- Delayed infrastructure activity dampens mill sales

- Semi-finished, finished steel tags drop INR 100-400/t

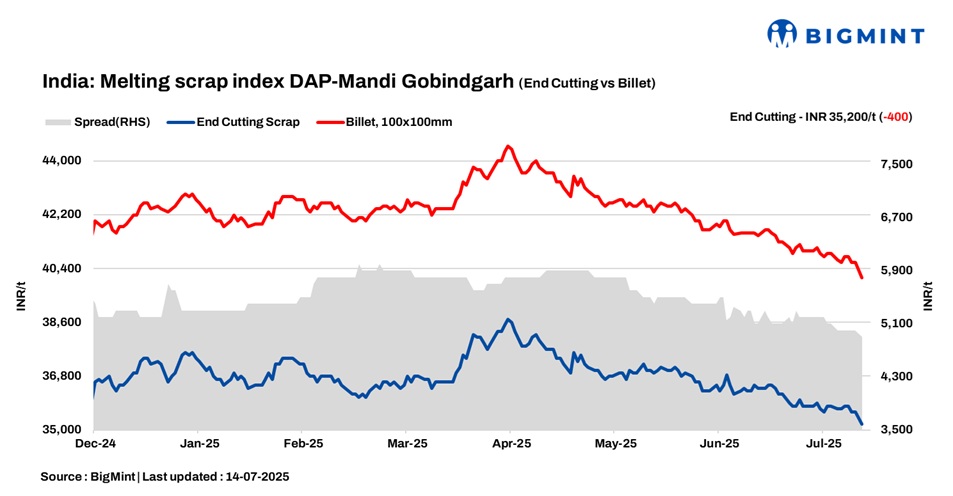

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, dropped by INR 400/tonne (t) d-o-d to INR 35,200/t DAP on 14 July 2025. Steel scrap prices in the region have tumbled to their lowest point in over four years, marking a significant downturn for the market. The last time prices hovered at this level was on 27 March 2021, underscoring the magnitude of the current decline.

This drop reflects mounting pressures from tepid demand, with industry participants closely monitoring the situation for signs of recovery.

Steel mills in the region are facing sustained pressure on both semi-finished and finished steel products, a trend that has persisted over the past few months. Several factors are contributing to this challenging environment:

- Demand from adjacent markets remains tepid, limiting opportunities for mills to offset local weaknesses through inter-state trade.

- Infrastructure-related projects in the region have experienced delays or slower-than-expected progress, reducing steel consumption and further dampening mill sales.

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh declined by INR 100/t d-o-d, settling at INR 28,700/t DAP. Steel-grade pig iron prices in Ludhiana have held steady at INR 35,200/t DAP for the past three working days, showing no change despite fluctuations in other steel markets

Steel market trends

In the Mandi Gobindgarh market, semi-finished steel prices registered a notable decline of INR 400/t d-o-d, closing at INR 40,000/t DAP. This downward movement mirrors the broader softness observed in the steel sector, with semi-finished prices across major trading hubs slipping by INR 100-600/t d-o-d. The most significant price correction was recorded in the Jaipur market, where semi-finished steel plunged by INR 600/t d-o-d.

Rebar (Fe500) prices in Mandi Gobindgarh declined by INR 100/t today, settling at INR 45,200/t exw. Rebar prices across key regions continued their downward trajectory, with declines ranging from INR 100-500/t d-o-d. The steepest fall was observed in the Hyderabad rebar market, where prices dropped by INR 500/t in a single day.

Overview of Alang market

On 14 July, Alang’s ship-breaking melting scrap prices showed no movement, with HMS (80:20) assessed at INR 31,600/t ex-yard, as per BigMint. Average trade activity and a steady stream of buying inquiries from Bhavnagar’s IF steel mills contributed to the price stability in the region.

Auction result

On 11 July, a major auto component manufacturer conducted a scrap auction at its Manesar plant in Haryana, offering approximately 1,100 t of CR busheling scrap. The auction concluded with bids closing at INR 34,000/t exy.

Last week, a major Indian multinational infrastructure company conducted an auction at its Hazira facility for Heavy Melting Scrap (HMS), successfully selling nearly 1,500 t. The scrap was offered in lot sizes ranging from 300 to 400 t, with final prices settling in the range of INR 33,000 to INR 34,000/t on an ex-works basis.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,800-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $330-335/t, which equates to approximately INR 30,963/t (including freight). Today, local HMS (80:20) prices in Mumbai remained stable at INR 30,500/t DAP. Indicative prices of shredded from Europe stood at $358-$360/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,150/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply