- Market sentiments remain sluggish

- Baltic dry bulk index weakens w-o-w

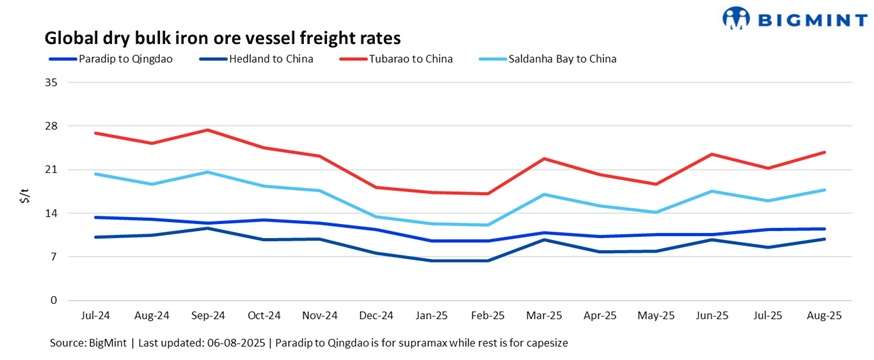

Dry bulk iron ore freight rates witnessed drop across major routes this week, except the India-China corridor.

Freight rates in the Asia-Pacific Supramax market remained rangebound with a softer note this week, amid subdued trading activity in the Pacific basin. While fresh cargoes emerged from Indonesia, most market participants adopted a cautious, wait-and-watch stance, seeking clearer direction. Meanwhile, bunker prices edged lower from the previous session, adding mild downward pressure on rates.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freight rates for Supramax vessels from the Indian Ocean to China remained at $11.50/dry metric tonne (DMT), stable w-o-w. A few deals of low grade Fe 57% fines were concluded from Odisha last week, hence fixtures remained limited.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China inched down to $9.8/DMT, marking a w-o-w decrease. A few fixtures of Australian miners were concluded in the past week.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freight rates for Brazil-to-China shipments fell w-o-w, settling at $23.8/DMT. There was a lack of activity in the throughout the week, with no reported fixtures concluded.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Freight rates from Saldanha Bay to Qingdao also inched down by $0.3/DMT w-o-w, settling at $17.7/DMT. The drop was attributed to easing of logistical issues at South African ports, which had disrupted operations in the previous week.

Market highlights:

- Baltic index drops w-o-w: The Baltic Exchange’s main sea freight index, which tracks rates for dry bulk carriers, declined w-o-w on 05 Aug 2025, driven by weaker demand across all vessel segments. The overall index dropped w-o-w by 74 points to 1,921, with the Capesize index falling 180 points to 3,006 on a weekly basis. Meanwhile, the Supramax index inched up by 8 points to 1,279.

- China’s iron ore spot prices rangebound w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $102/tonne (t) CFR China on 05 Aug, stable w-o-w. Prices have recovered this week after dropping last week. Prices rose due to sustained downstream activity and the upcoming holiday. The iron ore market remained resilient with firm demand for Sept’25 cargoes, as restocking efforts boosted the outlook.

- DCE iron ore futures inch up: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Sept 2025 contract stood at RMB 795/t ($111/t) on 05 Aug.

Outlook

The dry bulk iron ore freight market faces an uncertain outlook in the near term due to weak demand, seasonal disruptions, and limited trading activity.

Leave a Reply