- CRC prices fall by INR 300/t w-o-w

- Market waits for price support from mills

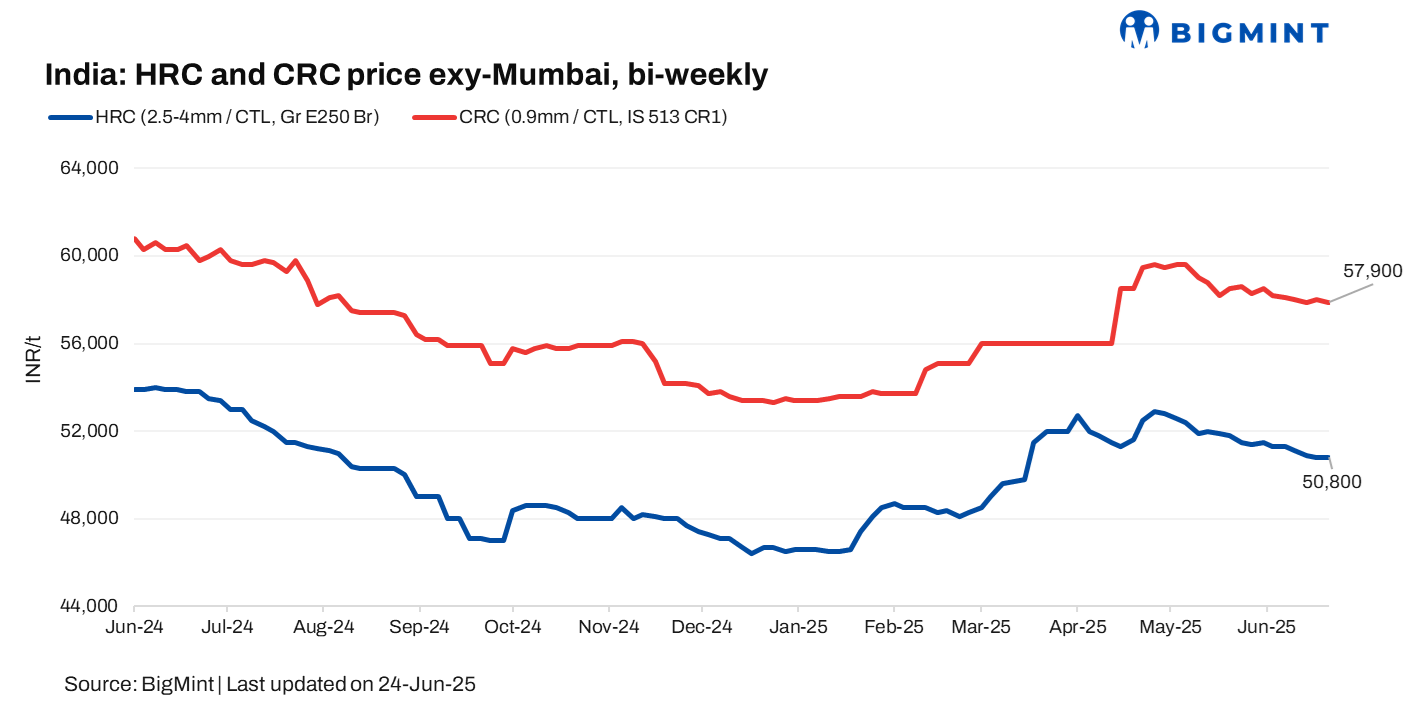

Trade-level prices of hot-rolled coils (HRCs) in India declined by up to INR 400/tonne (t) ($5/t) w-o-w to INR 50,600-52,500/t ($588-610/t) across markets. Meanwhile, cold-rolled coil (CRC) prices declined by up to INR 300/t ($3/t) w-o-w at INR 56,200-60,700/t ($653-705/t).

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) remained stable w-o-w at INR 50,800/t ($590/t) on 24 June 2025. CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 100/t ($1/t) w-o-w to INR 57,900/t ($673t). Prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

Market awaits mills’ support: The market is waiting for clarity on whether mills will provide price support, as trade-level prices have dropped below mill prices and have remained lower for a while. Meanwhile, demand continues to be weak, with few enquiries and an even slower rate of converting inquiries into actual sales, sources reported.

“The market expects mills to announce price support soon. As a result, many buyers are holding off on restocking, hoping for better prices as the quarter-end approaches. Distributors, on the other hand, are under pressure to meet their MoU commitments, which is forcing them to sell at lower prices to clear old inventory,” a market participant noted.

Import volumes: India’s bulk imports of HRCs touched 214,961 t as of 23 June, based on vessel line-up data from BigMint. Around 48,946 t of additional cargo are expected by end-June and another 69,748 t in July.

Export trends: BigMint’s India HRC (S275) export index fell by $5/t w-o-w to $550/t FOB main port, following a 5,000 t deal to the EU. Buyers remain cautious amid expectations of a summer slowdown, keeping pressure on prices.

In the Middle East, weak sentiment due to geopolitical tensions continue to impact demand. Indian mills are holding back HRC offers to the region amid strong competition from other suppliers.

Outlook

Prices of HRC and CRC are expected to stay under pressure in the near term due to weak demand. Distributors are selling at lower prices to meet quarterly commitments, while buyers are delaying purchases in anticipation of mill price support. Limited export demand may prevent any significant price recovery.

Also, as per recent Joint Plant Committee (JPC) data, inventory levels for HR coils/strips & equivalent at mills stood at 562,000 t in March 2025, rose to 597,000 t in April, and marginally eased to 572,000 in May signaling a build-up followed by limited liquidation amid sluggish offtake.

Leave a Reply