- Charterers show limited interest in closing Pacific trades

- Wide bid-offer spread, firm stances hinder trade activity

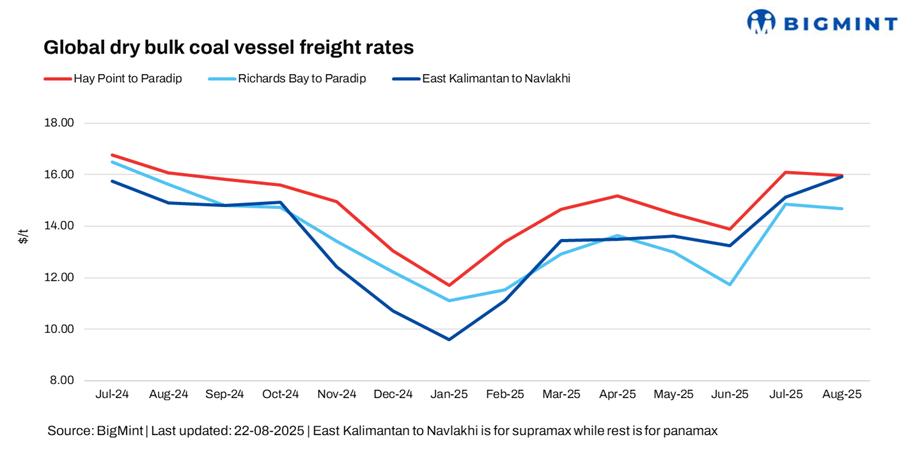

Dry bulk coal freights to India remained steady w-o-w across all key routes — Australia, South Africa, and Indonesia — despite the absence of significant vessel trading activity.

Cargo volumes from both the Pacific and Atlantic basins showed little movement, keeping vessel demand weak and likely to pressure rates in the near term. Meanwhile, many Pacific cargoes have forward loading dates and are not for prompt shipment, so charterers are not rushing to close deals, sources told BigMint.

Additionally, persistent rainfall across parts of India continued to dampen thermal coal demand, leading to slower vessel booking activity. Most market participants stayed on the sidelines, waiting for a correction in offers.

From the Pacific basin, no major coal inquiries emerged from operators, offering little support for a market recovery.

However, both charterers and shipowners remained firm on their positions, with neither side willing to concede. This kept the bid-offer spread wide, hindering trade execution for most of the Asian trading session.

Meanwhile, India’s portside thermal coal stocks rose 1.2% w-o-w to 13.86 million tonnes (mnt) in Week 33, from 13.70 mnt in Week 32. However, Paradip’s stocks dropped 8.8% w-o-w to 1.59 mnt from 1.74 mnt.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India remained stable w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16/dry metric tonne (dmt). Persistent heavy monsoons in parts of India continued to disrupt port operations, causing delays in cargo handling and vessel turnaround. Meanwhile, cautious buying by Indian blast furnace operators kept import demand in check.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route also remained unchanged w-o-w to $15/dmt. Portside offers for South African thermal coal in India held largely steady this week, but overall activity remained muted, with few trades heard, as high prices kept buyers cautious and delayed fresh bookings. A weak domestic sponge market also weighed on demand for South African coal, BigMint understands.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route stood at $15.93/dmt, stable w-o-w. On the Indonesia-India coal route, reports of fresh fixtures were scarce during the day, reflecting subdued trading interest. Market participants indicated that limited buying appetite from Indian end-users, combined with ample vessel availability, kept activity sluggish and prevented any notable movement in freight levels.

Meanwhile, the Baltic Exchange’s main dry bulk sea freight index faced pressure this week. The overall index slipped 34 points d-o-d to 1,893.

Outlook

In the near term, dry bulk coal freights are expected to either remain range-bound or soften a bit, as muted Asian demand and ample vessel availability weigh on market momentum. While South Africa may sustain export flows on improved logistics, Australia and Indonesia could face headwinds from weak buying interest and port delays.

Leave a Reply