- Mills raise HRC list prices on improved global sentiment

- Rebar inventory at Tier-1 mills falls slightly against end-Jul’25

- Induction furnace steel prices show mixed trends across regions

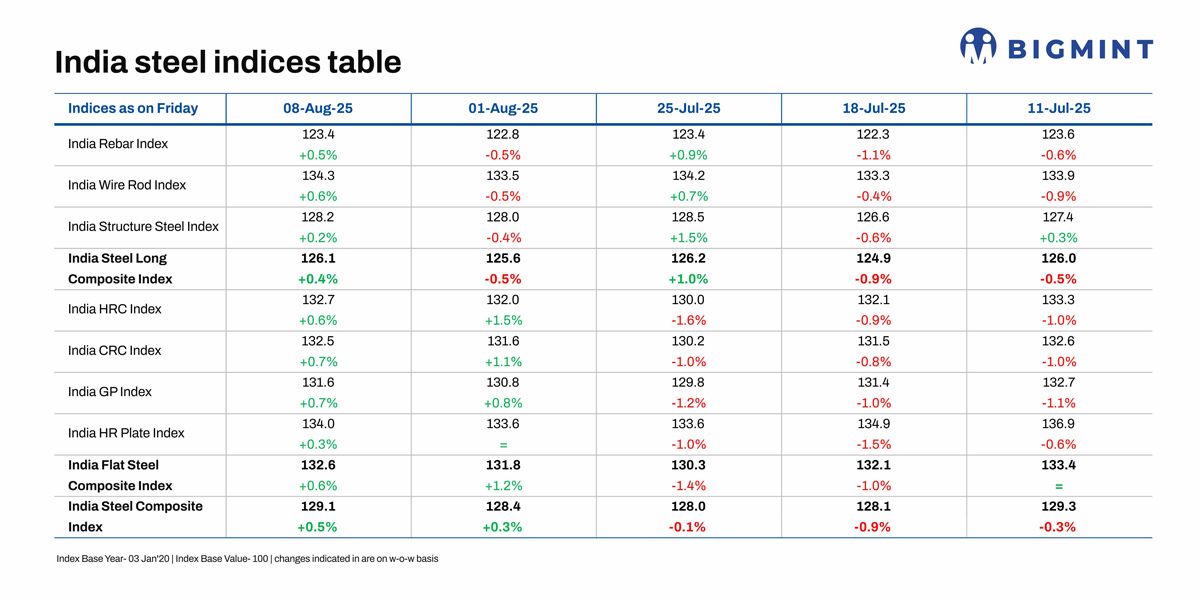

Morning Brief: BigMint’s India steel composite index, which tracks domestic steel market movements, continued its steady recovery in the second week of August 2025, edging up by 0.5% w-o-w. The index inched up on gradual improvement in market sentiments and with mills hiking their list prices for August.

While the flat steel composite index moved up by 0.6% w-o-w, the longs index showed slower growth of 0.4%. After rising for two weeks in succession, domestic steel prices seem to have recovered some lost ground since July.

Analysis of price movements

Mills hike flat steel prices: Leading Indian steel manufacturers have officially raised the list prices of HRCs and CRCs by INR 1,000-2,000/t ($11-23/t) for August sales as compared to the net sales price of end-July.

In the trade market, BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) held stable w-o-w to INR 50,200/t ($573/t) on 8 August. CRC (IS513, Gr O, 0.9 mm/CTL) prices held stable w-o-w at INR 57,000/t ($651/t) on Friday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Prices increased as global market sentiments improved. The India hot-rolled coil (HRC, S275) export index rose by $5/t w-o-w to $540/t (FOB main port), supported by improved global sentiment and higher Chinese export offers. This upward movement in Chinese prices lent support to domestic sentiment.

Steel prices also rose following NMDC hiking iron ore prices for August by up to INR 450/t.

The HRC market continues to see healthy demand, with prices remaining stable. Moreover, buying interest is expected to stay firm until mid-August, ahead of the holiday break. There is no supply shortage, with adequate material availability in the market, sources informed.

Coated flats prices up: The domestic coated steel market witnessed a price increase for both GP (galvanised plain) and PPGI (pre-painted galvanised iron) in the week ending 7 August. The INR 500/t w-o-w hike in prices reflects near-term optimism and limited supply pressures.

Rebar prices increase: The primary mills increased rebar prices by up to INR 2,000/t ($23/t) for early-August deliveries as against end-July, sources informed. Rebar inventories at Tier-1 mills increased over 45% m-o-m in early-August as against early-July. Meanwhile, inventories have dropped by 5% from end-July levels as mills liquidated material in the projects segment.

General anticipation of a surge in construction activities with the gradual receding of monsoon, as well as positive property registration data in key markets propelled rebar prices amid an overall recovery in the steel market.

IF rebar sees mixed trends: Induction furnace-route rebar prices witnessed mixed trends. Buying activity was largely limited to immediate requirements. Manufacturers preferred to either adjust trade discounts or reduce prices to encourage sales. Inventory levels stood at around 8-12 days, although this varied region-wise. Additionally, the lifting of previously booked materials was smooth.

Outlook

The hike in steel prices reflects near-term optimism and limited supply pressures, but market chatter suggests that any sustained price support will depend on actual improvement in downstream demand. Some sources indicated that if buying remains limited or inventory builds up, prices could witness downward adjustments in the coming weeks, although the general feeling is that prices will improve further towards mid- and end-August.

Of course, a lingering worry remains due to the continued inflow of steel imports. India’s bulk imports of HRCs touched 111,748 t as of 7 August, based on vessel line-up data. Around 261,045 t of additional cargoes are expected by late-August. India’s bulk HRC import volumes stood at 484,879 t in July as against 322,329 t in June.

The coming days will prove whether the market is in a position to absorb the recent hikes announced by the leading mills or whether downstream weakness will continue to weigh on steel prices.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply