- Crude steel output, consumption fall by 6-9% m-o-m

- Coal production plunges to 7-month low amid supply glut

- Auto output, sales fall; inventories at INR 51,000-52,000 cr

Morning Brief: India’s macroeconomic indicators showed diverging trends in April 2025. While the manufacturing purchasing managers’ index (PMI) crawled up to a 10-month high of 58.2 points, both core sector growth and the Index of Industrial Production (IIP) fell to eight-month lows.

Notably, the contrasting movements may be warning signs of a further macroeconomic slowdown in May.

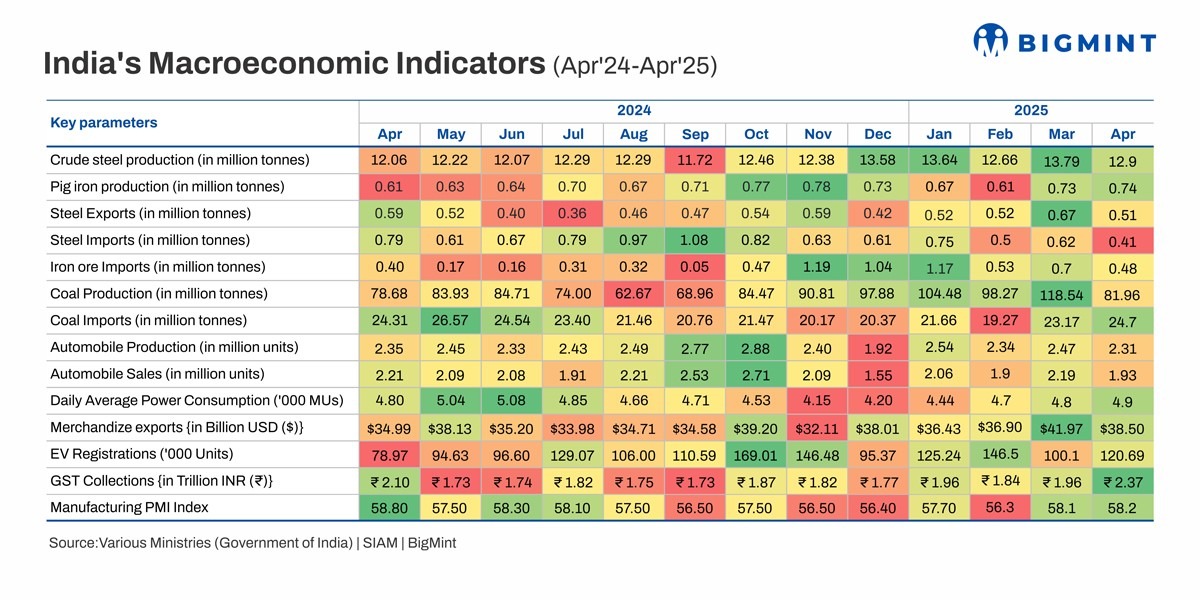

Factors influencing Indian economy in Apr’25

Crude steel production, consumption fall m-o-m

Crude steel output declined by 6.5% m-o-m to 12.9 million tonnes (mnt), as production schedules were impacted by maintenance downtimes. Steel consumption, too, was subdued, falling by 9% to around 13 mnt from 14 mnt in March, amid slowing demand and buyer resistance to price hikes.

In contrast, pig iron production was largely stable m-o-m, recording a minor uptick of 1.4% m-o-m to 0.74 mnt.

India emerges as net steel exporter

India was a net steel exporter in April, with exports exceeding imports by 0.1 mnt. Both exports and imports fell m-o-m, by 24% to 0.51 mnt and 34% to 0.41 mnt, respectively.

The drop in exports could be attributed to sluggish demand globally, growing trade protectionism, and elevated global exports from China (over 10 mnt), aided by its predatory pricing. The US reciprocal tariff policy also led to uncertainty in markets worldwide.

Meanwhile, imports were stifled by the 12% safeguard duty, which was finally imposed on 21 April. Stricter Bureau of Indian Standards (BIS) norms also helped pare down volumes.

Iron ore exports, imports decline

India’s iron ore and pellet exports fell by 46% m-o-m in April to 1.68 mnt, a four-month low. For reference, March registered 3.13 mnt, a nine-month high.

The key factor contributing to the drop was lower demand from China amid heightening tensions with the US, which led to cautious sentiment among mills.

Meanwhile, imports fell by 31.4% m-o-m to 0.48 mnt but were 20% higher y-o-y due to the requirement of specific grades and high logistics costs in India.

Additionally, iron ore production edged down by 1.2% m-o-m to 33.79 mnt.

Coal production drops, imports rise

Coal output fell a steep 31% m-o-m to a seven month-low of 81.96 mnt, with Coal India (CIL) producing 62.06 mnt, down 27.7%. Volumes were pressured by persistent weak demand due to a supply glut in the domestic market.

High inventory levels at CIL, ranging at around 112 mt compared to the FY’20-25 average of 83 mnt, likely also contributed to the steep drop in its output.

However, it should also be noted that March’s 119 mnt, a one-year high, was due to domestic miners ramping up production to meet annual targets before the FY-end.

April’s coal imports of 24.7 mnt also represented a 6.6% m-o-m growth, with arrivals of both coking and thermal coal climbing up. Imports rose because some companies have overseas sourcing patterns, and some plants run only on imported coal.

Y-o-y, imports were up by 1.6%, with the surge in domestic production capping greater spikes.

Industrial activity slows to 8-month low

Key macroeconomic indicators, such as core sector output growth and the IIP, indicated a noticeable deceleration in industrial activity. Both plummeted to eight-month lows of 0.5% and 2.7% in April. In March, the two were at 4.6% and 3.9%, respectively.

Notably, core sector data shows that while cement production, a key gauge of construction activity in the country, advanced the highest in April – at 6.7% – it was much lower than March’s 12.2%.

According to IIP data, the mining and quarrying segment contracted by 0.2%, electricity generation moderated to 1.1%, and the primary goods category declined to 0.4%. All three recorded their worst performance since August 2024.

Daily average power consumption increased to 4,900 million units compared to 4,800 million units in the previous month.

On the positive side, the manufacturing segment expanded by 3.4%, while consumer durables saw a 6.4% rise, both quickening at the fastest pace in three months. However, the capital goods sector stole the show, with a sharp rise of 20.3%, although this was partly due to a low base effect.

Manufacturing PMI hits 10-month high

The manufacturing PMI was at a 10-month high in April, although it increased by just a fraction 0.2% m-o-m.

This growth, which indicates the fastest pace of expansion since June 2024, stemmed from a robust increase in order books, especially for exports. Again, firms recorded healthy margins due to strong pricing power and a rise in output prices, which outstripped the modest climb in input costs. Additionally, optimism reined regarding FY’26 demand strength.

Auto sector posts muted performance

Automobile production dropped 6.5% m-o-m to 2.31 mnt, as manufacturers recalibrated volumes amid subdued business confidence. Parallelly, sales were down by 12% at 1.93 mnt, indicating lack of end-user interest.

According to the Federation of Automobile Dealers Associations (FADA), passenger vehicle (PV) inventory stood at 52-53 days, more than double the recommended 21 days. Car dealerships had unsold inventory worth INR 51,000-52,000 crore, a record peak in value terms.

Supportive factors included the summer harvest festival period, resumption of the wedding season, and new model introductions. However, in the PV segment, consumer sentiment was cautious, which hindered inquiry-to-sales conversions.

Furthermore, commercial vehicle (CV) sales contracted by 4.4% m-o-m due to price hikes, stagnant fleet utilisation, and a slew of holidays in April.

In contrast, electric vehicle (EV) registrations increased 20.6% m-o-m amid favourable market sentiment.

Merchandise exports drop 8% m-o-m

India’s merchandise exports declined by 8.3% m-o-m to $38.5 billion, possibly pressured by market uncertainty regarding the tariff-related tug-of-war and other trade tensions.

GST collections surge over 20% m-o-m

GST collections shot up by 21% m-o-m to INR 2.37 trillion, reflecting the impact of a boost in economic activity due to the fiscal-end.

Outlook

As per early estimates, manufacturing momentum softened in May. The manufacturing PMI fell to a three-month low of 57.6 points, against preliminary projections of a slight growth to 58.3 points.

In May, steel demand was also lacklustre, and prices witnessed a steady downtrend throughout the month, with BigMint’s India Steel Composite Index losing almost 2.5%. Weak demand, tight liquidity, and a monsoon-led slowdown in construction activity suppressed trade activity.

This depression in prices has continued into June, and there are no signs of abatement yet.

However, hope remains. The RBI’s 50 basis point cut to the repo rate in early June is expected to address the liquidity woes of market participants and help lift business growth and consumer purchasing power.

Although it is uncertain by when the market will be able to see a noticeable uptick in demand and whether the positive impact will be sustained, for now, the manufacturing and real estate segments are cheering. The steel industry can also expect some relief from its current despondency.

Leave a Reply