- High-CV coal prices rise amid supply tightness

- Mid and low-CV coal indexes decline

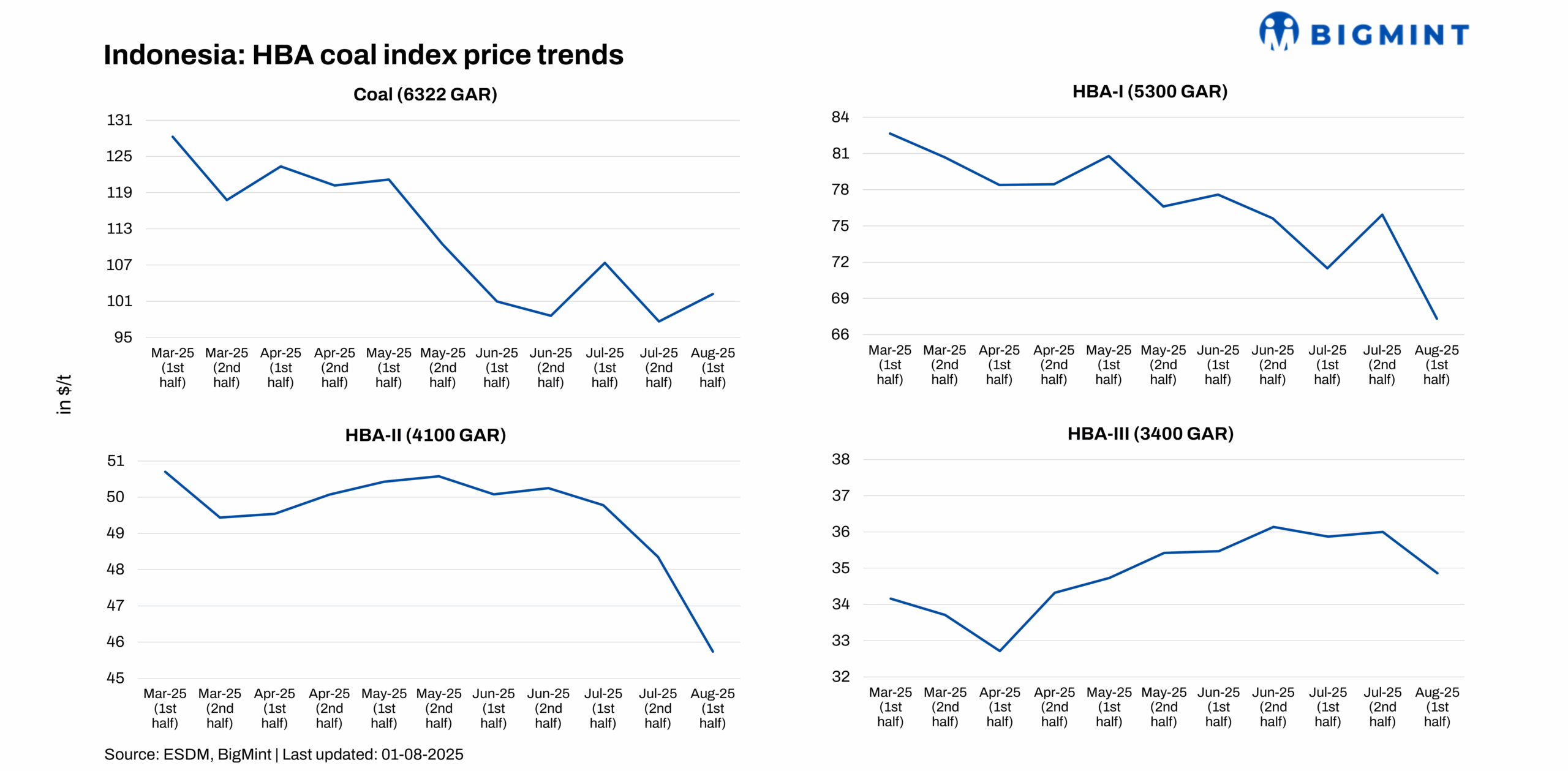

The Indonesian Ministry of Energy and Mineral Resources (ESDM) has published its revised Harga Batubara Acuan (HBA) for the first half of August 2025, highlighting contrasting price movements across different grades of thermal coal.

The adjustments reflect evolving market dynamics, with high-calorific value coal registering an upward price revision, while mid- and low-grade variants witnessed notable declines.

High-calorific coal sees uptrend

The benchmark price for Indonesia’s highest-grade thermal coal (6,322 kcal/kg GAR) rose to $ 102.22/t, marking a 4.6% increase compared to the second half of July.

The price rise signals firming demand for high-energy coal, likely supported by supply-side disruptions and selective procurement by import-dependent countries seeking higher combustion efficiency.

Sharp correction in mid-calorific coal prices

In contrast, the benchmark price for mid-range thermal coal (5,300 kcal/kg GAR), referred to as HBA-I, registered a sharp decline of 11.3%, settling at $ 67.33/t. This marks the lowest price level for this grade since March 2025.

The drop reflects subdued buying interest from key Asian markets, amid soft power demand, elevated inventories, and seasonal factors limiting consumption.

Low-calorific coal benchmarks continue to slide

Lower-calorific value coal grades also experienced downward pressure. The HBA-II price for 4,100 kcal/kg GAR coal fell by 5.3% to $ 45.74/t, these prices are also the lowest since March, suggesting continued cautious buying from utilities and industries amid weak end-use demand. While the HBA-III price for 3,400 kcal/kg GAR coal declined by 3.1% to $ 34.86/t.

Market sentiment and strategic implications

The revised HBA prices underscore a widening gap between high and low grade coal, indicating stronger demand for premium coal amid shifting regional needs, supply disruptions, and evolving energy policies. As market volatility persists, traders, utilities, and producers are likely to rely on HBA benchmarks to guide procurement strategies and pricing decisions.

Outlook

High-CV coal prices are likely to remain supported by supply constraints and targeted import demand, while mid- and low-CV segments may stay under pressure amid weak regional demand and high inventories. Market participants are expected to adopt a cautious approach, tracking demand trends and policy shifts closely.

Leave a Reply