- Imports from South Korea, Japan – key exporters – decline

- Domestic consumption rises in Jan-Apr’25, output decreases

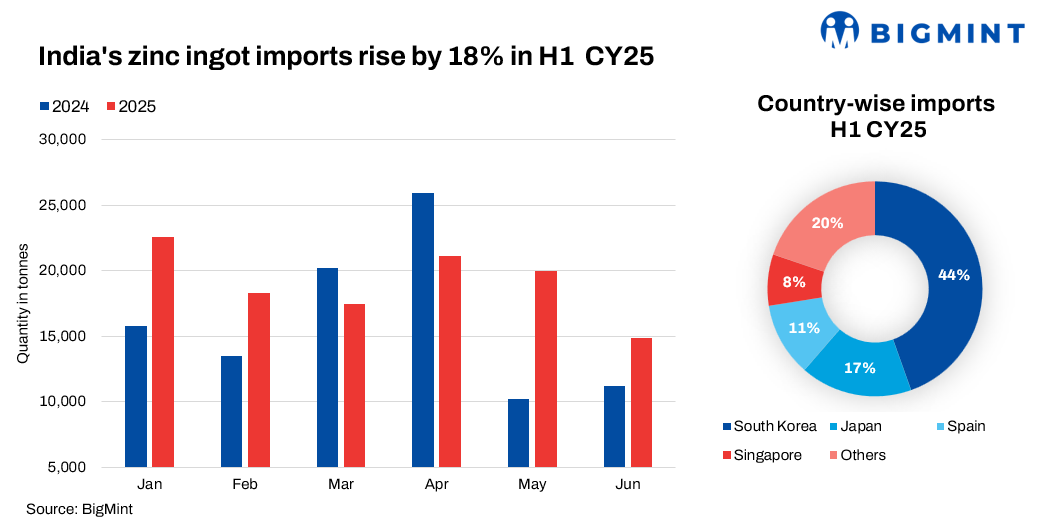

India’s zinc ingot imports witnessed an 18% increase to 114,203 tonnes (t) in H1CY’25 (January-June 2025) from 96,715 t in H1CY’24, driven by restocking demand and lower global prices. However, more prominently, India’s sourcing patterns shifted, with key exporters — South Korea and Japan — recording steep drops in shipments despite overall growth in the country’s arrivals.

Notably, March and April 2025 saw strong inflows at 17,479 t and 21,084 t respectively, reflecting improved buying from galvanisers and alloy makers. In contrast, import volumes in H1CY’24 were impacted by higher domestic output and cautious procurement amid volatile zinc prices.

India sees shift in import sources

India’s zinc ingot imports from South Korea, though still the largest, dropped to 50,878 t in H1CY’25 from 59,705 t in H1CY’24, a decline of 8,827 tonnes or 14.8%, due to destocking and lower refinery dispatches.

Japan, the second-largest supplier, saw a steeper fall of 32.1%, with volumes reducing from 28,304 t to 19,234 t, largely because of maintenance shutdowns and weak auto-sector demand.

Other new or rising contributors include the United Arab Emirates (rising to 1,210 t from 349 t), Norway (new with 1,488 t), and Finland (new with 1,098 t).

These shifts indicate a structural diversification in India’s sourcing strategy, with growing reliance on European and Middle Eastern origins, driven by price advantages and shifting trade routes.

Zinc ingot production dips in Jan-Apr’25

India’s zinc ingot production declined by 1.7% y-o-y to 286,000 t in January-April 2025, while apparent domestic zinc consumption strengthened by 0.9% y-o-y to 293,000 t. Monthly production was largely stable at around 74,000 t in January-March, although volumes fell to 63,000 in April.

However, export volumes moderated by 4.2% y-o-y to 71,200 t, while imports rose 6.3% to 78,000 t. This shift indicates robust domestic demand.

Notably, April 2025 recorded lower exports (15,972 t), possibly signalling improved domestic offtake. The overall trend points to a consumption-driven market recovery in early CY’25.

Conclusion

India’s zinc ingot import landscape in H1CY’25 reflects a clear shift toward diversified, short-term sourcing, with growing contributions from Europe, the Middle East, and non-traditional hubs. Despite reduced overall volumes, strategic re-routing and opportunistic buying indicate adaptability to global price trends and subdued domestic demand.

Leave a Reply