- Iranian domestic tags rise amid production disruptions

- Chinese export pressure, US tariffs limit price uptrend

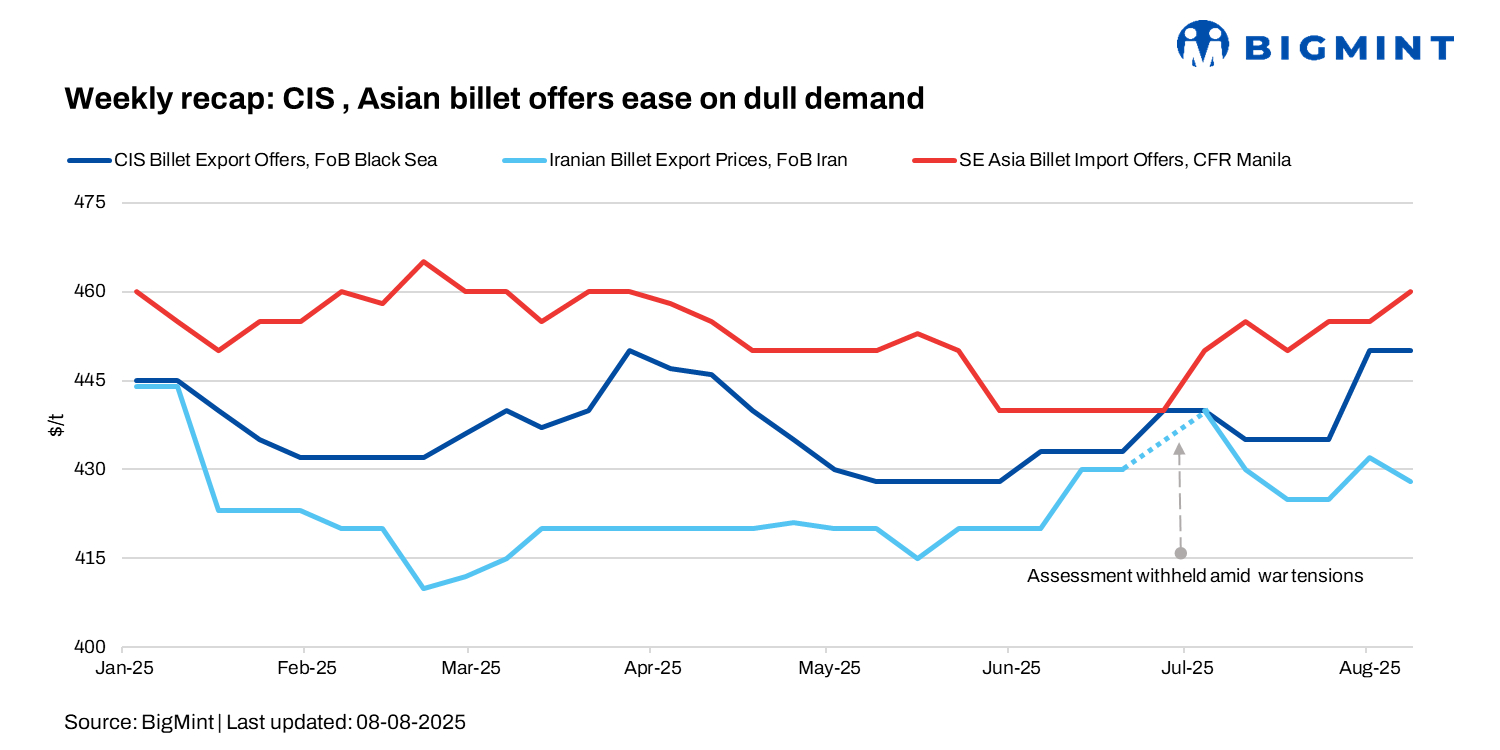

Billet prices across major markets showed mixed trends last week, with Russian and Chinese tags sliding w-o-w due to subdued demand. Additionally, the Iranian market experienced mixed trends. Iranian export offers edged lower by $4/t, while domestic prices rose.

Other regions such as Turkiye, India, and the Philippines were mostly stable w-o-w, while Nepal recorded a drop of around $14/tonne (t) w-o-w.

Globally, prices appear to have found a floor, but Chinese export pressure and US tariffs capped any sharp upside. Domestic supply constraints continued to lend support to Iranian local billet prices despite the marginal dip in export values.

Chinese and Malaysian billets for the October shipment were quoted at around $485-490/t CFR, but they were deemed too high for the Turkish market.

As per BigMint’s assessment, Turkiye’s deep-sea scrap market saw limited activity this week, with US-origin HMS 80:20 averaging $347/t CFR, almost unchanged from last week’s $346/t. US and Baltic-origin cargoes were assessed at $345-350/t CFR, while EU-origin ones were traded at $339-343/t CFR.

Both mills and suppliers remained on the sidelines amid weak finished steel demand, currency volatility, and cautious sentiment. Trading was minimal as mills processed earlier bookings, while financial strain at some producers, including Alter Iron and Steel, further weighed on activity.

Market highlights

Iran’s billet prices extend gains w-o-w

Iran’s billet market posted a steady rise this week despite broader economic challenges. Billet prices increased by 11,000 rial/kg w-o-w to 325,500 rial/kg, while rebar remained unchanged w-o-w at 385,000 rial/kg.

On 4 August, billet prices surged 8,000 rial/kg to 322,500 rial/kg, supported by tightening supply as power outages disrupted industrial and household goods production. Limited billet and slab availability kept sentiment firm.

By 6 August, billet prices added another 3,000 rial/kg to 325,500 rial/kg, while rebar held unchanged at 385,000 rial/kg.

Market participants attributed the gains to ongoing electricity and water shortages that curtailed mill output, alongside cautious buying as traders expected further supply constraints.

Export offers were at $425-430/t FOB for billet, down by $4/t w-o-w, $405-410/t FOB for slab, and $400-405/t exw for rebar.

Black Sea billet prices under pressure

Export prices of billets from the Black Sea continued to slide this week amid weak buying interest and fluctuating Chinese offers.

Russian medium-sized mills offered billets at $450-455/t FOB Black Sea, down from $455-460/t last week, with further cuts likely due to sluggish demand and competition from lower-priced Chinese material.

In Turkiye, both local and exported billet suppliers were active, but only small lots of domestic material were traded at $500-510/t exw for August shipment. Imported Russian billets for September shipment were offered at $455-460/t CFR Turkiye ($430-435/t FOB).

BigMint assessed Russian billets at $450/t FOB Black Sea, stable w-o-w. CIS-origin offers held at $465/t CFR Turkiye.

In Egypt, CIS billet offers stood at $460-465/t CFR for Russian-origin material. In Asia, Russian billet prices held steady at $410-420/t FOB Far Eastern ports.

China billet prices inch down by RMB 20/t ($3/t)

Steel billet prices in Tangshan fell by RMB 20/t ($3/t) w-o-w to RMB 3,070/t ($427/t, including VAT) as of 8 August. The week began with a sharp drop on 4 August, before a mid-week rebound pushed prices to RMB 3,100/t ($432/t).

The recovery was supported by a rally in coking coal futures — driven by rumours of production controls — which lifted steelmaking costs and improved sentiment.

However, towards the weekend, prices slipped again, as sluggish demand and steady raw material costs weighed on buying activity. Mills focused on output cuts rather than raising finished steel prices, capping any sustained uptrend.

Leave a Reply