- Govt’s policy impact may be seen over 2026-28

- Real estate inventory destocking on the cards

- Rebar prices likely to bottom out in 2nd half of year

By Madhumita Mookerji

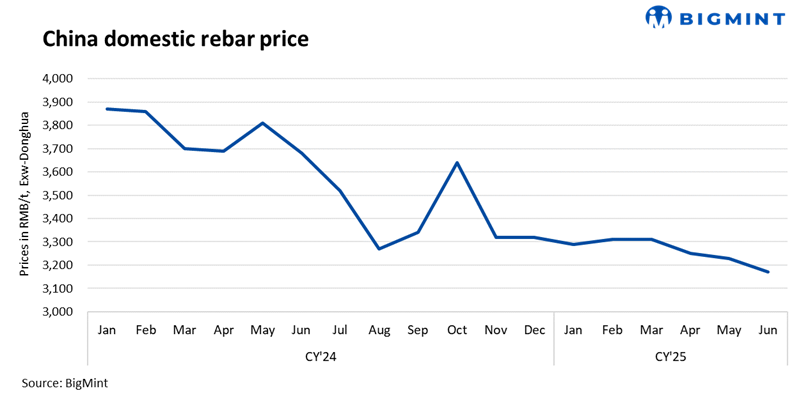

Recently, China’s rebar prices fell to their eight-year lows amid an inventory glut. While some indexed prices were hovering at RMB 3,236/tonne ($451/t), Tangshan tags fell even lower to RMB 3,180/t ($443/t) on 12 June, 2025. June’s prices are averaging RMB 3,180/t while May’s were at RMB 3,207/t ($447/t).

So, what does it indicate about China’s downstream demand? BigMint deep dives.

A source from China informed BigMint, if rebar, a benchmark product used in building construction and which acts as a barometer for China’s traditional steel demand, has plunged to an eight year low, “We cannot deny it is caused by structural changes in downstream demand.”

The source further observed that China’s entire real estate industry may have entered a period of deep trough. It may be mentioned that demand for rebar comes from two segments within construction – domestic infrastructure, and real estate.

Overall, construction steel demand has fallen to -1% in 2025 against a 7% growth in 2020, as per Horizon Insights data. Within this corpus, the demand drop from the real estate sector has deepened from -0.2% in 2020 to -15% in 2025, after recouping from a sharper -24% in 2023 and -31% in 2024. Infrastructure demand has slowed from a growth of 18% in 2020 to a mere 4% in 2025.

Why is rebar faring poorly?

Changing demographic patterns: The Chinese real estate market has been growing rapidly for the last 30 years. But, this itself has led to larger problem where the demographic support to the housing sector has weakened leading to its slow collapse, and whose immediate impact emerged in the implosion of real estate giants like Evergrande and others a few years back. “When our population cannot support the huge real estate volume, we will have this structural adjustment of real estate,” reasoned the Chinese source.

Shifting demand patterns: Demand from construction may be the largest but manufacturing has played catch-up. In 2010, demand was driven by construction with an estimated 42% share. Machinery (20%) and infrastructure (13%) recorded the second- and third-highest demand, respectively.

However, over the past 13 years, demand has shifted towards machinery and infrastructure with that from construction estimated to have almost halved to 24%, as firms purchased 37 million tonnes less steel in 2023 compared to 2010. This slump can, in part, be attributed to the Chinese real estate crisis and developers’ bankruptcies, triggered by the demographic shift.

The machinery sector, on the other hand, witnessed incredible growth spurting from an estimated 20% share in overall steel demand in 2010 to 30% by 2023, boosted by an influx of equipment order renewals. Infrastructure demand growth rose from around 13% to 17% over this timeframe.

Factors that will impact rebar performance in medium term

Pinning hopes on urban renewal: Looking at the medium term, the Chinese real estate and infra segments are pinning hopes on the government’s urban renewal programme, including urban village renovation that encompasses focus on improving infrastructure. This involves setting up fresh infrastructure as well as renovating existing ones.

Plan to destock realty inventories: Secondly, with an eye on the medium term, the authorities, saddled with high inventory in the entire real estate sector, are planning to speed up the destocking process through incentives. “In the medium to long term, we may have two changes in the structure of the entire housing segment. The first is that our entire affordable housing sector may grow. As for commercial housing, it may be in a state of destocking to a reasonable level before we can have new development,” a Chinese source informed.

But it is obvious that demand for construction materials will show a downtrend despite the fact that housing has performed slightly better than last calendar. Special steels in construction, rather than ordinary grades of rebars and wire rods, will drive demand.

Policy impact to take time: Several measures were implemented in the recent past. These included: 1) reduction in commercial loan interest rates to boost housing sales; 2) reduction in the down-payment portion, to promote new and second-hand houses; 3) permission to local authorities to issue special-purpose bonds to acquire commercial properties for affordable housing and idle land from developers.

Although these measures have not borne immediate fruit, many feel a turnaround in the realty space can happen within 2026-28.

Outlook on rebar prices for this year

Rebar, at current levels, is seeing a y-o-y decline of around 8%. “So, rebar completed the decline of the entire last year in half a year in 2025,” a China-based source said.

So, how will rebar behave in H2CY’25? The downward pressure may continue. Improvement in real estate, sustained investment in infrastructure, and addition of new infrastructure projects, may support prices. However, at a realistic level, there is lack of optimism over improvement in real estate unless there is continued policy support.

“Under the current policy implementation momentum, we may see a gradual or slow improvement in the real estate market. Can real estate investment turn positive by end-year? We can’t be too pessimistic, but we can’t be too optimistic either. Under these circumstances, rebar prices will likely bottom out in second half of the year,” the source said.

Another source feels, the falling momentum may vary depending on factors like global uncertainties and Sino-US relations. “Thus, the fall in rebar prices may be softer compared to flats, because, the latter will be impacted by exports demand, and anti-dumping moves.”

Leave a Reply