- Rainy season weighs on construction sector sentiment

- HKC certification gap limits bidding access for Chattogram yards

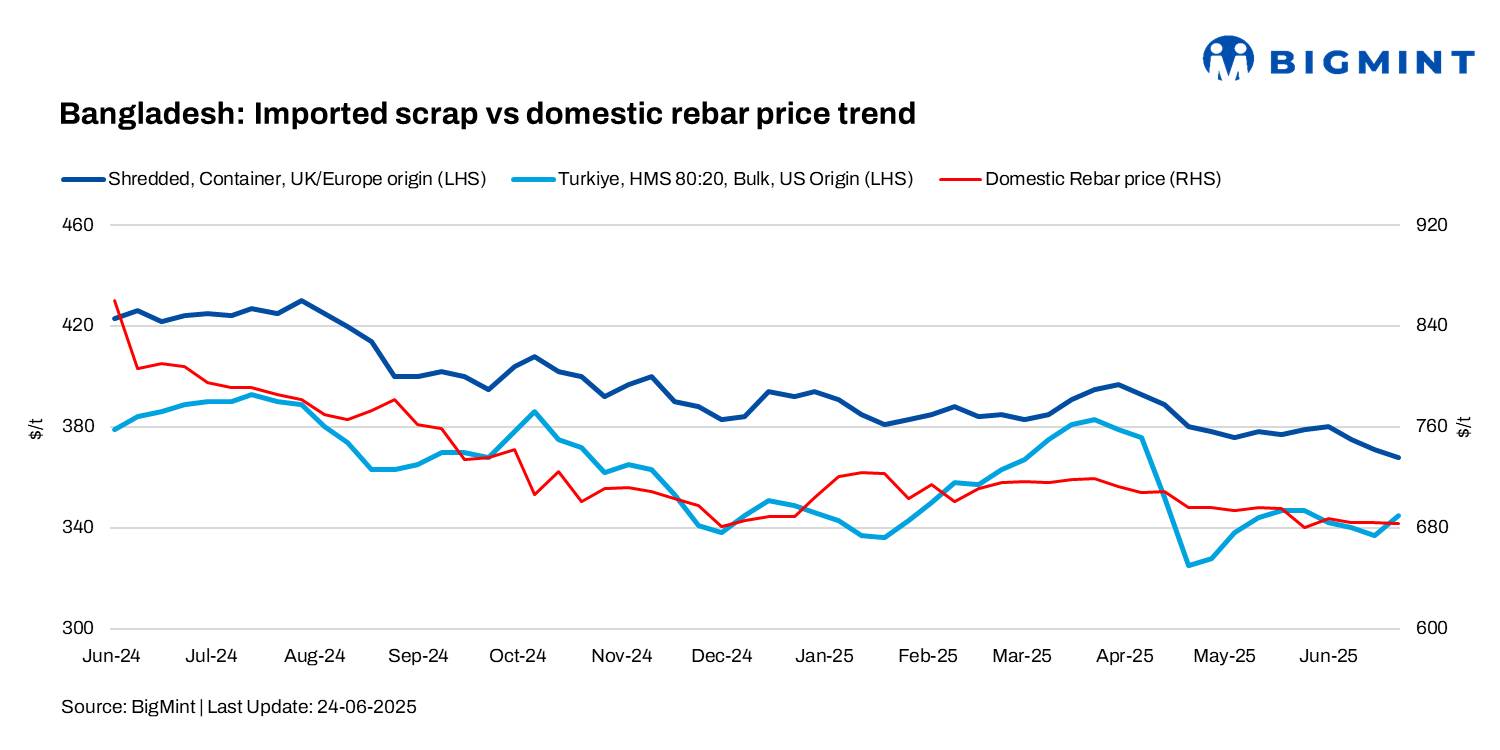

Bangladesh’s imported ferrous scrap market saw prices fall by up to $12/t this week as monsoon rains and weak steel demand dampened buying interest.

Most buyers were targeting shipments for late August or early September 2025 and were seen holding off purchases for the present.

Containerised offers stand at $355/t for HMS (80:20), $370-375/t for shredded, and over $380/t for Malaysian busheling, while buyer bids remain lower at around $345/t CFR Chattogram.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched down by $3/t to $356/t.

- European-origin containerised shredded was down $3/t w-o-w to $368/t.

- Japanese-origin H2 bulk prices stood at $348/t CFR Chattogram, down by $9/t w-o-w.

- US-sourced HMS (80:20) bulk prices stood at $357/t, down by $12/t w-o-w.

Market updates

Containerised HMS (80:20) is being offered at around $355/t CFR from Australia, while shredded scrap prices are quoted at $370-375/t. Malaysian-origin busheling is being offered even higher at $380-385/t CFR. However, market activity remains subdued, as buyers are resisting current levels — bids for 80:20 and shredded scrap are not exceeding $345/t CFR Chattogram, according to market sources.

As per a Chattogram-based trader, USA West Coast bulk offers are at $350/t for HMS, $355/t for shredded, and $360/t for bonus grade. A US-based yard source confirmed two recent bulk deals priced at $346/t and $350/t CFR Chattogram for HMS basis only. Both cargoes–40,000 t and 32,000 t, respectively–also included shredded and bonus scrap, though their individual prices were not disclosed.

As per a Japanese scrap supplier, “From Japan, H2 offers are heard at $340-345/t, HS at $370/t, and Shindachi at $370-375/t. Buyers, however, are bidding lower– $335-340/t for H2, $360/t for HS, and $365/t for Shindachi.”

A trader based in the Far East informed that Singapore-origin HMS 70:30 offers were at $345/t and HMS 80:20 at $350-355/t, though $350/t is seen as market-aligned. One Singapore-origin cargo was recently sold at $349/t for HMS 80:20 and $362/t for PNS (15,000-18,000 t).

Domestic market update

According to market participants, buying appetite remains weak as only a few mills are operating, with limited support from government projects. Rebar prices continue to decline — currently at BDT 80,500-81,000/t exw Dhaka ($658-662/t) and BDT 83,500-84,000/t exw Chattogram (equivalent to $683-687/t).

Chattogram ship recycling market

With the Hong Kong Convention taking effect on 26 June, only 10 Chattogram yards have secured certification, while 25 are still undergoing upgrades. Without HKC approval, uncertified yards are unable to obtain NOCs or participate in fresh bids, prompting large vessels to divert to Indian yards.

Market sentiment remains weak amid stagnant steel plate prices at $551/t, monsoon-related disruptions, and muted construction and manufacturing activity. Despite a slight recovery in the Bangladeshi Taka, downstream steel demand remains sluggish. A recent $5/t drop due to budgetary tax revisions adds further pressure, although Bangladesh still offers the highest global scrap prices.

Chattogram Port received 2,985 LDT this week, steady w-o-w.

Outlook

Bangladesh’s imported scrap market is likely to remain under pressure in the near term as monsoon disruptions persist and finished steel demand stays weak. Mills are expected to remain cautious with limited booking activity. Unless there is a recovery in domestic construction or government project spending, scrap prices may face further downside or remain range-bound, especially with buyers resisting current offer levels.

Leave a Reply