- Ample scrap supply weighs on prices amid weak demand

- Trade activity likely to pick up post-holidays

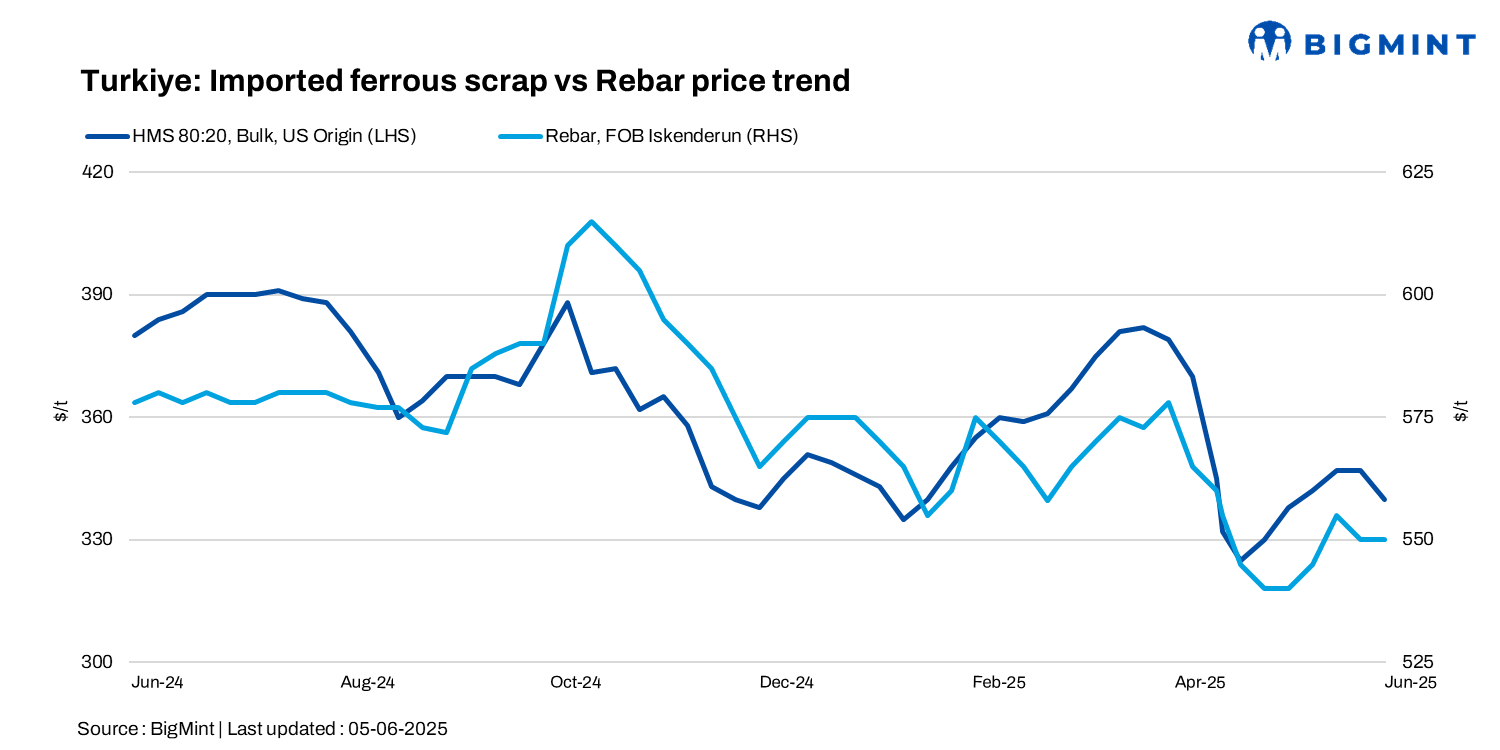

Imported deep-sea ferrous scrap prices in Turkiye declined by $7/t w-o-w to $340/t CFR, as trading slowed amid weak finished steel demand and the approaching Eid al-Adha holiday. Mills have paused bookings, preferring to conserve cash in a high-interest-rate environment and await clearer post-holiday market direction.

While scrap availability remains sufficient, mills still need to secure material for July. They are using the holiday lull to push for better terms. Rebar sales, both domestic and export, remain weak, weighing on scrap demand. However, price declines are being capped by currency volatility and elevated seller costs, particularly from Europe and the US.

BigMint’s price assessments

- US-origin HMS 80:20 bulk scrap stood at $340/t CFR Turkiye, fell by $7/t w-o-w.

- Bulk HMS 80:20 from the US East Coast was at $317/t FOB, fell by $7/t w-o-w.

The Turkish rebar-to-scrap spread stood at $200-210/t, with workable levels for Turkish rebars heard up to $545-550/t FOB.

Approximately 3-4 deep-sea deals were concluded over the past week in the $336-346/t CFR range.

Market commentary

Offers for US/Baltic-origin HMS 80:20 were mostly in the $340-344/t CFR range, with tradable levels around $338-340/t CFR while, EU-origin HMS 80:20 was heard near $335-336/t CFR.

According to a market participant, “No recent deep-sea scrap deals were reported as Turkish mills remained inactive ahead of the Eid holiday, which runs until 10 June. Mills is expected to resume bookings only after the break. The last confirmed deal involved prompt delivery of Stena material from Sweden. Initially heard at $346.5/t CFR, the final reported price was revised to $340.5/t.“

A Turkish mill-side source noted, “Rebar demand is weak, and mills are using the holidays to delay buying and push for lower scrap prices. Some suppliers may eventually be forced to sell if inventories build up.”

A Participants observed that mills are receiving abundant offers, allowing them to remain inactive and avoid counter-bidding. The last confirmed deal was for prompt Europe material from Sweden, initially heard at $346.5/t CFR and later finalised at 340.5/t.

Although mills will need to book more scrap for July, the upcoming holidays give them room to negotiate better terms. With both domestic and export rebar sales remaining sluggish, scrap prices face pressure, especially if selling urgency rises among exporters.

Outlook

The near-term sentiment remains bearish, with mills expected to stay inactive through the holiday week. Scrap prices may face further downside due to weak rebar demand, but support could come from firm US offer prices, limited euro-based scrap flows, and high seller costs. Chinese billet offers at $450/t CFR for August shipment may also add pressure on Turkish longs post-holiday.

![]()

Leave a Reply