- Buyers avoid large spot deals, amid steady port inventories

- Australian coking coal deal at $203/t CFR pulls up prices

This week, India’s coal market sentiments remained subdued as the ongoing monsoon rains have dampened demand from key sectors like cement and power. Buyers adopted a wait-and-watch approach, avoiding large spot purchases amid steady portside inventories and unpredictable import price trends. While some support came from mild global freight hikes and fresh Chinese demand for select grades, overall buying interest stayed limited. Market participants expect near-term trading to stay range-bound, with muted volumes and hesitant procurement likely until weather conditions improve and industrial activity picks up.

BigMint coking coal index rises on fresh Australian deal

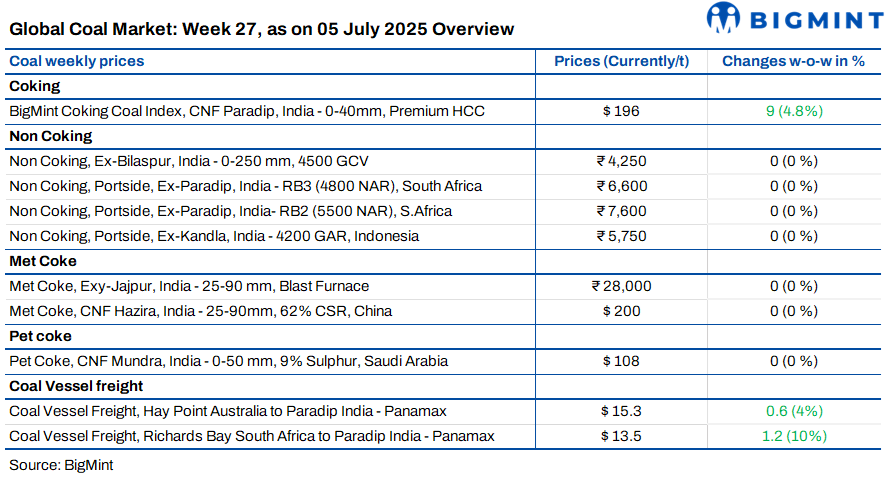

BigMint’s premium hard coking coal (PHCC) index climbed up by $9/t w-o-w to $196/t CNF Paradip on 4 July, supported by an end-August deal from Australia at around $203/t CFR for 40,000 t. The index, tracking price moves across origins, continued to gain after recent trade activity, reflecting firm market sentiment despite cautious outlook among some traders.

Domestic met coke prices steady as quotas boost sentiment

Metallurgical coke prices stayed firm this week, with BigMint’s 25-90 mm BF grade assessed at INR 28,000/t ex-Jajpur and INR 29,000/t exw Gandhidham. Market sentiment was cautiously positive as the government extended import quotas on LAM coke until December 2025, aiming to support local producers. Meanwhile, Australian PHCC prices edged up $9/t w-o-w to $183/t FOB, though Chinese coke prices held flat amid weak steel margins and limited plant utilisation.

Indonesian coal holds steady amid weak demand

Indonesian thermal coal prices stayed mostly flat at Indian ports, reflecting quiet buying interest. As per BigMint, 5000 GAR held steady at INR 7,400/t in Kandla and INR 7,300/t at Vizag; 4200 GAR was at INR 5,750/t and INR 5,650/t respectively, while 3400 GAR stayed at INR 4,300/t at Navlakhi. Power plants’ coal stocks slipped to 61.18 mnt but still remained at comfortable levels. Globally, 5800 GAR dipped to $71.43/t, while 4200 GAR edged up to $40.11/t amid uneven demand.

South African coal prices inch up; outlook steady

South African thermal coal prices at Indian ports moved up slightly this week. Exw-Gangavaram RB2 (5500 NAR) rose INR 50/t to INR 7,650/t, while RB3 (4800 NAR) touched INR 6,650/t. CNF offers stayed flat at $80-81/t for RB2 and $68-69/t for RB3, despite earlier index gains. Indian sponge iron prices saw mixed trends, dipping by INR 100-300/t in some regions while rising by INR 50-100/t in others. Port stocks stayed steady at around 15.86 mnt, keeping market sentiment cautious.

Domestic coal prices steady as demand stays muted

Domestic coal prices stayed flat this week, reflecting sluggish market sentiment. BigMint assessed 5000 GCV at INR 4,700/t and 4500 GCV at INR 4,250/t exw-Bilaspur, unchanged w-o-w. The market was notably quiet, with almost no fresh enquiries and scattered offers under selling pressure. SECL auctions saw limited buying interest, and only small volumes were booked.

Indian refineries revise pet coke offers for July

CPCL raised pet coke prices by INR 240/t m-o-m to INR 13,140/t for July. BPCL reduced Bina rail rates by INR 598/t to INR 13,522/t, while Kochi prices inched up by INR 228/t to INR 11,145/t. MRPL rolled over prices at INR 10,570/t (road) and INR 10,270/t (rake/barge). Nayara Energy increased pet coke offers by INR 260/t to INR 13,430/t, maintaining its premium in the market.

Pet coke import prices hold steady as monsoon slows demand

Imported pet coke offers in India stayed flat this week, with US-origin cargoes at $107-109/t CFR and Saudi-origin at $108-110/t CFR for both eastern and western ports. Market activity remained muted as the monsoon dampened infrastructure work, leading to lower cement production and softer pet coke demand. Traders expected subdued buying to continue in the coming weeks until construction picks up again.

Coal freights rise as monsoon, demand tighten supply

Coal freights to India increased this week as longer voyages, steady buying and monsoon-related delays supported rates. Panamax freights from Australia to Paradip rose by $0.6/t w-o-w to $15.3/t, while South Africa-to -Paradip jumped up by $1.2/t to $13.5/t. Indonesian freights inched up $0.3/t to $13.9/t. Higher bunker costs and seasonal stockpiling by Indian buyers also added to freight gains, despite largely steady portside coal inventories.

Leave a Reply