- Coking coal index drops as mills wrap up Aug’25 restocking

- South African coal prices rise following rail disruptions

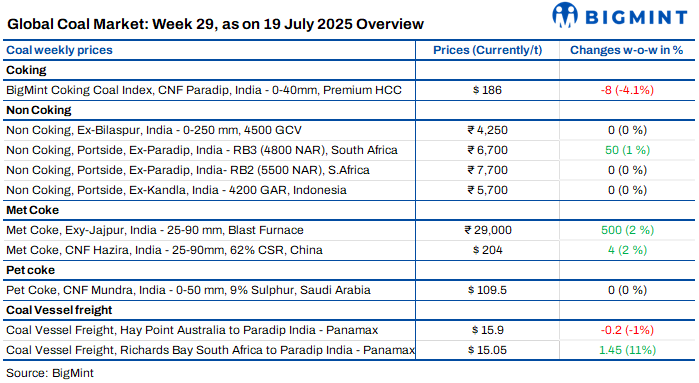

The Indian coal market remained subdued this week. While supply disruptions supported South African offers, overall demand was weak. Portside inventories remained firm, and domestic trade lacked momentum. Buyers preferred to wait, limiting fresh bookings. The sponge iron segment also softened slightly, reflecting sluggish industrial activity. Traders are likely to remain cautious until stronger demand signals emerge.

South African coal prices edge up

Portside prices for South African coal inched up amid disruptions in rail movement and RBCT maintenance, with RB2 at INR 7,650/t and RB3 at INR 6,650/t exw-Gangavaram. Offers stayed volatile, but weak buying interest capped gains. Portside stocks held steady at 15.84 mnt as arrivals matched offtake. Sponge iron prices dipped INR 700/t w-o-w to INR 24,800/t as earlier bookings weighed on buying. Looking ahead, South African supply tightness may lend some support, but high domestic availability and muted industrial demand may limit any sharp rise. Traders remain cautious, waiting for firmer cues from end-user sectors.

Indonesian thermal coal prices steady at ports

Indonesian thermal coal prices stayed flat at Indian ports as monsoon delays and muted demand kept activity subdued. 5000 GAR held at INR 7,150/t (Kandla) and INR 7,050/t (Vizag), while 4200 GAR stood at INR 5,700/t and INR 5,600/t, respectively. Freight to Navlakhi rose to $15.58/t amid vessel tightness. Port stocks neared 15.84 mnt, barely changing w-o-w. Power plant stocks fell to 58.52 mnt, with 12 sites critically low. International prices showed mixed cues. Near-term prices are likely to remain stable unless post-monsoon demand revives.

Domestic coal prices steady

Domestic coal prices stayed flat this week, with 5000 GCV and 4500 GCV assessed at INR 4,700/t and INR 4,250/t exw-Bilaspur. Market activity remained slow as buyers refrained from new bookings. However, in SECL’s latest auction, a few high-grade lots received decent bids, while most grades hovered near notified prices. Supply stayed steady, and end-user demand remained subdued.

Coking coal index slips $8/t

BigMint’s premium hard coking coal (PHCC) index dropped to $186/t CNF Paradip on 18 July, down by $8/t w-o-w. Indian steelmakers have mostly secured cargoes for August loadings, with fewer spot trades seen. A few Australian-origin deals were concluded at $183-188/t CFR. Canadian offers stood at $175-180/t, but no trades were heard. Weak domestic steel prices and sufficient coal supply weighed on buying interest. Meanwhile, Indian met coke prices inched up INR 100-500/t, while Chinese coke prices rose on tight supply. However, India’s HRC and CRC prices declined up to INR 800/t amid weak demand.

Met coke prices rise slightly, imports drop

Met coke prices in India picked up slightly this week due to stable steel demand and tight global supply. As of 16 July, BF-grade met coke was assessed at INR 29,000/t ex-Jajpur, up by INR 500/t. Prices in Gandhidham rose modestly to INR 29,100/t. India’s met coke imports dropped 9% y-o-y to 2 mnt in H1CY’25, owing to government QRs and good domestic supply. While steel prices stayed flat, demand for foundry-grade pig iron grew in western India. Meanwhile, China may raise coke prices amid supply cuts, even as Australian PHCC dropped $5/t w-o-w to $173/t FOB.

Indian imported pet coke offers stable

Imported pet coke offers remained steady w-o-w at $110-112/t CFR (US-origin) and $109-111/t (Saudi-origin). However, some quotes reached $114-118/t as rising freight costs pushed up landed prices. The increase in freight rates is due to monsoon-related route disruptions and rough sea conditions. Despite unchanged market fundamentals, freight pressure is making high-end offers more common in spot discussions.

Freight trends mixed, Baltic index climbs

Dry bulk coal freight rates to India showed mixed movement this week. Australia-India Panamax rates slipped $0.2 to $15.9/DMT, while South Africa-India rose $1.45 to $15.05/DMT due to vessel shortage at RBCT. Indonesia-India Supramax rates gained $1.47 to $15.58/DMT on tight supply. However, India’s coal demand remained dull due to rains, with non-coking coal imports in H1CY’25 dropping 4% y-o-y to 89 mnt. In June alone, imports fell 14% m-o-m. Meanwhile, the Baltic index hit a one-month high at 1,906 as Capesize rates firmed, though Panamax and Supramax segments moved unevenly.

Leave a Reply