- Rising FFA rates, monsoons trigger freight hikes

- Baltic index climbs to its highest level in a month

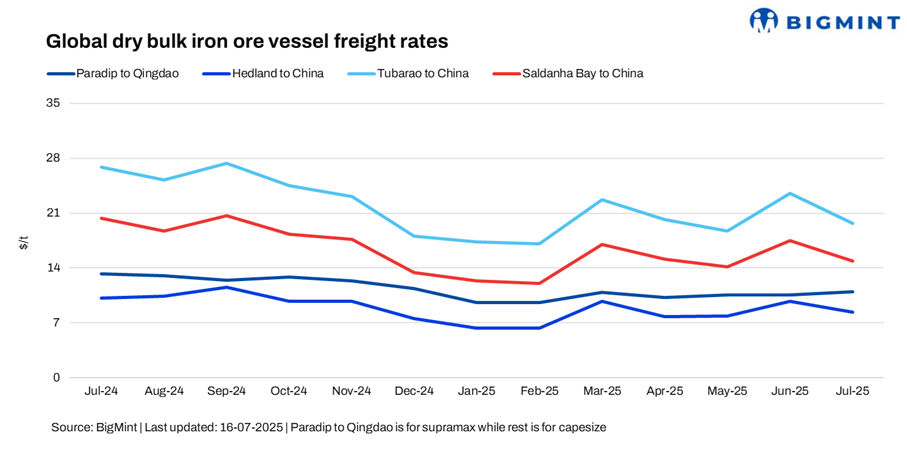

Dry bulk iron ore freight rates recorded a notable surge this week, reflecting improved market sentiment and stronger cargo demand. Vessel hiring activity picked up across key routes, with freight rates on the India-China, Australia-China, Brazil-China, and South Africa-China corridors registering w-o-w gains.

The increase was driven by a combination of firmer iron ore shipments from key global miners, tighter vessel availability in certain regions amid monsoons, and improved chartering activity — particularly in the Pacific and Atlantic basins. Market participants also noted increased enquiries from miners and traders, contributing to upward pressure on rates across major export hubs. “Monsoon always plays a role in India, leading to the deferral of some cargoes, which in turn is tightening vessel availability and pushing freight rates higher,” observed a source to BigMint.

Port disruptions amid the monsoon are tightening vessel availability, limiting the supply of prompt tonnage and pushing freight rates higher. A market participant told BigMint, “Adverse weather conditions in both China and India have caused vessel congestion at several key ports, with many ships currently stuck and facing delays.”

Furthermore, rising forward freight agreement (FFA) rates for both Capesize and Supramax segments have added to the upward momentum in vessel freights, BigMint understands.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freight rates for Supramax vessels from the Indian Ocean to China rose to $11.70/dry metric tonne (DMT), up by $0.7/DMT w-o-w. The rise was further supported by positive sentiment in the Indian low-grade iron ore export market, coupled with a w-o-w increase in global iron ore prices and gains in DCE iron ore and SHFE rebar futures during the week.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freight rates for iron ore shipments from Western Australia to China rose to $8.40/DMT, marking a w-o-w increase of $0.8/DMT. The increase was driven by active chartering from major Australian miners, such as Rio Tinto and BHP, who secured vessels to Qingdao at rates ranging between $7.45-8.40/DMT for end-July to early August 2025 laycans. This heightened activity significantly tightened available tonnage, sources informed by BigMint.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freight rates for Brazil-to-China shipments rose significantly by $2.4/DMT w-o-w, settling at $20.90/DMT. Approximately five fixtures were reported on the Tubarao-Qingdao route, concluded at rates ranging from $18.70-$21/DMT for end-July to early August 2025 laycans. Sources noted that, after a slow start, the market witnessed firmer activity with improved fixture levels.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freight rates from Saldanha Bay to Qingdao also increased by $1.9/DMT w-o-w, settling at $15.50/DMT. The increase was attributed to ongoing logistical challenges at South African ports, which have disrupted operations and tightened vessel availability.

Market highlights:

- Baltic index rises w-o-w on strength across vessel segments: The Baltic Exchange’s main sea freight index, which monitors rates for vessels transporting dry bulk commodities, rose w-o-w to its highest level in a month, supported by broad-based gains across all vessel segments. The main Baltic Dry Index, which tracks freight rates for Capesize, Panamax, and Supramax vessels, recorded a w-o-w increase of 83 points, reaching 1,866 on 15 July 2025. Leading the gains, the Capesize segment posted the sharpest rise, jumping by 166 points w-o-w to 2,533. Among the smaller vessel categories, the Supramax index also advanced, climbing 43 points w-o-w to 1,287.

- China’s iron ore spot prices remain firm w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $98/tonne (t) CFR China on 16 July 2025, up by $3/t w-o-w. Market sentiment remained buoyant, supported by a positive outlook and heightened trading activity. Robust demand for mid-grade fines further reinforced this optimism.

- DCE iron ore futures climb w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract increased by RMB 36.5/t ($5/t) w-o-w to RMB 773/t ($108/t) on 16 July. Meanwhile, prices inched up by RMB 6.5/t ($1/t) d-o-d today.

Outlook

The near-term outlook remains strong, as the ongoing monsoon in India continues to disrupt operations, leading to a shortage of available vessels. Additionally, the sustained rise in FFAs and the Baltic index, along with logistical bottlenecks at key ports, is expected to provide continued support to freight rates.

Leave a Reply