- Billet prices rise by INR 500/t w-o-w

- Trade in finished steel improves in recent days

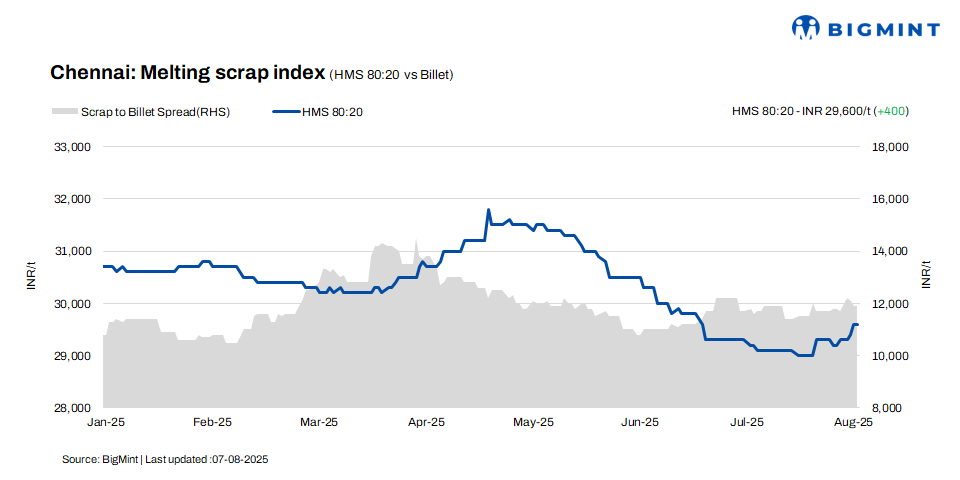

In Chennai, HMS (80:20) scrap prices saw a w-o-w increase of INR 400/t, reaching INR 29,600/t, though prices remained stable d-o-d. Steel billet prices rose by INR 500/t w-o-w, stabilising at INR 41,500/t. Rebar prices also saw a w-o-w increase of INR 200/t, reaching INR 45,700/t, while remaining unchanged d-o-d.

The slight rise in prices of key raw materials and steel products in Chennai, particularly HMS scrap, billet, and rebar, reflects a stable yet positive trend in market conditions. The ongoing improvements in trade activity suggest a strengthening of demand for both semi-finished and finished steel products.

Imported, domestic price trends

According to a scrap trader, imported shredded scrap offers are currently at $365-370/t, with buyers bidding between $360-365/t. HMS 80:20 scrap is priced at $335-340/t. However, despite these competitive offers, the demand for imported scrap remains subdued as buyers are increasingly turning to cheaper domestic options.

Domestic HMS (80:20) scrap prices are currently ranging between INR 29,500-30,000/t for buyers making immediate payments. For transactions with extended credit terms, prices have risen to INR 30,000-30,500/t. The majority of offers fall within the INR 29,500-30,500/t range, with most deals being concluded at these levels, reflecting the current market pricing structure.

Buyer-supplier sentiments

According to market sources, sponge iron supply is currently constrained, with many major producers choosing to retain the material for self-consumption instead of selling into the merchant market. A significant sponge producer has also undergone a maintenance shutdown. On the other hand, billet trade activity has seen an uptick, although the market faces supply shortages. Rebar demand has similarly improved in recent days.

HMS (80:20) scrap prices in the domestic market are currently ranging from INR 29,500 to INR 30,500/t, with minor fluctuations based on payment terms, according to a local scrap supplier. Meanwhile, both billet and rebar markets have experienced consistent demand and pricing improvements in recent days. Domestic scrap remains more competitively priced than imported alternatives, leading mills to prioritize local material. This trend supports a more cost-effective procurement strategy for mills in the current market environment.

Regional comparison

In the Jalna market of western India, billet and HMS 80:20 prices dropped by INR 100/t, reaching INR 40,300/t and INR 31,100/t, respectively. Rebar prices witnessed a decline of INR 200/t to INR 44,100/t. Trade activity in finished steel remained slow in today’s session. On a positive note, mills are receiving better raw material flows, supported by recent price increases that have bolstered procurement confidence.

Outlook

As demand for semi-finished and finished steel continues to improve in the region, market participants are maintaining an optimistic outlook on the steel sector’s performance in the near term. Despite the ongoing preference for domestic scrap over imported alternatives, the positive sentiment in the steel market is likely to support a gradual upward movement in scrap prices.

However, any price increases are expected to remain within a limited range due to the relatively higher cost of imported scrap compared to domestic.

Leave a Reply