- Monsoon, festive lull affect construction activity

- Some major mills reduce prices amid limited offtake

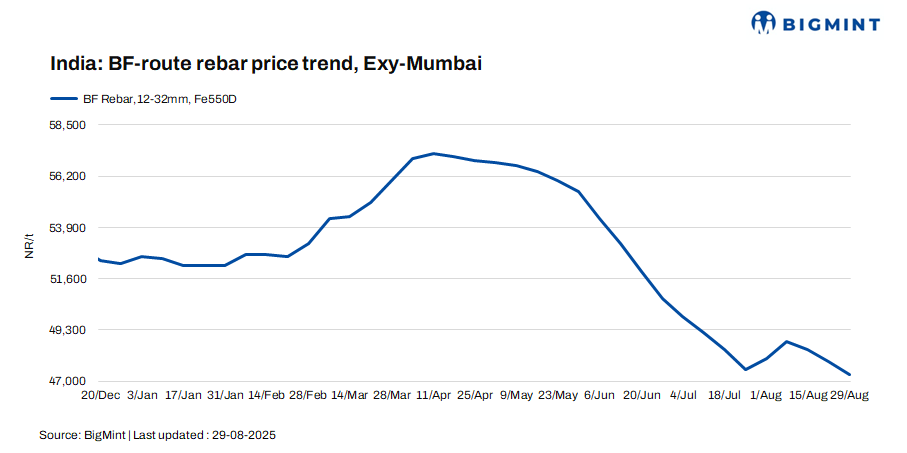

India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets. Some steel majors reduced their prices amid subdued domestic demand this week.

Trade-level BF rebar prices decreased by INR 600/tonne (t) ($7/t) w-o-w to INR 47,300/t ($538/t) exy-Mumbai, as per BigMint’s assessment on 29 August 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices dropped w-o-w to INR 46,000-47,000/t ($523-535/t) FOR Mumbai. Market activity was muted, as buyers stayed cautious during the monsoon season and the festive week. Construction momentum was further dampened by logistical challenges, leading to project delays and subdued procurement.

Update on projects

- Ashoka Buildcon received an LOA worth INR 499.95 crore from Northwestern Railway, Jaipur, for upgrading the electric traction system to 2×25 kV with OHE modification, covering 581 km.

- IRCON International has received an INR 510 crore engineering, procurement, and construction (EPC) contract from NESTS for constructing Eklavya Model Residential Schools across 11 districts of Meghalaya, strengthening its presence in education infrastructure development.

- IRB Infra’s SPV, VM7 Expressway Pvt. Ltd., achieved Provisional COD for its 27.5 km Gandeva-Ena HAM project on the Delhi-Mumbai Expressway, enabling INR 180 crore annual annuity from NHAI over 15 years.

- G R Infraprojects received an LOI from REC Power for developing transmission systems evacuating 2,500 MW of renewable energy in Madhya Pradesh. The INR 3,670.73 million project, under the BOOT model, has a 35-year O&M period.

- Rail Vikas Nigam Limited (RVNL) has signed a joint venture agreement with Texmaco Rail & Engineering Ltd., with 51:49 shareholding, to undertake railway and allied infrastructure projects in India and abroad.

Factors behind market dynamics

1. IF rebar trade prices decline w-o-w: Induction furnace (IF) rebar trade prices declined w-o-w across key Indian markets. Prices dropped amid subdued trading activities due to rainfall in some regions and the festive season. Manufacturers reduced their list prices and offered discounts to liquidate material. There was no major buying interest during the week and limited offtake. Inventory days were more than 12 days across regions. IF rebar prices dropped by INR 900/t ($10/t) w-o-w to INR 44,800/t ($510/t) exw-Mumbai as on 29 August 2025.

The BF-IF rebar price gap stood at around INR 2,000-2,500/t ($23-28/t) in Mumbai. IF rebars hold a dominant 65-70% market share in India.

2. Raw material prices show mixed trends w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,500/t ($63/t) ex-mines on 23 August 2025.

Iron ore prices in Odisha stayed firm this week following the recent OMC auction, where bids for fines rose while those for lumps remained largely stable compared to the July event. The auction witnessed strong participation from steelmakers, with over 2 million tonnes (mnt) of material booked. Meanwhile, supply disruptions due to the monsoon kept iron ore prices in Odisha stable w-o-w.

Australian premium hard coking coal (PHCC) prices rose by $4/t w-o-w to $206/t CNF Paradip.

Outlook

Market participants are waiting for mills’ prices for next month, which are likely to be announced next week. Meanwhile, buyers are cautious in making purchases amid weak market sentiments.

Leave a Reply