- Limited policy support weighs on Iranian market

- Russian offers remain stable, SE Asia tags climb up

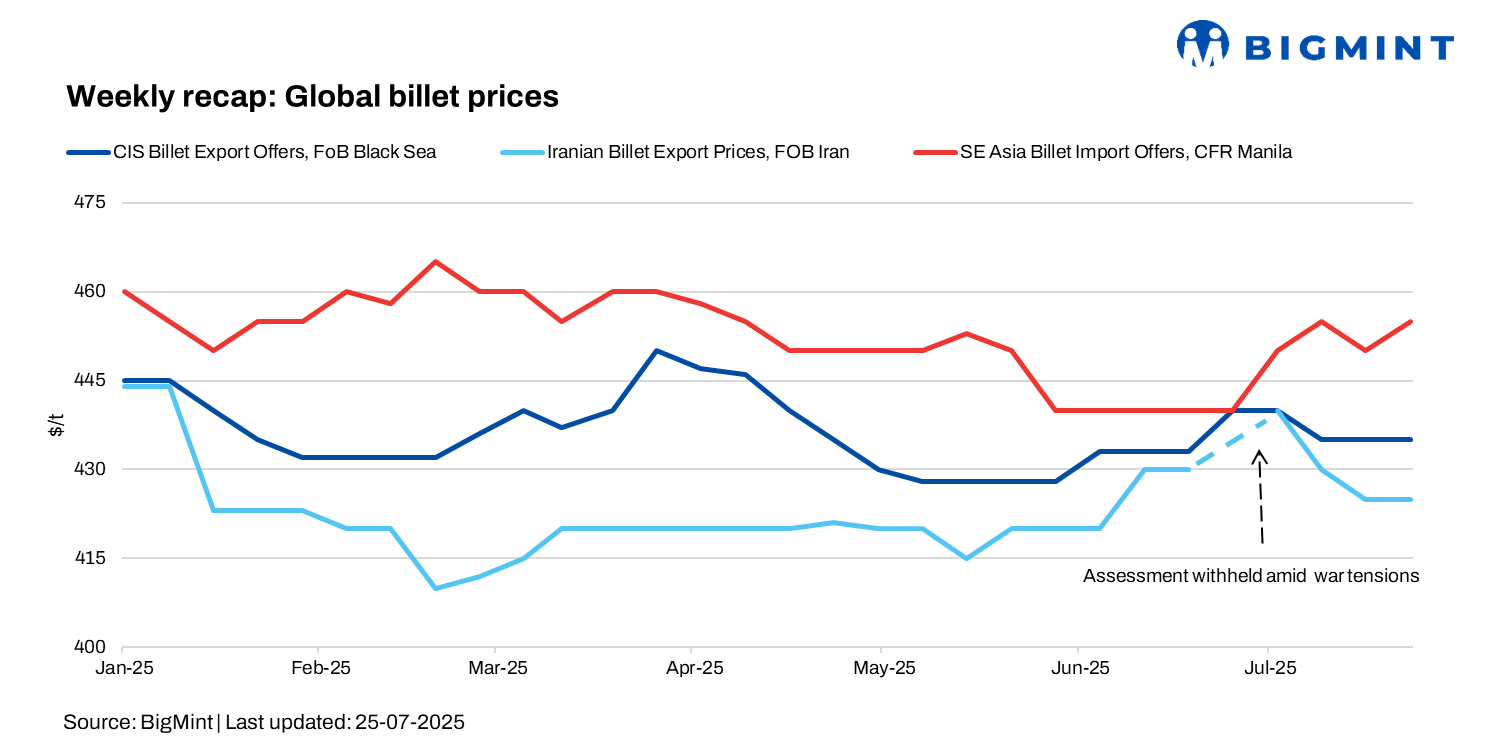

In the 30th week of 2025, the global billet market saw moderate demand and some trading activity, though buying remained cautious across regions.

Turkish mills raised domestic billet offers following Chinese price hikes. China’s billet export offers were heard at above $450/tonne (t) FOB this week, but Asian buyers were cautious, deeming regional offers as unworkable.

As per BigMint’s assessment, the Turkish imported scrap market was flat with US-origin HMS 80:20 at $346/t CFR, down $1/t w-o-w as mills completed August bookings. Sellers held firm offers for September cargoes, at above $350/t CFR, expecting better finished steel demand. About 9-10 deals were heard. The rebar-to-scrap spread was tight at $185-190/t, with rebar offers at $530-535/t.

Market highlights

SE Asia offers for 150×150, 3SP billet rose to $455-460/t CFR Philippines as of 25 July, but buying interest was limited. Some small quantities could have been traded at these levels, though no confirmed deals were heard.

Vietnamese steelmaker Hoa Phat priced billets at $465/t and rebars at $512/t for its latest September shipments.

Iran‘s steel market continued to struggle amid weak demand and stagnant policy support, keeping billet and rebar prices largely range-bound. The domestic market remained under pressure, while the industry pushed for reforms to boost exports and manage oversupply.

As of 23 July, billet prices stood stable at 309,500 rial/kg, while rebar held firm at 375,000 rial/kg. Export offers were assessed at $415-430/t FOB for August shipments, mostly via traders, slightly down from last week’s $420-430/t, reflecting limited buying interest and squeezed margins.

Recently, a tender was floated for 30,000 t of billet exports, due on 31 July for October shipment. Meanwhile, other mills failed to secure their desired prices.

As per market insiders, trading activity in Iranian billets remained weak; however, optimism in Asia may encourage suppliers to test higher offers. While exports to Iraq and Afghanistan continued, demand was tepid amid ongoing power cuts and geopolitical uncertainties.

Recently, a notable volume of Iranian billets was sold to Pakistan on a FOB basis, supported by the recent duty cut to 5%.

Rebar prices remained at breakeven, curbing mill profitability. Slabs were offered at $405-410/t FOB and rebars at $430-435/t exw, unchanged w-o-w.

BigMint assessed Russian billets at $435/t FOB Black Sea, stable w-o-w. CIS-origin offers were held at $455-460/t CFR, with some Iranian billets traded to Turkiye this week.

Chinese billet prices rise w-o-w

Tangshan billet prices rose RMB 50/t ($7/t) w-o-w to RMB 3,160/t ($441/t incl. VAT) as of 25 July, supported by higher coking coal costs and capacity cut speculation. Despite a mid-week dip of RMB 30/t ($4/t) amid profit booking, sentiment stayed firm on stimulus hopes, stock market gains, and lower inventories.

Leave a Reply