The Indian coal market was stable this week. Portside South African and Indonesian coal prices held largely firm amid limited August availability and growing interest for September shipments. Domestic coal remained supported by tight supply from SECL. Although demand from the sponge iron and cement sectors remained slow, traders expect improved buying post-monsoon. Notably, sponge iron prices remained range-bound w-o-w due to the monsoon. Export offers for South African coal edged up on continued freight firmness.

Indonesian coal prices hold steady despite tight low-GAR supply

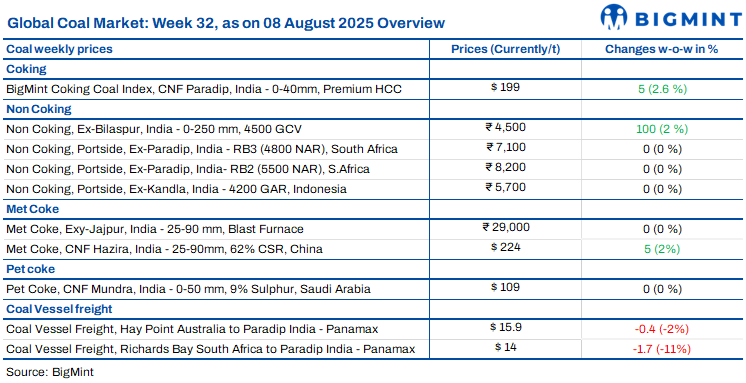

India’s portside market for Indonesian thermal coal stayed broadly stable w-o-w as of 8 August 2025. BigMint assessed 5000 GAR at INR 7,150/t at Kandla and INR 7,050/t at Vizag, while 4200 GAR remained at INR 5,700/t and INR 5,600/t, respectively. Only 3400 GAR at Navlakhi rose INR 50/t to INR 4,450/t on tight supply. Indonesian freights eased, but power plant stocks fell to 52.96 mnt, keeping sentiments mixed.

South African coal steady; Sep’25 bookings set the tone

South African RB2 thermal coal offers held firm w-o-w at INR 8,100/t exw-Gangavaram, while RB3 eased INR 50/t to INR 7,000/t. Offers reflected September delivery sentiment, as August cargoes were mostly booked. Around 5,000 t of RB3 were traded at INR 7,200/t from Mangalore and 8,000 t at INR 7,000/t exw-Paradip. Stocks fell 3.4% to 14.27 million tonnes (mnt). Export offers were up by $0.5-1.5/t w-o-w; domestic coal and sponge iron markets showed mixed signals.

Domestic coal prices firm on lower SECL supply

Domestic coal prices remained firm w-o-w as SECL supply stayed constrained amid monsoon disruptions. BigMint assessed 5000 GCV at INR 5,000/t exw-Bilaspur, unchanged from last week, while 4500 GCV rose INR 100/t to INR 4,500/t. SECL’s reduced e-auction frequency and positive response in recent auctions lent support to prices despite weak overall demand. Traders expect continued firmness until supply conditions improve post-monsoon.

BigMint’s coking coal index edges up in recent deal

BigMint’s PHCC index rose to $199/t CNF Paradip as of 8 August 2025, up $5/t w-o-w, backed by a recent deal for 25,000 t of Australian GYC. Market sources placed Australian PHCC at $197-200/t and Canadian at $180-185/t CFR. Indian met coke prices stayed supported, while Chinese prices firmed up on strong steel demand. Seaborne PHCC offers held at $183/t FOB amid tight vessel availability and sustained Asian buying.

Indian met coke sentiment improves; prices may rise soon

India’s met coke market showed early signs of bullishness, supported by rising coking coal and Chinese met coke prices. Domestic BF-grade coke stayed flat at INR 29,000/t in the east, while western prices inched up to INR 30,000/t. Tight supply, delayed imports, and higher seaborne coal costs are lifting sentiment. A weaker rupee and steady pig iron rates further supported prices. An uptick is likely in the near-term until imports arrive in September.

Imported pet coke prices hold steady amid weak demand

Imported pet coke offers in India stayed unchanged w-o-w. US-origin cargoes were quoted in the $110-120/t CFR range, while Saudi-origin ones stood at $109-111/t. Demand remained quiet due to monsoon disruptions impacting construction. However, with freights holding firm and expectations of improved infrastructure activity post-monsoon, cement makers may ramp up bookings in September for October deliveries, potentially supporting price sentiment in the coming weeks.

Coal freights soften amid slow fixtures

Coal freights to India from South Africa, Australia, and Indonesia slipped further this week, with the sharpest drop seen on the South Africa-Paradip route, now assessed at $14/dmt. Fixtures remained limited as buyers, especially sponge iron players, held back due to weak domestic sentiment. A SAIL booking from Australia to Vizag was done at $16.95/dmt for early September. Meanwhile, port delays and monsoon disruptions continued to weigh on demand, keeping the market subdued in the near term.

Leave a Reply