- Falling finished steel demand prompts output cuts at mills

- Mills face pressure to reduce scrap procurement prices

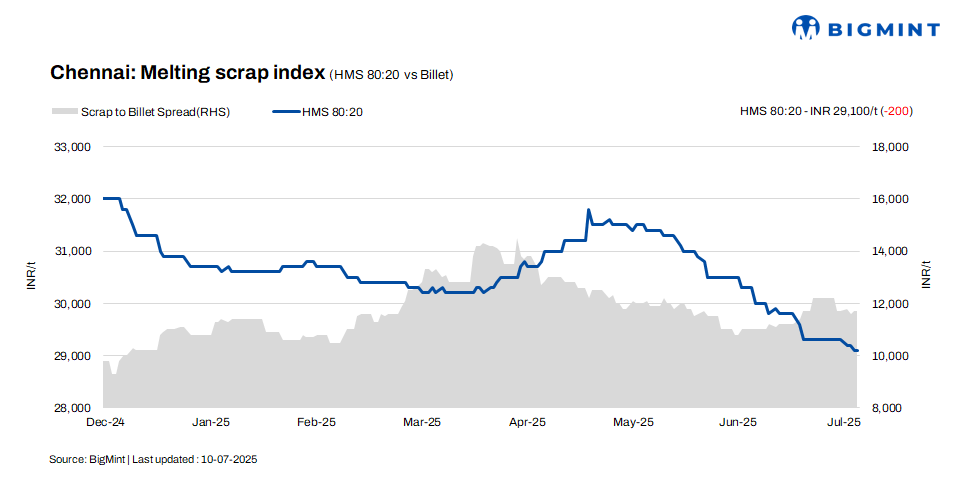

HMS (80:20) scrap prices in Chennai declined by INR 200/tonne (t) w-o-w to INR 29,100/t, with no d-o-d change, according to BigMint’s latest assessment. The w-o-w decline was due to weakened demand for finished steel.

Billet prices declined by INR 700/t on a weekly basis to INR 40,800/t, although they remained unchanged d-o-d. Rebar prices remained unchanged at INR 46,000/t on both d-o-d and w-o-w bases.

Imported, domestic price trends

A scrap trader noted that offers for shredded from Australia were quoted at $365-370/t CFR Chennai, while HMS (80:20) was priced at $340-345/t. Subdued demand for finished steel continued to dampen market sentiment. Additionally, with domestic scrap currently priced lower than imported alternatives, mills showed limited interest in securing overseas bookings.

In Chennai, domestic HMS (80:20) scrap was traded at INR 29,000-29,500/t for spot deals involving immediate payment, while transactions on extended credit terms closed marginally higher at INR 29,500-30,000/t. The existing trade range of INR 29,000-30,000/t reflected the pricing premium attached to credit-based deals, emphasising the significant impact of liquidity conditions on transaction dynamics and deal closures.

Buyer-supplier sentiments

According to a mill representative quoted by BigMint, trade activity in the Chennai market has slowed notably over the past couple of weeks, with finished steel demand holding at moderate levels. In response to reduced transaction volumes, some mills initiated production cuts, currently operating at approximately 70-80% of their capacity. On the raw material front, sponge iron prices remained largely stable, though limited supplier participation was evident in the merchant market, with only a few actively offering material.

According to a scrap supplier, HMS (80:20) was traded between INR 29,000-30,000/t, with price realisations varying based on payment terms. Amid declining demand for both semi-finished and finished steel, mills faced pressure to reduce scrap procurement prices. Compounding the situation, some mills received shipments of imported scrap booked earlier, which contributed to increased inventory levels.

Regional comparison

In the Jalna market of western India, billet prices registered a minor correction of INR 100/t, closing at INR 39,300/t. Rebar prices, however, saw a modest uptick of INR 200/t to reach INR 43,200/t. Meanwhile, HMS (80:20) scrap prices held firm, assessed at INR 30,300/t. Market sentiment held firm, supported by moderate trade activity, while scrap inflows remained well-matched to mills’ production needs, with balanced supply at prevailing prices.

Outlook

Despite the prevailing market slowdown, scrap prices are likely to remain within a narrow range in the near term, with expected fluctuations limited to approximately INR +/- 500/t. Pricing will be primarily influenced by demand-side dynamics, stock levels at mills, and broader sentiment across the value chain.

Leave a Reply