- Supply tightness in north India prompts price hikes

- LME zinc futures edge lower, HZL trims ingot prices

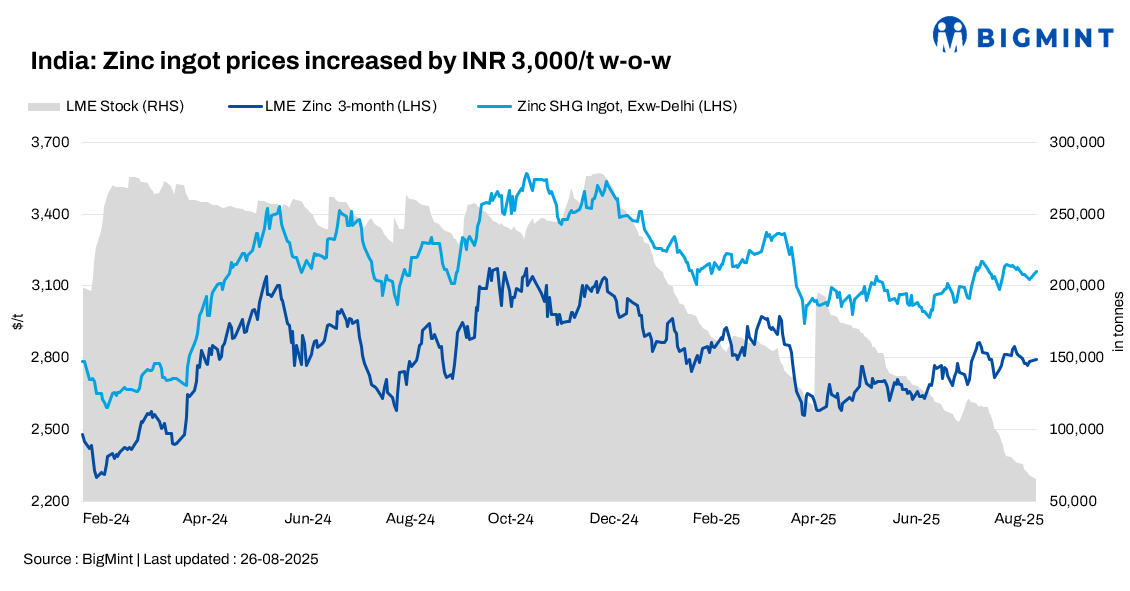

India’s zinc ingot (99.995%) prices rose by INR 3,000/tonne (t) w-o-w to INR 278,000/t ex-Delhi, as per BigMint’s assessment. The uptrend was driven by supply tightness in north India and firmer overseas offers, while overall demand remained subdued.

On 25 August 2025, Hindustan Zinc Limited (HZL) trimmed its zinc ingot prices by INR 200/t ($2/t) to INR 283,100/t ($3,238/t) ex-Chanderiya.

Special High Grade (SHG) zinc ingots were offered at INR 269,000/t ex-Mumbai, up by INR 1,000/t from last week, though trading was limited. In the import market, Australian-origin SHG zinc ingots were quoted at a premium of $360/t over London Metal Exchange (LME) prices at CFR Mundra Port, but no fresh bookings were observed, as shipments are unlikely before mid-October.

Shortages in Delhi pushed Australian offers to INR 348,000/t ex-Delhi, higher by INR 8,000-10,000/t w-o-w, with some traders expecting levels near INR 370,000/t in the short term.

Global zinc futures snapshot

As of 26 August, LME three-month zinc futures fell by $51/t w-o-w to $2,794/t, pressured by macroeconomic concerns and sluggish global industrial activity.

On the Shanghai Futures Exchange (SHFE), the September zinc contract dipped by RMB 250/t w-o-w to RMB 22,300/t, with Chinese demand still subdued despite restocking expectations ahead of September.

In India, MCX zinc August futures eased by about INR 1,000/t w-o-w, hovering in the INR 263,500-264,500/t range, mirroring overseas weakness and thin domestic trading volumes.

Zinc semi-finished imports surge

India’s zinc semi-finished (ingot) imports rose sharply in July 2025 to 31,689 t, more than doubling from 12,188 t in July 2024, and over 100% higher m-o-m against 14,827 t in June 2025.

In January-July 2025, total imports reached 145,892 t, up 34% y-o-y from 108,903 t in the same period of 2024.

The surge comes ahead of the Refined Zinc (Quality Control) Order, 2025, effective 17 October 2025, mandating BIS certification and ISI marking (IS 209:2024) for all refined zinc ingots sold in India. This has prompted domestic producers and importers to boost volumes, ensuring smooth trade flows.

Outlook

Domestic zinc prices are likely to remain range-bound with muted demand and overseas weakness limiting upside. Import tightness, particularly for Australian-origin zinc, may lend short-term support in north India. Rising pre-BIS order imports are expected to keep the market adequately supplied into Q4CY’25.

Leave a Reply