- Alternate raw material prices remain steady

- Finished steel prices gain 100/t d-o-d

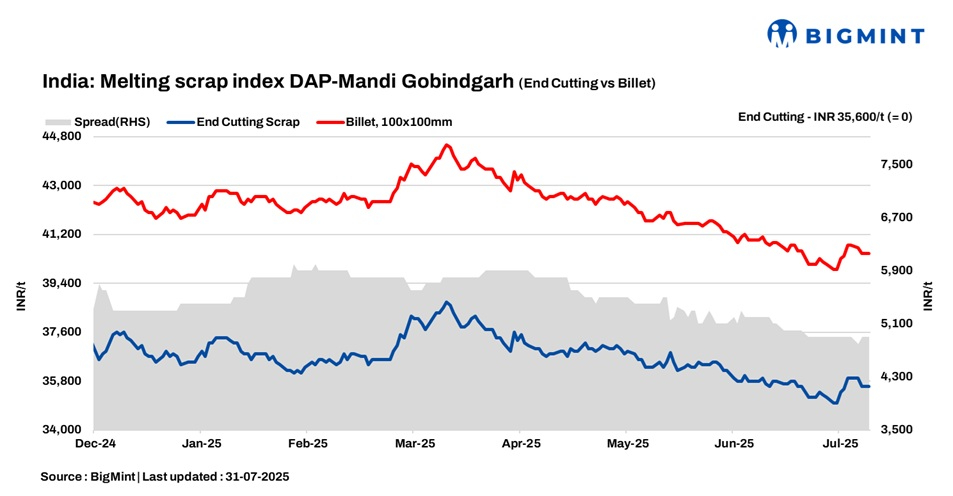

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, remained from the two consecutive days and assessed at INR 35,600/t DAP on 31 July 2025. No any price fluctuation seen in todays scrap market as buying remained moderate by mills over all steel makers hoping for some positive steel market trend in upcoming month.

A local mill owner reported that weekly operations averaged just 2-3 working days, with buying activity remaining below moderate levels throughout the week. As a result, steel prices in Mandi Gobindgarh stayed range-bound, reflecting the subdued demand.

The region is currently experiencing monsoon-related disruptions, leading to slight delays in scrap arrivals. Additionally, labour availability issues have further minor impacted operational efficiency at several units.

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh remained firm on a d-o-d basis, holding steady at INR 30,000/t DAP. Similarly, pig iron prices in Ludhiana (Punjab) showed no movement, maintaining levels at INR 36,000/t DAP.

Market sources indicate that raw material prices have remained largely stable over the past few days, reflecting balanced supply-demand conditions .

Steel market trends

Steel ingot prices in Mandi Gobindgarh declined by INR 100/tonne, settling at INR 40,500/t DAP. The semi-finished steel market across major trading hubs remained largely range-bound, with prices showing minor fluctuations. While some regions saw a marginal dip of INR 100-200/t, others witnessed slight gains of INR 200-300/t, reflecting a mixed market sentiment.

In contrast, rebar (Fe500) prices registered a modest rise of INR 100/t, currently quoted at INR 45,500/t ex-works. The uptick comes in response to price hikes announced by primary mills in finished steel categories a day earlier, which has influenced short-term buying sentiment in the spot market.

Uptrend in scrap auctions across major auto clusters

Scrap auctions conducted during the current week across major auto manufacturing hubs in India witnessed a notable price improvement of approximately INR 1,000/t to 2,000/t on a m-o-m basis. The rise is attributed to selective restocking by secondary mills and improved demand anticipation post-monsoon.

Significant transactions were recorded from locations such as Nashik, Chakan, Pune, Pantnagar, Sanand, and Becharaji, involving various grades like CA GA profile, profile end cuts, and CR-HR mixed scrap.

On 29th July, Nashik saw around 2,300 t of CA GA profile scrap traded at INR 40,900/t ex-works, while Chakan witnessed 1,100 t of profile end cuts sold at INR 33,000/t ex-works.

CR-HR mixed scrap volumes ranged between 500-750 t, with prices varying from INR 33,400/t to INR 36,300/t ex-works across hubs like Pune, Pantnagar, and Sanand.

Earlier in the week, smaller lots were auctioned from regions such as Becharaji and Nashik, with CA GA profile scrap reaching INR 41,500/t ex-works.

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $335-340/t, which equates to approximately INR 31,983/t (including freight). HMS (80:20) prices in Mumbai rose by INR 100/t to INR 30,700/t DAP today. Indicative prices of shredded from Europe stood at $368/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,800/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply