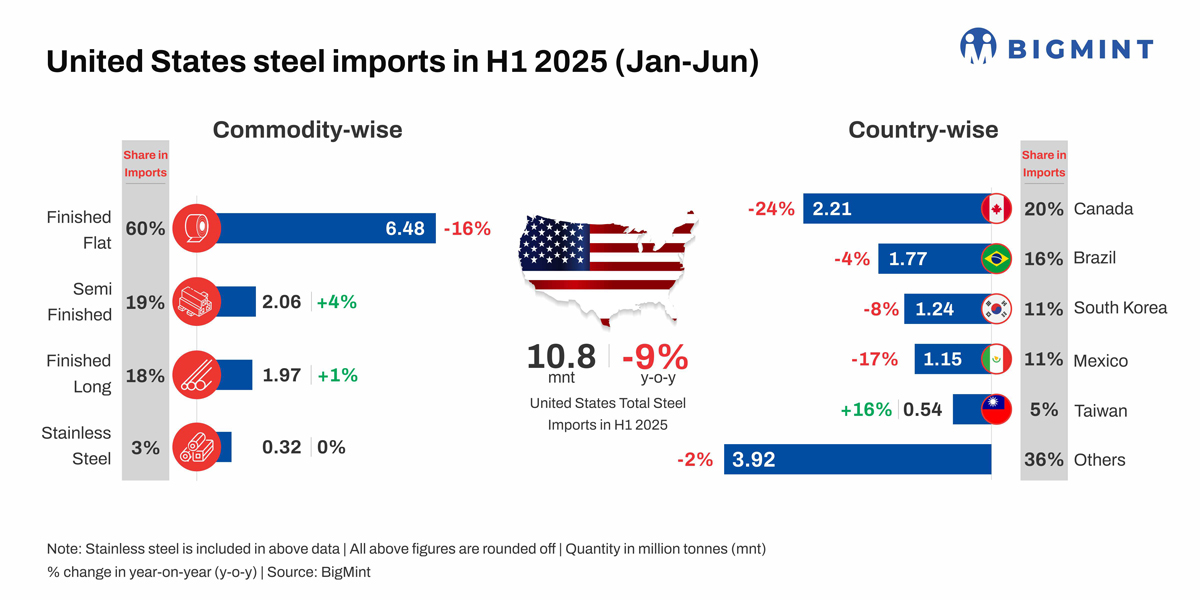

- Imports decline 17% y-o-y in Q2 following stable Q1

- Canadian shipments fall 24%, Mexico sees 17% drop

- Pipes, tubes remain only flat products to see growth

Morning Brief: US steel imports (including stainless steel) declined moderately by 9.4% y-o-y in January-June 2025 (H1CY’25), a far cry from the sharp reduction expected by industry stakeholders following Trump’s tariff announcement.

Volumes totalled 10.83 million tonnes (mnt) in H1CY’25 against 11.96 mnt in the year-ago period. Specifically, the January-March quarter witnessed arrivals of 5.78 mnt, reflecting a marginal 1.3% y-o-y decrease. However, imports declined 12.6% q-o-q and 17.2% y-o-y to 5.05 mnt in the April-June quarter.

This shows that imports were frontloaded to Q1 amid tariff apprehension but then declined gradually in Q2CY’25, which demonstrates that Trump’s tariffs, the first round of which came into effect on 12 March, have had some success in reducing the US’s import burden. For context, Trump announced a 25% tariff on steel imports initially, which he later doubled to 50% on 4 June.

However, it should be noted that, besides the tariff impact, the decline in steel imports could also be attributed to persistent demand weakness, which poses a significant headwind that not even tariffs can help address.

Country-wise imports – Canada leads despite 24% drop in H1CY’25

The top four leading steel exporters to the US — Canada, Brazil, South Korea, and Mexico — witnessed a drop in volumes in H1CY’25. For most countries, the percentage drop was steeper in Q2CY’25, following the imposition of the tariff.

Canada remained the largest steel supplier in H1 but saw shipments fall 23.6% y-o-y to 2.21 mnt. In Q2, volumes stood at 0.90 mnt, a drop of 31.8% q-o-q and 37% y-o-y.

Brazil followed with 1.77 mnt in H1CY’25, down 3.9%. In Q2, exports to the US fell 29% q-o-q and 11.0% y-o-y to 0.73 mnt.

South Korea shipped 1.24 mnt (-8.3% y-o-y) in H1CY’25 and 0.64 mnt in Q2. The latter was down 6.3% q-o-q and 14.3% y-o-y.

Mexico’s exports contracted by 17.2% to 1.15 mnt in H1. In Q2, exports plunged by 52.6% q-o-q and 42.2% y-o-y. This marks the sharpest fall among the leading exporters to the US.

Taiwan and Germany posted growth of 16.1% and 19.4% y-o-y, respectively, to 0.54 mnt and 0.43 mnt in H1. In Q2, both regions recorded slight increases in volumes to the US q-o-q and y-o-y.

Commodity-wise trends – finished flats drive decline

Among the various commodities imported, finished flat steel remained dominant in H1CY’25 at 6.48 mnt but was down 15.9% y-o-y. Imports totalled 3.07 mnt in Q2, down 10% q-o-q and 23% y-o-y.

Galvanised steel imports saw the steepest drop of 32.6% to 1.55 mnt in H1. The same in Q2 stood at 0.67 mnt, reflecting a decline of 24% q-o-q and 47% y-o-y.

Hot-rolled coil (HRC)/plate arrivals fell 23.4% y-o-y to 1.14 mnt in H1, while cold-rolled coils (CRCs) declined 13.4% to 0.55 mnt. HRC/plate imports decreased by 21% q-o-q and 28% y-o-y to 0.50 mnt in Q2. Additionally, CRC volumes slid by 23% q-o-q and 28% y-o-y to 0.24 mnt.

The only flat steel category that witnessed an increase was pipes and tubes, whose imports climbed up by 5% to 2.42 mnt in H1CY’25. Q2 also registered an uptick of 14.2% q-o-q and 6.6% to 1.29 mnt.

Finished long products were steady at 1.97 mnt in H1CY’25, with rebar up 7% to 1.24 mnt and structures down 7% to 0.52 mnt. On Q2 basis, finished longs were down by around 9% q-o-q and y-o-y.

Semi-finished steel imports rose modestly by 3.8% to 2.06 mnt in H1, indicating targeted procurement of feedstock. However, in Q2, imports totalled 0.89 mnt, down 24% q-o-q but stable y-o-y.

Stainless steel volumes were broadly unchanged y-o-y at 0.32 mnt in H1.

Outlook

US steel trade data for H1CY’25 confirms that protectionist US policies have reduced import volumes, though not to an extreme degree.

Notably, a month-wise analysis shows that although imports fell 31% m-o-m to 1.34 mnt in April, May witnessed a sharp 49% rebound to 2.00 mnt. June volumes were down m-o-m at 1.72 mnt but largely stable against 1.74 mnt in the year-ago period.

As such, it may be slightly premature to expect a steady downtrend throughout the rest of the year. There will be some ups and downs, while full-year volumes are likely to settle moderately lower y-o-y.

Another arena in which the tariffs have been somewhat effective is crude steel production, which the US was able to increase by 1% to 40 mnt. For comparison, in CY’24, US crude steel output dipped 2.4% to 79.5 mnt. US steelmakers seem eager to have the tariffs continue, with the industry yet to achieve the 80% capacity utilisation goal prescribed by the Commerce Department in 2018.

Consequently, in the near term, there may be little chance of the US granting new tariff exemptions to close partners such as Canada or Mexico without significant concessions, given President Trump’s firm negotiating style. This is also attested to by the fact that the EU and Japan have not received exemptions. The protective stance is expected to persist well into 2025, sustaining the risks and pressures currently affecting global steel flows.

Leave a Reply