- BF-rebar trade prices drop INR 400/t w-o-w, HRC holds firm

- Govt imposes AD duty on flat steel imports from Vietnam

- DGTR moots 3-year staggered safeguard duty on flats imports

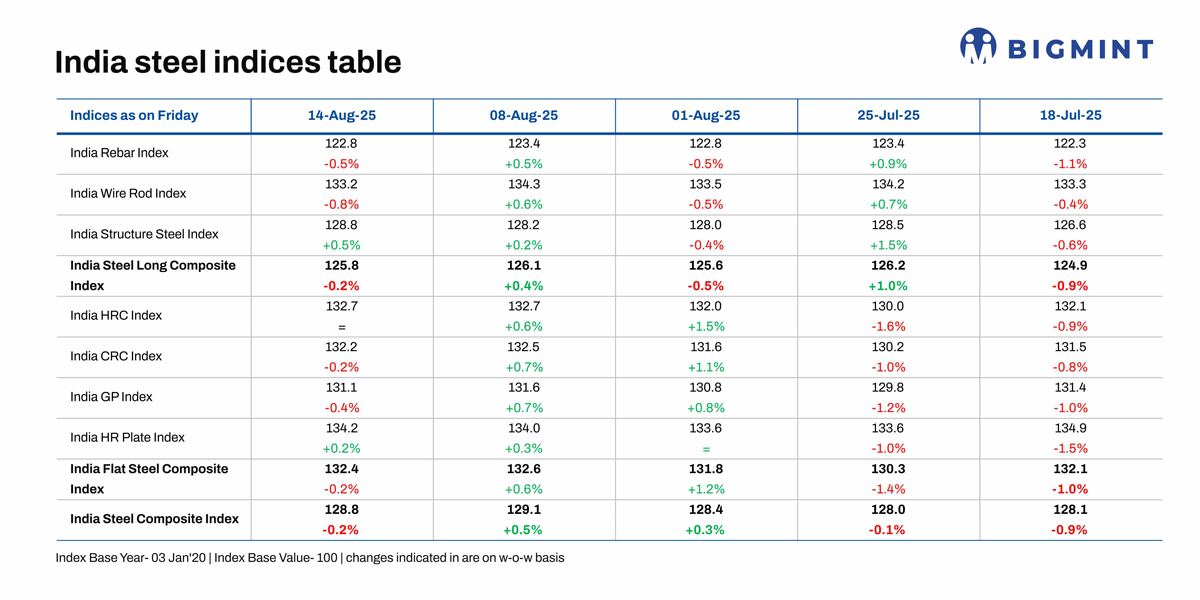

Morning Brief: BigMint’s flagship India steel composite index, a barometer of the domestic steel market, edged down by 0.2% w-o-w on 14 August 2025 after ascending for two consecutive weeks. The decline is attributable, in equal measure, to the 0.2% w-o-w drop in the long and flat steel indexes, with the rebar and wire rod sub-indexes showing sharp w-o-w decreases.

Sources said the weakness in domestic steel prices last week was due to the Independence Day holiday and Janmashtami festivities that kept market activity somewhat muted.

Analysis of price movements

Rebar prices drop: Trade-level BF rebar prices dropped by INR 400/tonne (t) ($5/t) w-o-w to INR 48,400/t ($553/t) exy-Mumbai, as per BigMint’s assessment on 14 August. Prices are exclusive of GST at 18%.

Festive week slowdown in the trade channel weighed on market sentiments. In the projects segment, prices fell w-o-w to INR 47,500-48,000/t ($543-548/t) FOR Mumbai, driven by sluggish end-user demand during the festive week. Meanwhile, a leading private steel mill has scheduled an annual maintenance shutdown at one of its plants till next week, sources informed.

Induction furnace (IF) rebar prices showed mixed trends w-o-w. Trade prices dropped across major markets while remaining stable in a few. Demand was need-based. Semi-finished steel prices also declined w-o-w, which led to a lack of cost support. Inventory levels ranged between 10 and 12 days across regions.

HRC market remains weak: Trade-level prices of hot-rolled coils (HRCs) in India remained stable w-o-w at INR 49,200-51,200/t ($561-584/t) but BigMint’s benchmark bi-weekly assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) dropped INR 200/t ($2/t) w-o-w to INR 50,000/t ($570/t) on 12 August. On the other hand, CRC (IS513, Gr O, 0.9 mm/CTL) prices remained stable at INR 57,000/t ($650/t).

The market witnessed a slowdown, with demand remaining weak and buyer inquiries limited. Market participants attributed the sluggish activity to the ongoing festive period, which temporarily dampened trading momentum. Traders expect clearer demand signals to emerge in the first week of September, once market activity resumes post-festivities.

HRC imports: India’s bulk imports of HRCs touched 195,577 t as of 12 August, based on vessel line-up data. Around 151,508 t of additional cargo are expected by late-August.

India’s Directorate General of Trade Remedies (DGTR) has recommended an anti-dumping duty of $121.5/t on imports of hot-rolled flat products of alloy or non-alloy steel from Vietnam, following the final findings of its investigation, as announced on 13 August. The DGTR has recommended a fixed anti-dumping duty for imports from Vietnam for five years.

With landed HRC prices from China and Japan remaining higher than domestic prices, it is clear that the safeguard duty has stablised the market condition for domestic players.

Outlook

Although domestic consumption remains strong, in the near term steel prices are expected to stay rangebound amid slow trade activity during the festive season and the holiday lull. Market participants expect demand signals to become clearer in early September, with activity likely to pick up ahead of the Navratri festivities beginning late September.

Additionally, the Directorate General of Trade Remedies (DGTR) has proposed imposing the safeguard duty for three years, with staggered rates of 12% in the first, 11.5% in the second, and 11% in the third. The potential implementation of such a long-term trade barrier may provide a fillip to domestic producers. However, given the steady price downtrend in the previous few months, it is uncertain if the impact will be sustained.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply