- Price drop expectations prompt need-based buying

- Sellers focus on clearing stocks before quarter-end

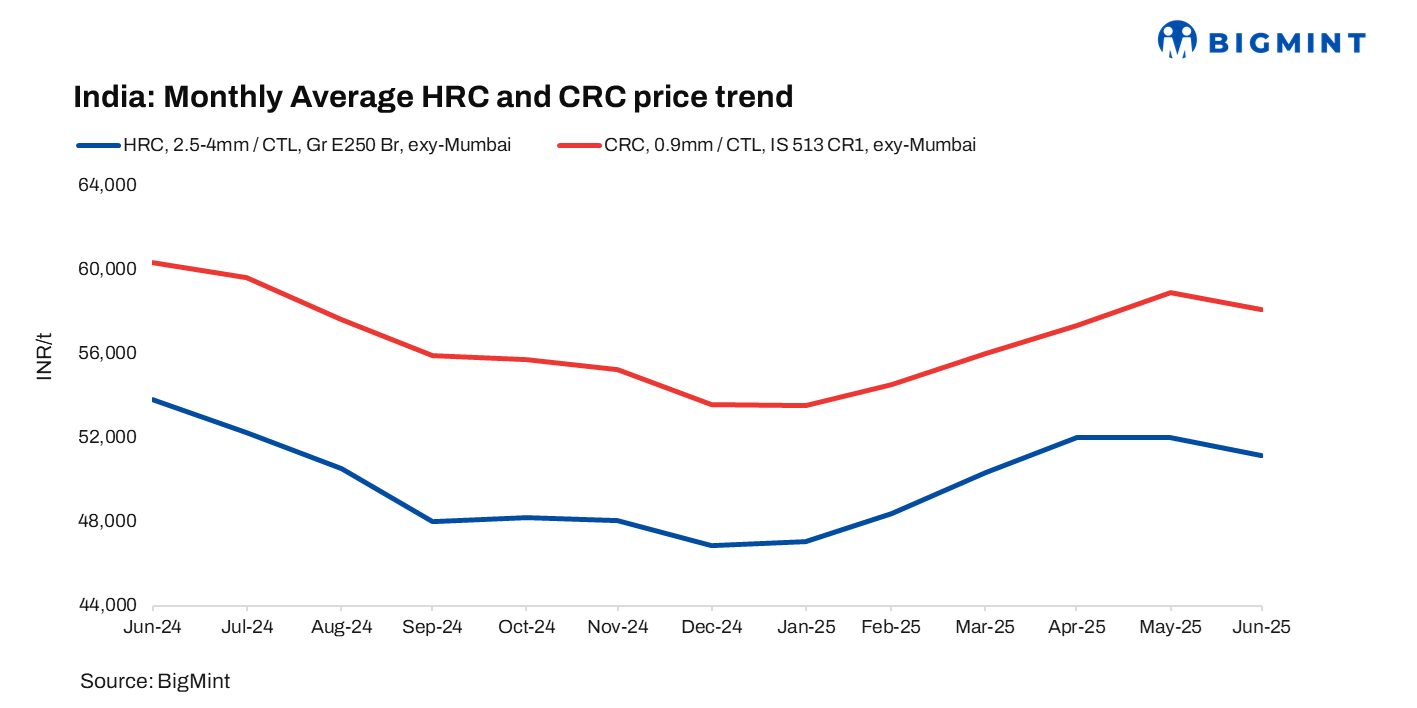

India’s monthly average trade-level hot-rolled coil (HRC, 2.5-8mm/CTL, IS2062, Gr- E250 Br.) prices declined by approximately INR 900/tonne (t) to INR 51,100/t in June 2025 from the previous month’s INR 52,000/t exy-Mumbai. Simultaneously, cold-rolled coils (CRCs, 0.9mm/CTL, IS513, Gr-O) dropped INR 800/t m-o-m to INR 58,100/t in June, compared to the preceding month’s INR 58,900/t exy-Mumbai, excluding GST at 18%.

Market updates

Mills roll over list prices for Jun’25 sales: Indian steelmakers kept HRC and CRC list prices unchanged for June 2025 sales.

Leading producers priced HRCs at INR 52,150-54,000/t ($608-630/t) and CRCs at INR 57,650-60,750/t ($672-708/t) ex-Mumbai. New entrants offered HRCs slightly lower at INR 51,900-52,000/t ($605-608/t).

Muted demand, monsoon disruptions weigh on market sentiment: Domestic demand remained need-based, and price resistance persisted. Buyers negotiated down prices amid expectations of further corrections. Additionally, end-users delayed purchases, expecting price tags to decline, while sellers sought to clear inventories ahead of the quarter-end to improve liquidity. However, distributors could not cut prices beyond a certain degree, given that trade prices were already much below mills’ list rates and no price support had been announced by mills.

Additionally, inventories in major markets were above average, except in certain pockets, where supply was constrained. The early onset of the monsoon slowed down construction activity as well as the transportation of materials.

High-frequency indicators such as GST collections, which grew just 6.2% y-o-y in June – the slowest first-quarter expansion in over four years – along with muted UPI transactions and sluggish diesel demand, pointed to weak consumer sentiment. Passenger vehicle sales fell 6% to 320,000 units, and the commercial vehicle segment also remained under pressure, with Tata Motors’ offtake down 9% and Ashok Leyland slipping 1%.

Imports remain low: India’s bulk imports of HRCs touched 294,879 t as of 27 June, based on vessel line-up data from BigMint. This indicates that volumes may remain low compared to the over 400,000 t seen in December 2024-January 2025. However, there may be a slight uptick m-o-m. Around 159,825 t of cargo are expected in July.

Export market remains lacklustre: India’s HRC export offers to the EU fell by $26/t m-o-m to $565/t FOB in June.

Over the last month, European HRC prices remained under pressure amid weak domestic demand, high inventories, and subdued market sentiment. Seasonal holidays and the summer slowdown further weighed on trading activity. Despite price cuts, buyers remained cautious, expecting further corrections due to sluggish consumption from key sectors such as automotive and construction. At the same time, Indian mills focused more on the domestic market, supported by stronger price realisations, resulting in limited export offers to Europe.

Weekly assessment update

BigMint’s benchmark evaluation (bi-weekly) for HRCs remained range-bound w-o-w at INR 50,800/t ($664/t) exy-Mumbai as of 1 July 2025. In the same period, CRC prices decreased by INR 600/t w-o-w to INR 57,300/t ($755/t) exy-Mumbai. These prices exclude GST at 18% and are for cut-to-length (CTL) form.

Outlook

Trade-level prices of HRCs and CRCs are expected to stay under pressure in the near term, following June’s m-o-m decline of INR 900/t and INR 800/t, respectively. Weak demand, high inventories, and monsoon-related disruptions are likely to weigh on sentiment. With trade prices below mill list rates and limited export support, further softening may be possible. Additionally, mills are expected to reduce their list prices.

Leave a Reply