- Semi-finished prices remain stable w-o-w

- Finish steel sees average trading activity

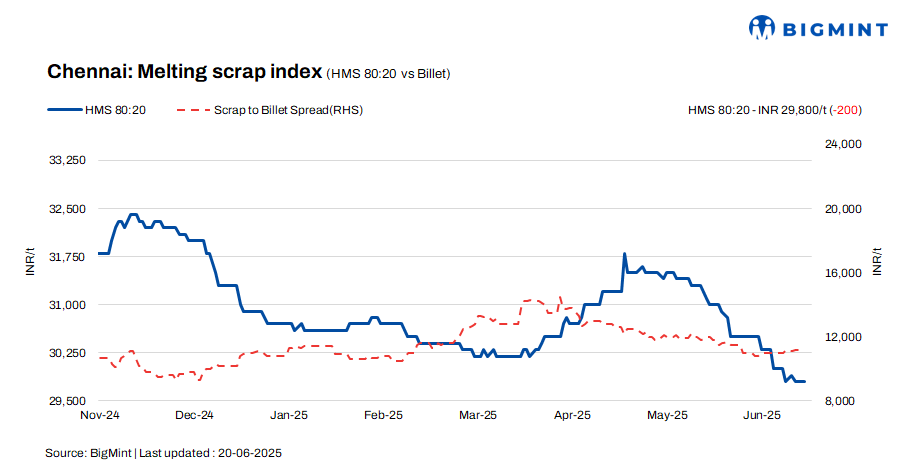

HMS (80:20) prices in Chennai slipped by INR 200/t w-o-w, settling at INR 29,800/t, though daily prices remained flat, as per BigMint’s latest report. Billet prices remained stable at INR 41,000/t across both daily and weekly assessments. Conversely, rebar prices registered a decline of INR 200/t to INR 46,300/t, reflecting uniform downward movement on both daily and weekly terms.

Imported, domestic price trends

A scrap trader informed that shredded scrap offers from Australia were quoted at $360–365/t CFR Chennai, while buyers remained cautious, targeting purchases at $355–360/t. In comparison, HMS 80:20 offers stood slightly lower at $340–345/t. Weakened finished steel demand continues to weigh on market sentiment, prompting buyers to reduce bids by $5–10/t below quoted levels.

In the Chennai market, domestic HMS (80:20) scrap is transacting at INR 29,500–30,000/t for immediate payment spot deals, while trades on extended credit terms are priced slightly higher at INR 30,000–30,500/t. The prevailing trade range of INR 29,500–30,500/t underscores the impact of payment terms on pricing, with liquidity preferences playing a key role in deal finalisations.

Buyer-supplier sentiments

A mill representative informed BigMint that finished steel demand has remained weak over the past couple of months, resulting in a build-up of 15–20 days’ worth of rebar inventory at the mill level. This surplus stock is creating downward pressure on prices, contributing to a drop of approximately INR 1,500/t in billets and INR 1,200/t in rebar over the last month.

According to a scrap supplier, HMS 80:20 is currently trading at INR 29,500–30,500/t, with pricing influenced by payment terms. Amid subdued demand for both semi-finished and finished steel, mills are facing pressure to lower scrap procurement rates. A notable shift in payment behaviour is emerging, with mills extending payment cycles from the usual 5–7 days to 10–15 days, indicating tighter liquidity. With continued weakness in finished steel demand, a further reduction in scrap buying rates appears likely in the near term.

Regional comparison

In the Jalna market of western India, billet and scrap prices declined by INR 100/t each, settling at INR 39,500/t and INR 30,600/t, respectively. Rebar saw a steeper correction, dropping by INR 300/t to INR 43,500/t. Ongoing rainfall in the region has disrupted trade activities in finished steel. To optimise production costs, most mills are currently operating with a 50:50 ratio of scrap and sponge iron in their charge mix.

Outlook

According to market sources, scrap prices are projected to remain range-bound in the near term, with potential fluctuations capped at INR +/- 500/t. This anticipated stability stems from persistent uncertainty in the finished steel trade, where cautious buyer and seller sentiment continues to limit transactional activity. As a result, the prevailing market mood is expected to constrain price volatility and sustain a narrow trading band.

Leave a Reply