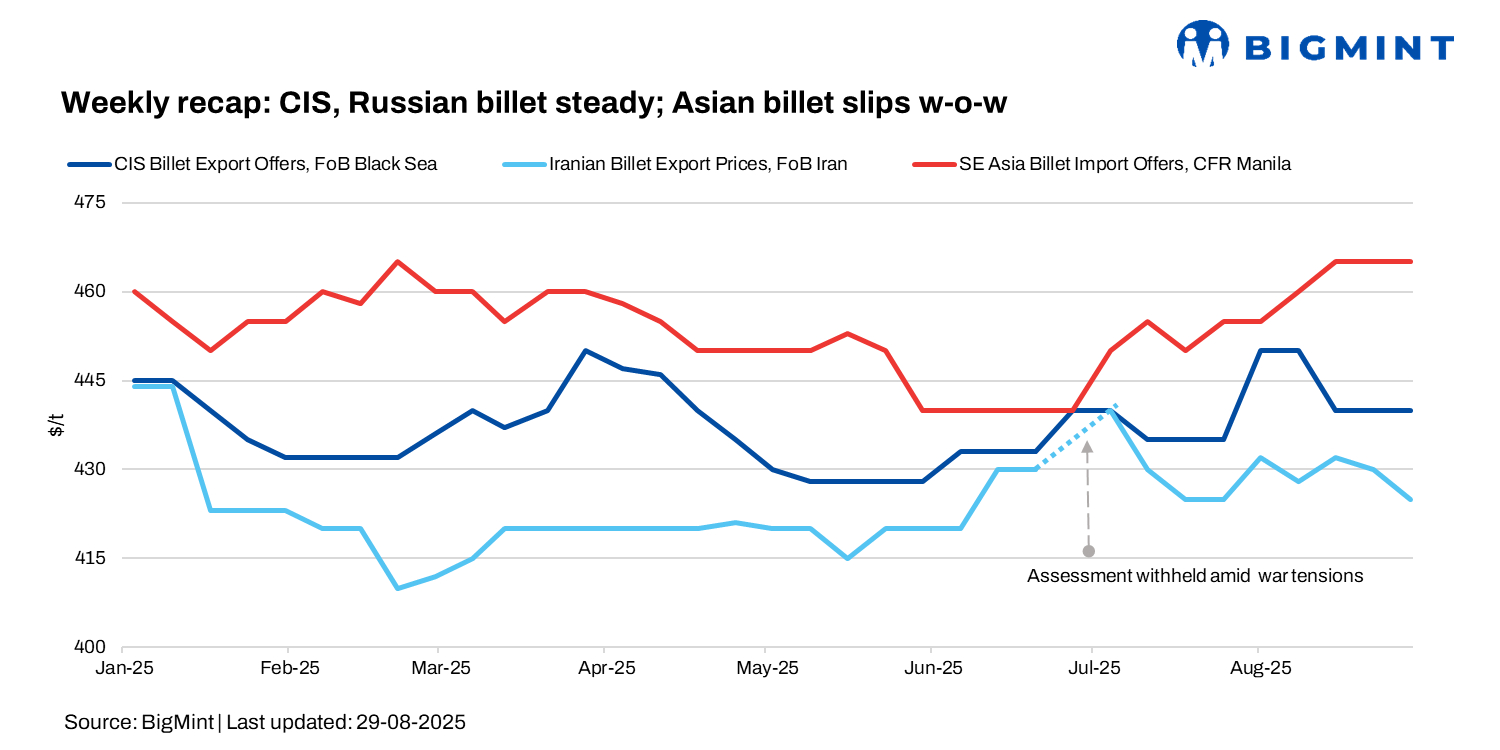

- Muted activities in CIS region keeps tags unchanged

- China, Iran show mixed trends; demand weakness caps gains

Global billet prices remain largely stable in the 35th week of 2025. CIS billet export activity stayed muted last week, with Russian October-shipment offers stable at $440-450/t FOB Black Sea, though a few small deals were done at slightly lower levels.

Asian semis also added pressure, with Chinese billets easing by up to $5-7/t against a week prior.

Meanwhile, the Turkish deep-sea scrap market stayed muted as mills remained inactive amid seasonal slowdown and weak steel demand. HMS 80:20 held at $346-347/t CFR early in the week, with EU cargoes at $334-340/t CFR. By week’s end, US-origin HMS 80:20 slipped to $345/t CFR on higher freight costs, while ample EU supply and limited US availability kept Turkish buyers cautious.

Market highlights

In Turkiye, CIS billet was offered at $460-470/t CFR ($435-440/t FOB), with limited trades at $460-465/t CFR, but by week’s end, buyers cut bids to $445-455/t CFR ($420-430/t FOB), levels more aligned with Ukrainian sellers.

As per a market insider from Turkiye, billet imports only work when rebar exports are viable, but with rebar export prices still uncompetitive, buyers remained cautious.

Domestically, Turkish billets softened to $500-505/t exw from $510-515/t a week earlier, pressured by weak demand and cheaper Asian semis–Chinese billets fell to $475-480/t CFR Turkiye from $485-490/t, while Malaysian stayed flat at $495/t.

In the Philippines, billet offers remain steady at $465-470/t CFR with minimal inquiries from the market.

Iran’s steel market showed mixed trends in the week ended 27 August. Domestic billet rose 4,000 rial/kg w-o-w to 333,500 rial/kg, while rebar slipped 3,000 rial/kg to 380,000 rial/kg. Power shortages curbed output, but billet demand stayed weak, whereas rebar trade found some support from credit-based sales, though prices remained well below stock exchange levels.

On the export side, billet offers held at $420-425/t FOB and slab at $405-410/t FOB, but deals were scarce as buyers in the UAE and Oman resisted higher prices. Rising domestic inventories further weighed on sentiment, leaving mills with limited room to lift offers.

China billet prices inch down by RMB 20/t ($3/t)

Tangshan billet slipped RMB 20/t ($3/t) w-o-w to RMB 3,010/t, while SHFE Oct’25 rebar futures fell RMB 29/t ($4/t) to RMB 3,090/t. Domestic billet firmed early in the week but weakened on oversupply from higher steel output. Export offers initially gained $3-5/t on tight supply and stronger raw materials, but later softened amid muted construction demand, weaker exports, and plate mills trimming $5/t despite rising HRC inquiries.

Leave a Reply