- Odisha expected to witness 6% y-o-y growth in production

- PSU miners have ambitious expansion targets in FY26

- JSW sole major miner which might record a decline in output

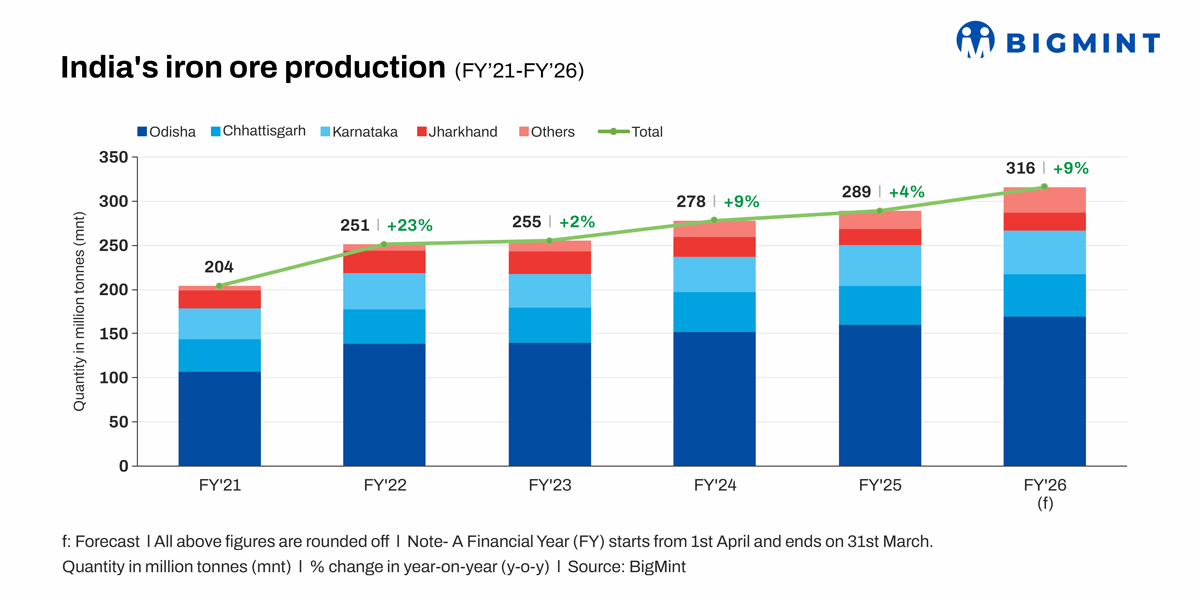

Morning Brief: Iron ore production in India is expected to reach around 315-316 million tonnes (mnt) in financial year 2025-2026 (FY26), a growth of 9% y-o-y from 289 mnt in FY25, as per BigMint calculations. The expected additional supply of 27 mnt in FY26 owes entirely to the capacity enhancement approvals accorded to both PSU and private miners in the country.

Iron ore production in the first half of 2025 witnessed a slight uptick of 3% y-o-y to reach 158 mnt. In the current fiscal, around 74 mnt of iron ore has been produced in the country.

Iron ore production is increasing due to the phenomenal surge in steelmaking capacity and demand in the country. Projections show that crude steel output in FY26 is expected to reach around 167 mnt, an increase of 10% y-o-y. While hot metal production is likely to touch around 104 mnt in FY26 compared with 91 mnt in FY25, DRI production is expected to reach nearly 60 mnt.

Therefore, iron ore production has to increase rapidly to keep pace with burgeoning domestic steelmaking needs.

Top miners

NMDC, the country’s No.1 miner in terms of volumes, has a target of 55 mnt of production in the current fiscal, although our estimation is around 50 mnt. Production was affected in FY25 after a loss of 45 days of operations due to strikes and labour problems. The company stopped short at 44 mnt in FY25, failing to reach its target of 50 mnt.

NMDC’s production has increased by 33% in the first four months of FY26 compared to the same period last year. This growth is expected to result in an additional 5-6 mnt of supply this year.

In order to achieve its target of 100 mnt by 2030, the miner has applied for EC in Bailadila for around 55 mnt and 17 mnt in Karnataka. NMDC has applied for EC of around 7 mnt for deposit 4 of Bailadila which is under NCL (an NMDC-CMDC JV) and deposit 13, where the EC needs to be transferred to NMDC, which is for another 13 mnt, CMD Amitava Mukherjee informed during the FY25 investor’s call.

The other leading PSU miner OMC is expected to raise production by an additional 4 mnt in FY26 to 40 mnt. The miner has witnessed a surge in capacity post transfer of non-operational auctioned mines – Guali and Jilling – following the mineral auctions in 2020.

Through the MDO mode, OMC intends to raise production from Blocks A and B of the Gandhamardan mines, the peak rated capacity of which is 9.47 mnt. The miner has applied for expanding the Guali mine to 30 mnt/year, while Jilling will be enhanced to 10 mnt/year.

Among the other major miners, Tata Steel is expected to achieve total production of 39 mnt in FY26 and the operationalization of the 2.95 mnt Kalamang mine and later the 10 mnt Gandhalpada mine won in auction will be key to the company’s strategy of attaining 60 mnt of production domestically to feed its expanding steel production targets.

Moreover, the NINL and Usha Martin mines are now with Tata post acquisition, which will also be crucial, as the other legacy mines come up for auctions in 2030.

Only JSW Steel is expected to see a decline in production after the surrender of the Jajang mine. Moreover, delay in operationalization of auctioned mines due to forest clearances, etc. is affecting the company’s production.

On the other hand, Rungta Mines is likely to raise production by 4 mnt after its Sanindpur mines in Odisha received an EC to increase production to 22.9 mnt/year from 19.7 mnt. This, along with strong production from its Oraghat mines, will help it raise output.

Lloyds Metals has received (EC) to expand its capacity from 10 mnt to 26 mnt, and is expected to contribute an additional 8 mnt of output in FY26.

State-wise projections

Odisha, India’s top iron ore producing state, is expected to see a 6% surge in output to 169 mnt in FY26. In Odisha, 84 mnt was mined in H1CY25 against 88 mnt in the year-ago period, reflecting a slight 4% drop. This was because OMC recorded a 15% y-o-y drop to 20 mnt, primarily because of elevated iron ore inventories at the beginning of the fiscal year, which prompted the miner to adjust its production strategies, as well as a change in the MDO model and weak steel prices.

Both Karnataka and Chhattisgarh are expected to churn out roughly 49 mnt in FY26, while Maharashtra will likely witness an increase of 7 mnt in production, thanks to the expansion being undertaken by Lloyds.

Even Goa’s output is set to rise after Vedanta commenced mining operations at the Bicholim mineral block. Goa’s production increased to around 1 mnt in H1CY25 compared to nil in the corresponding period of 2024.

Leave a Reply