- Slow rebar sales, holidays curb demand from Turkiye

- Tariff uncertainty keeps market sentiment divided

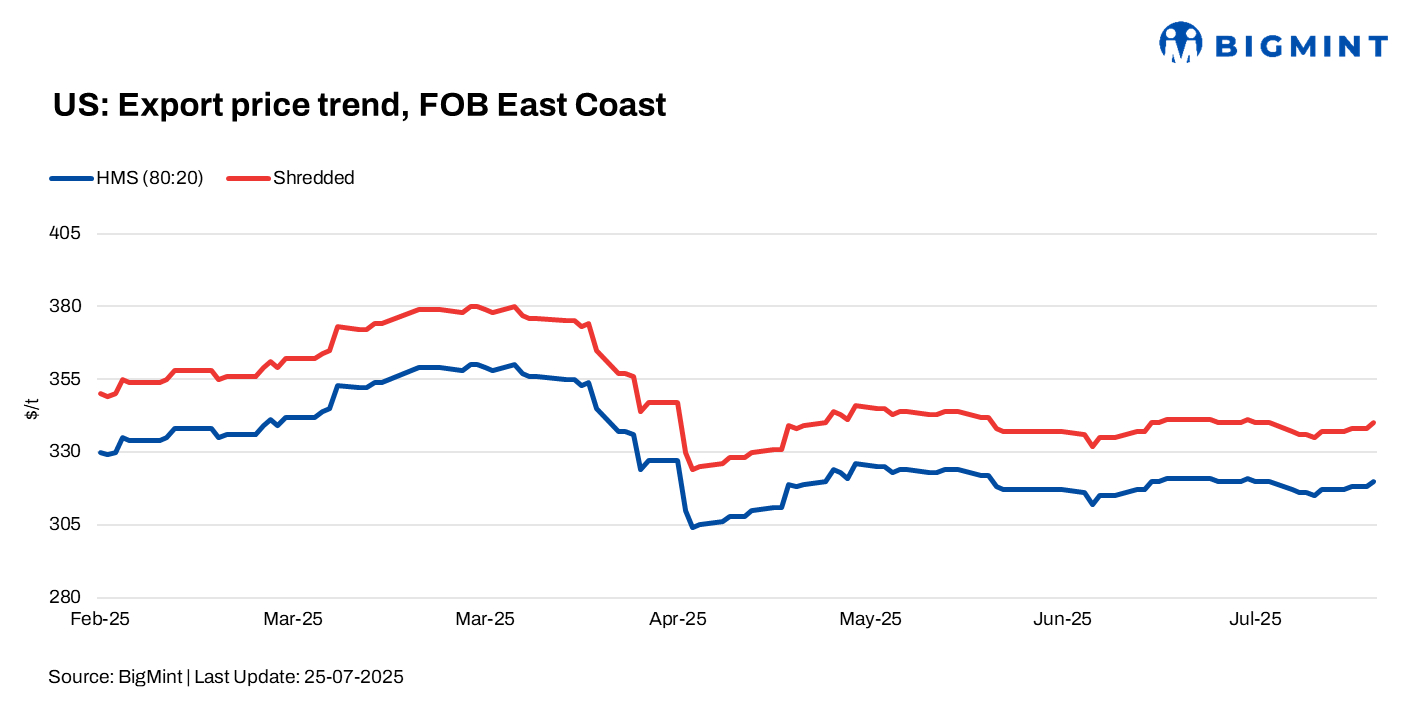

US ferrous scrap export prices edged up by $3/tonne (t) w-o-w, despite lingering uncertainty in the domestic market. The export segment remained under pressure from subdued demand, especially from South Asia, where a monsoon-led slowdown in construction activity dampened steel trades.

Additionally, falling hot-rolled coil (HRC) prices reduced scrap offtake, while the upcoming 50% tariff on Brazilian pig iron imports in early August created uncertainty. However, expectations remain that scrap demand may rise as US mills shift from pig iron to prime scrap.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $320/t, up by $3/t w-o-w.

- Shredded – $340/t, up by $3/t w-o-w.

Updates on key importers

Turkiye: Demand for US-origin scrap in Turkiye remained limited, with only a few deals heard, as deep-sea prices held at around $347/t CFR and mills exercised caution amid weak steel demand.

Factors weighing on Turkish buying interest

- The mid-July national holiday in Turkiye slowed market activity.

- Sluggish rebar sales made mills hesitant to pay beyond $345/t CFR.

- Higher US offers at $352-353/t CFR faced resistance amid cheaper European alternatives.

Turkish buyers were largely inactive, European-origin cargoes, offered at $337-340/t CFR, remained more competitive, further dampening appetite for US scrap.

Bangladesh: Demand for US-origin HMS 80:20 scrap in Bangladesh remained weak, with prices steady w-o-w at $351/t CFR. Mills were largely inactive in the import market, as persistent monsoon rains continued to hinder construction activity and suppress steel demand.

Most buyers stayed on the sidelines due to limited consumption, delaying raw material bookings. A few mills remained active, but most waited for clearer market signals before making new purchases.

Vietnam: Vietnam saw a further dip in demand due to ongoing monsoon-related disruptions and weak rebar demand kept mills largely inactive. With sufficient scrap inventories and low production levels, buyers held off on new purchases, awaiting clearer signals from the domestic steel market.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – down by $1/t w-o-w at $346/t.

- Vietnam – down by $3/t w-o-w at $335/t.

- Bangladesh – stable w-o-w at $351/t.

Outlook

Market sentiment remains mixed, with some pockets of cautious optimism. Certain scrap sellers expect tariff-driven supply disruptions to lift prices in the near term. Additionally, the decision to impose a 50% tariff on Brazilian pig iron imports may improve scrap demand and, by extension, boost pricing.

However, others remain cautious, uncertain about the long-term enforcement of the tariffs and wary of soft export fundamentals.

Leave a Reply