- Bhutan offers rise INR 7,000/t ($80/t)

- Chinese prices remain steady

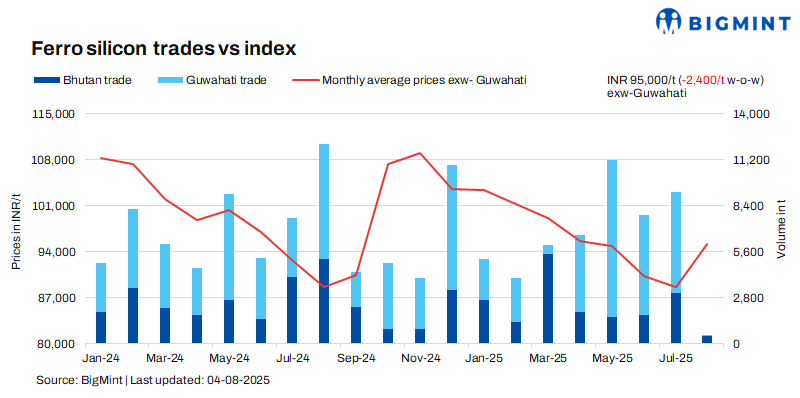

Indian ferro silicon (70%) prices experienced a drop of INR 2,400/t ($27/t) on 4 August 2025 in comparison to the assessment on 28 July. Prices came down following Bhutan’s price announcement of INR 95,000/t ($1,082/t) exw for this month and resumption of operations of Meghalaya plants.

Ferro silicon prices in India were INR 95,000/t ($1,082/t) exw-Guwahati, as per BigMint’s assessment on 4 July. In Bhutan, prices came down by INR 3,400/t ($39/t) w-o-w to INR 95,000/t ($1,082/t) exw. Around 650 t of deals were reported in both the regions last week in the price bracket of INR 95,000-98,000/t ($1,082-1,116/t) exw.

Market recap (29 July-4 August)

Prices drop w-o-w but rise m-o-m: Bhutan continues to be a major influence for Indian sellers particularly in the North east for determining prices. For this month, it stood at INR 95,000/t ($1,082/t) exw, a rise of INR 7,000/t ($80/t) m-o-m.

Following a brief and temporary shutdown of Meghalaya plants last month, there was a lack in clarity for prices and it had reached INR 100,000/t ($1,139/t) exw levels. However, buyers resisted those prices and hence new prices were lower than it.

But since anticipation had already built up for the prices to rise and with ongoing dispute between Meghalaya Power Distribution Corporation Limited and Meghalaya sellers, Bhutanese sellers decided to raise prices. A key seller from Bhutan was quoted as saying to BigMint, “We are open to selling at a higher rate if the opportunity arises. However, at present, we are not considering a lower rate unless the market shows signs of resistance.”

South India’s price trends: Sellers in South India too aligned their offers accordingly and were in the price bracket of INR 95,000-98,000/t ($1,082-1,116/t) exw.

Slight drop in silicon metal prices: Prices of imported silicon metal from China (grade 553, Si:98.5%) stood at $1,470/t CFR Mundra on 4 August, a slight drop of $15/t w-o-w.

Chinese prices held firm w-o-w: Ferro silicon (Si: 75%) prices inched up slightly by RMB 30/t ($4/t) w-o-w to RMB 5,760/t ($802/t) exw-Inner Mongolia. Operating rates in some production areas increased slightly, but overall output recovery remained limited.

Weak demand from steel mills kept transactions focused on need-based buying. The steel sector remained in a seasonal downturn, with reduced hot metal output further lowering alloy demand. Trading activity was cautious, and spot liquidity stayed low.

Outlook

As prices for August have just been announced, in the coming days not much of a variation is expected.

Leave a Reply