- Stainless steel prices rise despite weak demand

- Market cautious amid BIS norms and US tariffs

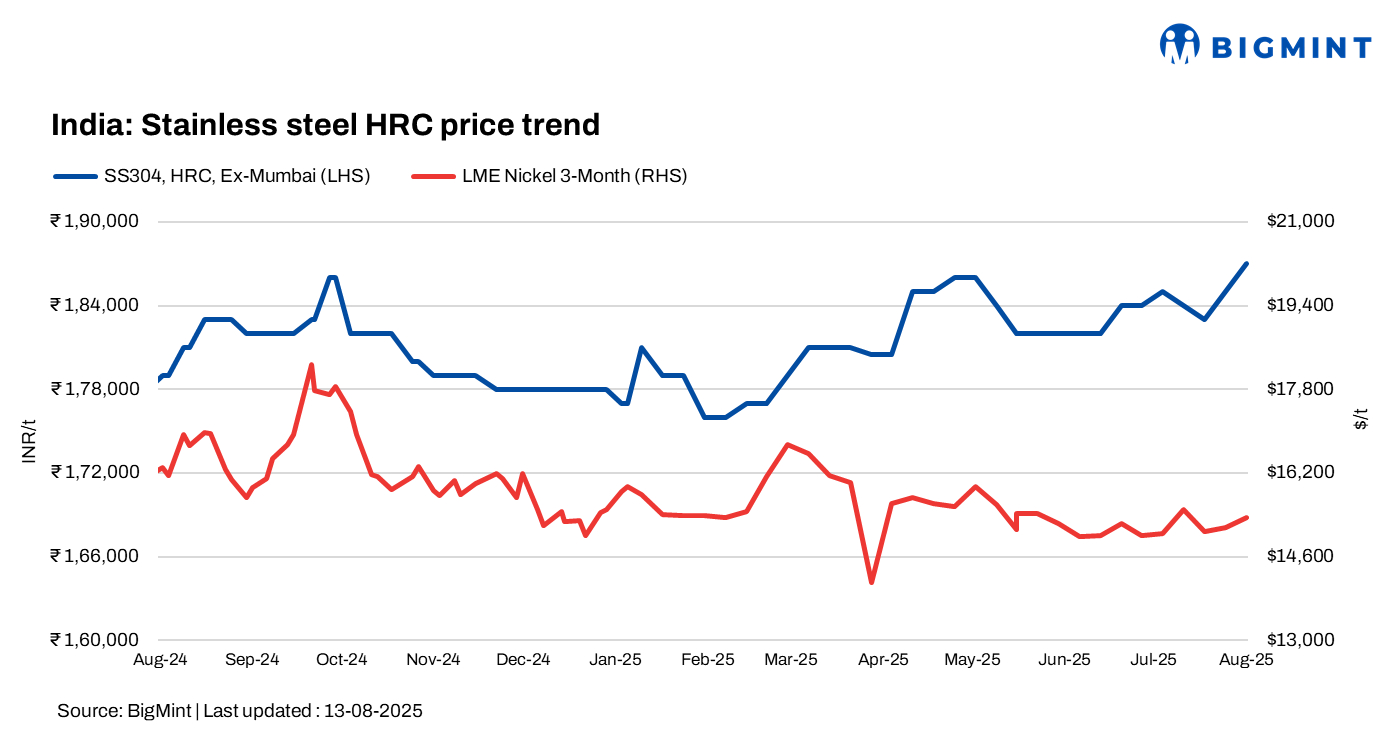

India’s stainless steel market witnessed upward movement this week despite weak demand and limited trading activity.

BigMint’s benchmark assessment for 304-series hot-rolled coils (HRCs) rose by INR 3,000/tonne (t) w-o-w to INR 187,000/t ex-Mumbai. Meanwhile, 304L black round bars (25-100 mm) was assessed at INR 157,000/t, up by INR 2,000/t w-o-w.

BigMint’s assessment for SS 316 HRCs stood at INR 335,000/t and for 316 cold-rolled coils (CRCs) at INR 338,000/t ex-Mumbai, both up INR 3,000 /t w-o-w.

Market updates

India’s stainless steel finished market sentiment remains largely subdued with no notable improvement, as participants remain cautious amid the recently notified BIS certification requirements for imports and following Trump’s tariff announcement. For context, Trump announced a 25% tariff on steel imports initially, which he later doubled to 50% on 4 June.

Indicative FOB prices for stainless steel longs remain steady, with India’s 304 bright bars at $2,050-2,100/t and 316 bright bars at $3,600-3,650/t, while Vietnams 304 bright bars are quoted at $1,940-1,990/t and 316 bright bars at $3,440-3,490/t. On the other hand, Europe domestic stainless steel 304 bright bars indicative levels were heard at $2,900-3,000 and 316 bright bars were heard at $4,450-4,550/t.

LME nickel up, Asian NPI firm

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,350/t, up 1.6% w-o-w. Nickel stocks at LME-registered warehouses stood at 211746

t, up 3% w-o-w compared to 211,254 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) remained firm w-o-w at RMB 917/t ($128/t). Meanwhile, Indonesian FOB prices of NPI (12-14%) stood at $114/t.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,450/t ($1,873/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were firm at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices stayed largely stable w-o-w, going up slightly by INR 35,000/t ($399/t) as compared to the assessment on 6 August. Prices stayed firm with steady demand and slightly improved molybdenum oxide supply.

As per BigMint’s assessment on 13 August, ferro molybdenum prices in India were INR 2,980,000/t ($33,988/t) exw-India.

Ferro Silicon: Indian ferro silicon (70%) prices witnessed a drop of INR 1,500/tonne (t) ($17/t) w-o-w as against the previous assessment on 4 August. Prices declined as bulk deals were finalised at lower rates. Additionally, expectations are that ongoing market negotiations may also lead to deals closed at reduced values.

As per BigMint’s assessment on 11 August, ferro silicon prices in India were at INR 93,500/t ($1,067/t) exw-Guwahati. In Bhutan, prices declined by INR 500/t ($6/t) w-o-w to INR 94,500/t ($1,078/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,600/t ($1,146/t) exw-Jajpur, range-bound w-o-w.

Ferrous scrap: India’s imported scrap market stayed quiet with no major trades, as buyers resisted high offers. UK/EU-origin shredded was offered at $365/t CFR, HMS 80:20 at $330-335/t CFR, and US/UK-origin shredded near $370-375/t CFR, but workable levels were lower.

Mills avoided fresh bookings due to a weaker rupee, sufficient domestic supply, and the upcoming 50% US tariff on Indian goods. Buying interest remained limited, with only sporadic inquiries ahead of the post-monsoon season.

Outlook

Market participants remain cautious and are expected to remain quiet in the near term, sustaining the risks and pressures currently affecting global steel flows.

Leave a Reply