- LME nickel prices largely stable w-o-w

- Demand remains weak amid monsoon slowdown

India’s stainless steel (SS) finished flats and longs prices remained stable w-o-w amid moderate demand.

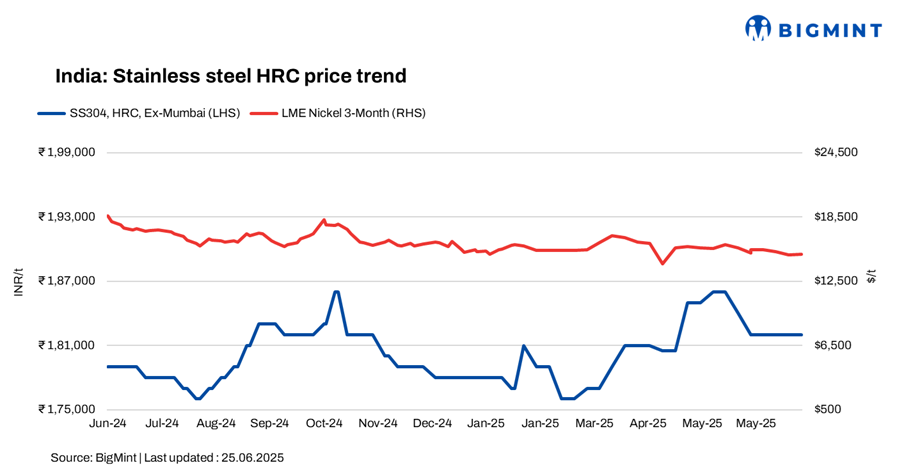

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) hovered at 182,000/tonne (t), while 304L (25-100 mm) black round bars stood at INR 157,000/t, both ex-Mumbai.

LME nickel, Asian NPI remain steady w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,000/t, remaining largely stable against last week’s $14,975/t. Nickel stocks in LME-registered warehouses stood at 204,120 t, rangebound compared to 204,936 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 930/t ($129/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $112/t.

Market insights

The stainless steel finished market continues to face headwinds due to persistently weak demand across India. A lack of new infrastructure projects and limited government initiatives have contributed to the subdued market sentiment.

Additionally, the onset of the monsoon season has further slowed construction activity and downstream consumption, putting additional pressure on mills and distributors.

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 325,000/t and 316 cold-rolled coils (CRCs) at INR 333,000/t ex-Mumbai, both stable w-o-w.

Demand for finished SS longs remains very weak in the domestic market, As per market participants, “Major mills are currently operating at 60-70% of their capacity. If this sluggish trend continues, production levels may be reduced even further.”

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,450/t ($1,874/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices stayed stable as compared to the previous assessment on 18 June. Steady dynamics in the market along with stable LME futures largely kept prices unchanged.

As per BigMint’s assessment on 25 June, ferro molybdenum prices were at INR 2,674,000/t ($31,125/t) exw-India. Approximately 10 t of deals were concluded last week within the price range INR 2,660,000-2,730,000/t ($30,962-31,777/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,100/t ($1,162/t) exw-Jajpur, remaining rangebound w-o-w.

Ferro silicon: Indian ferro silicon (70%) prices kept trending lower over last week, sliding by INR 600/t ($7/t) w-o-w. Prices fell as inquiries remained limited prompting sellers to lower their offers.

As per BigMint’s assessment on 23 June, ferro silicon prices were INR 88,600/t ($1,029/t) exw-Guwahati. In Bhutan, prices fell by INR 2,200/t ($26/t) w-o-w to INR 88,200/t ($1,025/t) exw. No deal was concluded last week as the majority of sellers were either sold out or were catering to previously booked orders.

Ferrous scrap: India’s imported scrap market remained subdued amid weak finished steel demand, monsoon disruptions, and high inventories, keeping buyers largely inactive.

Containerised shredded scrap offers held steady at $360-362/t CFR Nhava Sheva, but tradable levels were lower, mostly around $350-355/t, with occasional deals closer to $358-360/t.

Cheaper domestic alternatives like sponge iron and scrap further discouraged import bookings. Sellers adopted a cautious approach, withholding offers as mills stayed on the sidelines amid sluggish steel demand.

Outlook

In the near term, stainless steel prices are expected to stay stable within a narrow range, with market activity likely to remain moderate.

Leave a Reply