- Amid subdued buying, mills forced to keep prices stable

- India’s manufacturing PMI drops to 57.2 in May

Two major domestic coated flat steel producers have rolled over their list prices for June 2025 dispatches, effective 1 June. End-industrial buyers in the traders’ market continued to procure according to their requirements, avoiding any build-up of inventories. Furthermore, the early arrival of monsoons also added to the woes of distributors in the second fortnight of May.

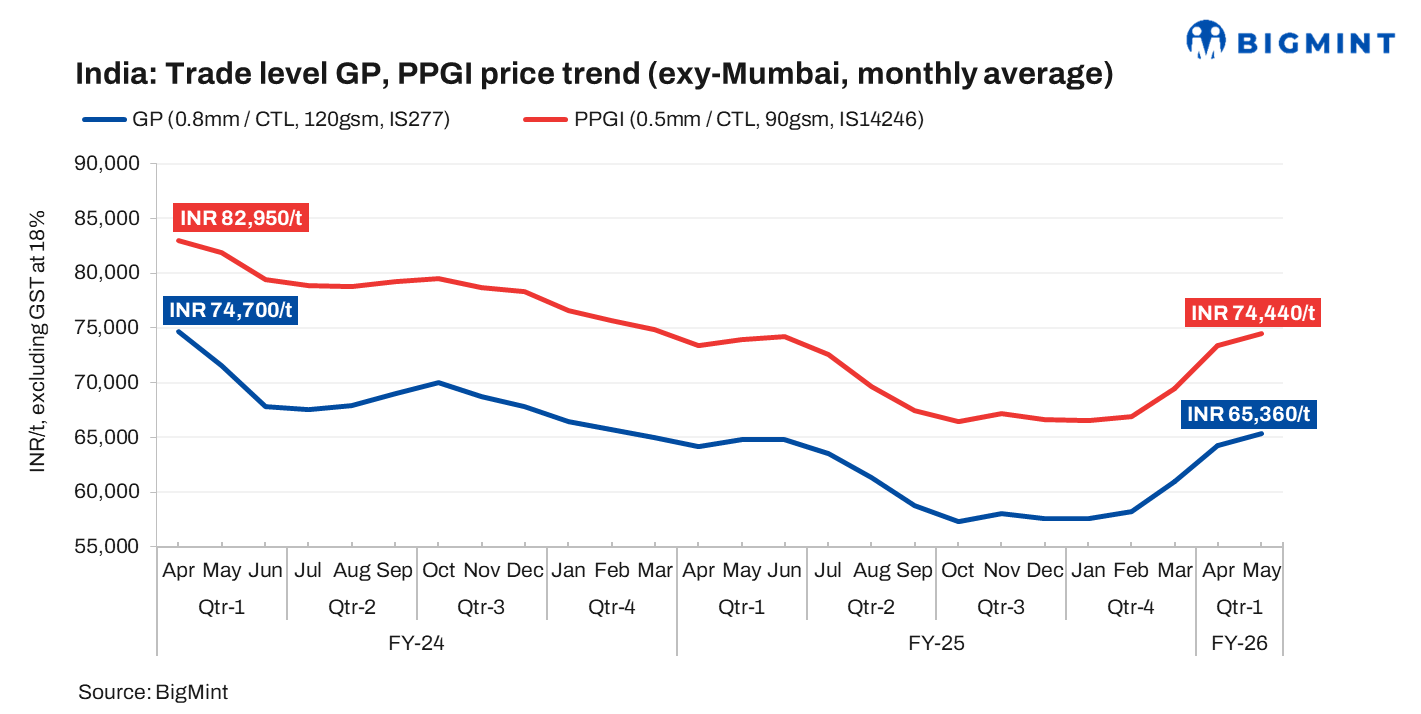

The effective list prices of GP (0.8mm, 80gsm, IS277) stand unchanged at INR 65,000-65,600/t ($757-764/t) ex-Mumbai, while those for PPGI (0.5mm, 90gsm, IS14246) are at INR 74,500-75,500/t ($868-879/t) ex-Mumbai for early June dispatches. Prices mentioned are for coil forms, excluding GST at 18%. (USD 1 = INR 85.8542; INR 1 = USD 0.0116477)

The monthly average trade level prices have shown a continual increase over the last five months (January-May). The price levels in May for 0.8 mm/CTL, 120 gsm, IS277 GP stood at INR 65,400/t ($768/t) exy-Mumbai, up INR 1,100/t ($13/t), m-o-m, while those for PPGI (0.5 mm/CTL, 90 gsm, IS14246) were assessed at INR 74,400/t ($873/t) exy-Mumbai, up INR 1,000/t ($12/t), m-o-m. This price ascent in May was shallow compared to what was seen in April, when GP had increased by INR 3,300/t and PPGI by INR 4,000/t. The figures are rounded off to the nearest 100 and exclude GST at 18%. (USD 1 = INR 85.1975; INR 1 = USD 0.011737)

Safeguard duty: The Directorate General of Trade Remedies (DGTR) had sent an intimation about the oral hearing to be scheduled on 5 June vide the letter dated 27 May. Meanwhile, the market went abuzz with the news that industry participants might request DGTR to increase the safeguard duty from 12% to 24%.

It may be recalled that on 19 April the DGTR levied the 12% safeguard duty on steel imports on a provisional basis for 200 days. The threshold price for zinc-coated flat products has been set at $861/t CIF (cost, insurance and freight) India, whereas the threshold price for colour-coated or pre-painted was at $964/t CIF India, as per the gazette. However, this also could not be much of a support and the prices dropped in the same week after remaining rangebound for the preceding three weeks.

Market updates

Trade prices rise halts towards end-May: Trade-level prices of coated flat products had shown an ascent in the first week of May with mills raising their list prices amid expectations of improvement in demand ahead of monsoons. However, prices lost sheen and declined in the fourth week of the month.

The latest weekly assessment, on 5 June, showed GP (0.8 mm/CTL, 120 gsm, IS277) coil prices at INR 65,000/t ($757/t) exy-Mumbai, down INR 200/t ($2/t) w-o-w, with offers varying in the range of INR 64,500-65,500/t ($751-763/t).

On the other hand, PPGI (0.5 mm/CTL, 90 gsm, IS14246) stood unchanged at INR 74,000/t ($862/t) exy-Mumbai, with offers at INR 73,500-74,500/t ($856-868/t). These prices exclude GST at 18% (USD 1 = INR 85.8542; INR 1 = USD 0.0116477).

“The weakening of demand and end-buyers’ resistance to maintaining inventories have dented activity levels in the traders’ market. Around 10-12 days of activity was cut short because of the early arrival of monsoons in India,” said a major distributor based in western India.

Demand-supply dynamics: Supply constraints that had propelled mills to raise their list prices amid production-related hassles in May continued to provide support in turn leading to a rollover in June 2025. Mills continued to focus on the business-to-customer (B2C) segment mostly towards the infrastructure, construction and manufacturing segments in May 2025.

The market indices, however, nudged down in May, hinting towards a decline in consumption levels. The manufacturing purchasing managers’ index (PMI) dropped by 1 point m-o-m to 57.2 in May as against the previous month.

Production and consumption volumes: The production of coated flat products declined by 5% m-o-m to 0.897 mnt in April compared to 0.947 mnt in March, as per recent data released by the Ministry of Steel. The average daily production was computed at around 29,900 t per day (tpd) in April compared to 30,548 tpd in March. Production volumes of Tata Steel were steeply lower compared to the previous month while there was a shallow drop witnessed in those of AM/NS and JSW in April.

Meanwhile, consumption also dropped by around 10% m-o-m in March to 0.880 mnt as compared to February’s 0.976 mnt. Out of these volumes, PPGI or the colour-coated coils aggregated 0.263 mnt in April and 0.309 mnt in March.

Outlook:

Trade-level prices might come under pressure in the near term and show some descent. Market participants have been anticipating price support from mills in May; however, the latter did not announce any hike. Distributor network participants are observing the recent weakening of market sentiments and are buying cautiously. This is likely to weigh on prices in the near term.

Leave a Reply