- Primary mills offer rebates on list prices

- Iron ore prices put up good show w-o-w

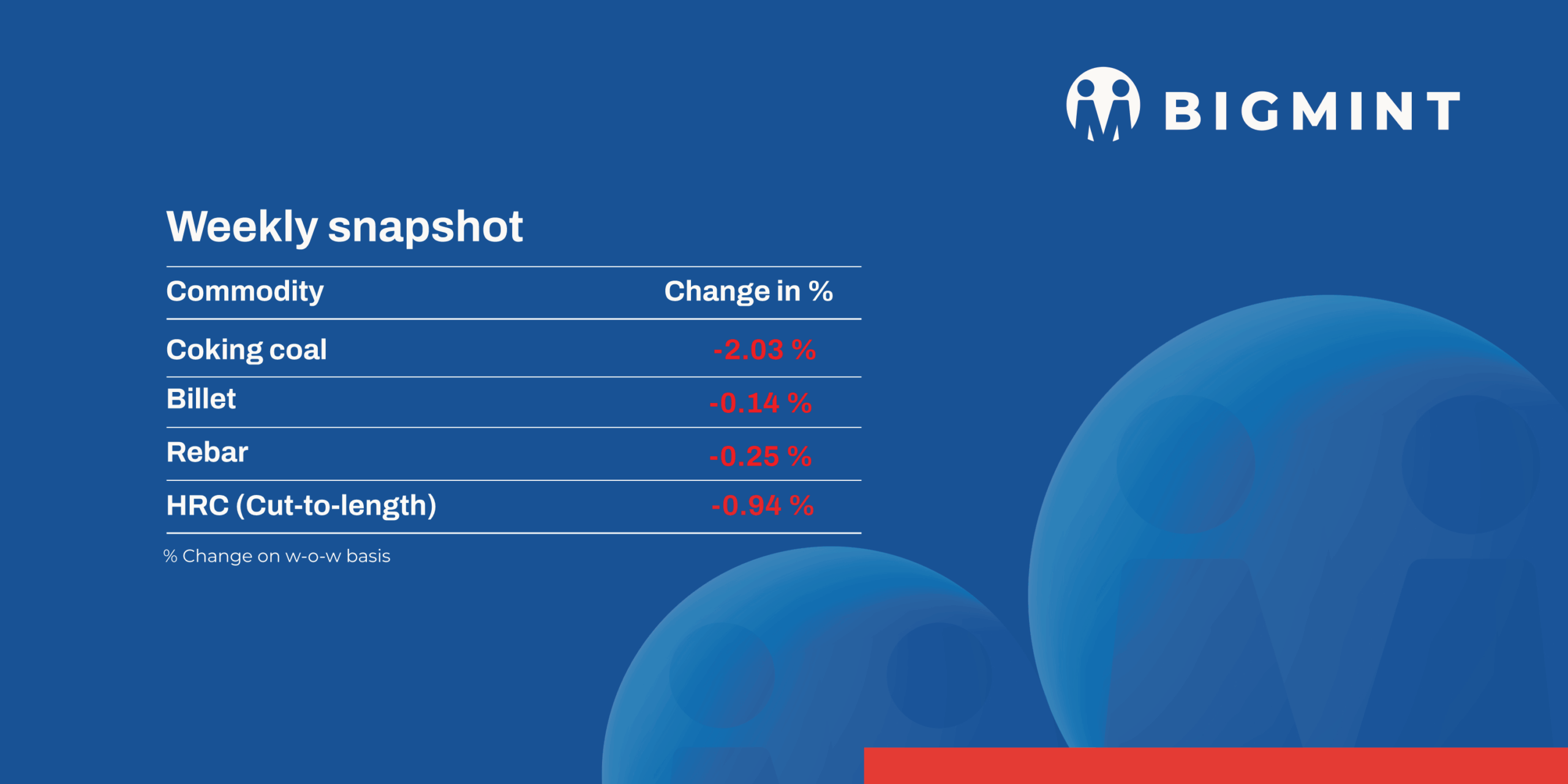

Indian semi-finished steel prices trended up w-o-w, with billet tags in most key locations increasing by INR 100-400/t. Meanwhile, trade-level blast furnace (BF) rebar prices dropped w-o-w amid subdued demand. Primary mills offered rebates/discounts on their list prices to spur buying interest.

Iron ore and pellets

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 400/t ($4.5/t) w-o-w to INR 9,300/t ($108/t) DAP Raipur on 11 July. Raipur-based pellet producers raised offers for Fe 62/63% (+/_0.5%) material by INR 400/t ($4.5/t) to INR 9,100-9,200/t ($106-107/t) exw this week. Around 80,000 t of pellets were sold in Raipur this week by local sellers.

- On 8 July, NMDC Donimalai’s auction saw full booking of 16,000-t lumps (10-40 mm, Fe 56%) at INR 3,480/t ($41/t) and 8,000-t fines (Fe 56%) at INR 2,842/t ($33/t). Similarly, the 9 July auction from the Kumaraswamy mines recorded sales of 64,000-t lumps (10-40 mm, Fe 57.46-62.68%) at INR 3,855-5,517/t ($45-64/t) and 92,000-t fines (Fe 57.8-58.85%) at INR 3,092-3,329/t ($36-39/t). All prices are on an ex-mines basis and include royalty, DMF, and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched up by $0.5/t w-o-w to $63/t FOB east coast on 10 July. Around 350,000 t of Fe57% fines were sold at $72-74/t CFR China in the last week. Furthermore, around 200,000 t of lower-grade (Fe54-55%) fines deals were recorded. This price rally comes on the back of positive macro-economic signals from China, which lifted the global fines market and supported higher trading activity in the Indian seaborne segment.

Coal

- Portside RB2 (5500 NAR) offers in India climbed up INR 200-300/t w-o-w, helped by firmer sponge iron prices and slight trader optimism. A small RB2 deal closed at INR 7,500/t exw-Krishnapatnam. Hike in sponge offers by around INR 200-800/t in different regions reflected in portside prices this week. Yet, portside stocks stayed steady at 15.92 mnt, while South African export offers moved up $0.5/t, reflecting mild external support. Domestic coal prices stayed flat; SECL auctions saw low volumes with limited buyer interest.

- Domestic coal prices held steady w-o-w, as per BigMint’s assessment, with 5000 GCV at INR 4,700/t and 4500 GCV at INR 4,250/t exw-Bilaspur. Market activity stayed muted, with random offers and hardly any fresh buying. SECL’s latest auctions offered lower quantities and saw limited participation, mostly from old buyers, reflecting weak industrial demand and continued cautious sentiment.

- BigMint’s PHCC index stood at $194/t CNF Paradip on 11 July, down $2/t from a week earlier. A west India mill booked 40,000 t of Australian PHCC at about $196/t CFR for end-August, but Canadian offers stayed softer at $175–180/t CNF. India’s coking coal imports rose 11% m-o-m to 6 mnt in June, driven by higher Australian shipments.

- India’s met coke market showed mixed moves this week as traders stayed wary ahead of new import quota news. As of 9 July, BigMint assessed BF-grade met coke at INR 28,500/t ex-Jajpur, up INR 500/t w-o-w, while Gandhidham prices held at INR 29,000/t.

Ferrous scrap

- India’s imported ferrous scrap market remained largely quiet throughout the week, with UK-origin shredded prices holding steady at $362/t, barely changed from $361/t in the previous week. Sentiment continued to be weighed down by weak steel demand, seasonal monsoon-related logistics challenges, and the availability of competitively priced domestic scrap.

- Shredded scrap offers were at around $360-365/t CFR, but buyers resisted paying above $355/t, maintaining a persistent bid-offer gap. Activity in HMS and busheling segments was also subdued, as mills increasingly preferred sponge for immediate needs.

- Approximately 8,000-9,000 t of imported scrap were booked into India last week, including HMS 80:20, HMS 60:40, LMS bales, HMS 1, turning scrap, and NTP bales. This included 6,000–6,500 t of HMS 80:20, booked at prices ranging from $335-355/t.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) surge to 4-month high w-o-w by INR 600/t ($7/t) w-o-w to INR 72,600-73,500/t ($846-856/t) in the key regions of Durgapur, Raipur, and Vizag. Rising silico manganese prices in India reflect tight supply conditions and a steady pick-up in steel sector demand, contributing to ongoing bullish sentiment.

- Ferro manganese: Indian ferro manganese (HC 70%) prices remained unchanged w-o-w at INR 71,900/t ($837/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also remained flat at INR 72,200/t ($841/t). Market cautiousness kept Indian ferro manganese prices steady despite stable supply and demand.

- Ferro silicon: Indian ferro silicon prices dipped by INR 200/t ($2/t) w-o-w to INR 86,800/t ($1,011/t) exw-Guwahati. Meanwhile, Bhutanese prices also decreased by INR 500/t ($6/t) to INR 87,000/t ($1,013/t) exw. Due to increasing imports of ferro silicon and silicon metal, sellers in Bhutan and northeast India lowered their prices to remain competitive in the market.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were flat w-o-w at INR 99,500/t ($1,159/t) exw-Jajpur. Market conditions stayed balanced, with no sharp fluctuations, and consistent trading activity kept ferro alloy prices steady through the week.

Semi-finished

- Indian semi-finished steel prices showed an increasing trend, as per BigMint’s assessment. Domestic billet prices in all key locations went up by INR 100-400/t. Meanwhile, regions like Raipur and Raigarh showed slight downtrend by INR 50-150/t. Sponge iron prices also showed an increasing trend in almost all key locations, moving up by INR 200-700/t. The highest increase was seen in Raigarh and Rourkela.

- Indian DRI export offers increased by $5/t at CPT Raxaul to $320/t while, CPT Benapole offers also increased by INR 14/t to $335/t.

- SAIL’s Rourkela Steel Plant (RSP) conducted an auction for 3,500 t of steel-grade pig iron on 11 July, in which the entire quantity was booked at an average price of INR 32,200/t exw. This shows an increase of INR 1,000/t compared to the previous auction on 1 July in which 7,100 t were sold at INR 31,200/t exw.

Finished long steel

- IF-rebar: India’s IF-route finished long rebar prices observed fluctuation this week. Purchases were mostly confined to urgent needs, prompting manufacturers to further reduce prices in an effort to stimulate sales. Inventory levels are reportedly hovering at around 12-15 days. To curb excess stock, many mills across regions have implemented production cuts of about 25-30%. Looking ahead, market players expect prices to stay subdued in the near term, largely due to muted project execution and sluggish construction activity during the ongoing monsoon season.

- On a weekly basis, rebar steel prices witnessed mixed response in the range of INR 100-700/t across regions except in Mumbai and Chennai markets where prices remained stable as per BigMint assessment.

- The trade reference price of the 10-25 mm Fe 500 grade rebar manufactured via the IF route was assessed at INR 39,100-39,500/t exw Raipur, and at INR 42,900-43,500/t exw Jalna.

- Trade reference prices of heavy structural steel channels of base size 150 mm stood at INR 41,800-42,200/t exw Raipur.

Trade reference prices of wire rod hovered at INR 40,800-41,300/t ex Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices continued their downtrend w-o-w, weighed down by sluggish domestic demand and muted market activity due to the onset of the monsoon. Suppliers expressed worry regarding the continuous free-fall in prices, and buyers also remained cautious, waiting for prices to stabilize.

- Trade-level BF rebar prices declined by INR 700/t w-o-w to INR 49,200/t exy-Mumbai, as per BigMint’s assessment on 11 July 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices declined w-o-w to INR 46,500-47,500/t FOR, owing to weak market sentiments. Buyers stayed on the sidelines, purchasing only for urgent requirements amid the continuous drop in prices.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India declined by INR 600/tonne (t) w-o-w to INR 49,500-51,500/t ($577-601/t) across markets. Moreover, cold-rolled coil (CRC) prices dropped by INR 900/t w-o-w to INR 55,500-59,800/t ($647-697/t).

- The ongoing monsoon has dampened demand across key sectors, resulting in a continued downturn in trade activity. Buyers are taking a cautious “wait and watch” approach, anticipating further price corrections amid weak market sentiment.

- India’s bulk imports of HRCs touched 81,903 t as of 5 July, based on vessel line-up data from BigMint. Around 249,194 t of additional cargo are expected by the month-end.

- BigMint’s India HRC (S275) export index held steady w-o-w at $545/t FOB. While a 40,000 t deal at $600/t CFR Antwerp for August offered some support, European demand remained subdued amid the summer lull. Indian mills stayed cautious on Middle East exports, citing better domestic realisations, competitive Chinese offers, and geopolitical risks.

Leave a Reply