- Steel inventories increase, straining scrap demand

- Rising loans lead to liquidity shortfalls

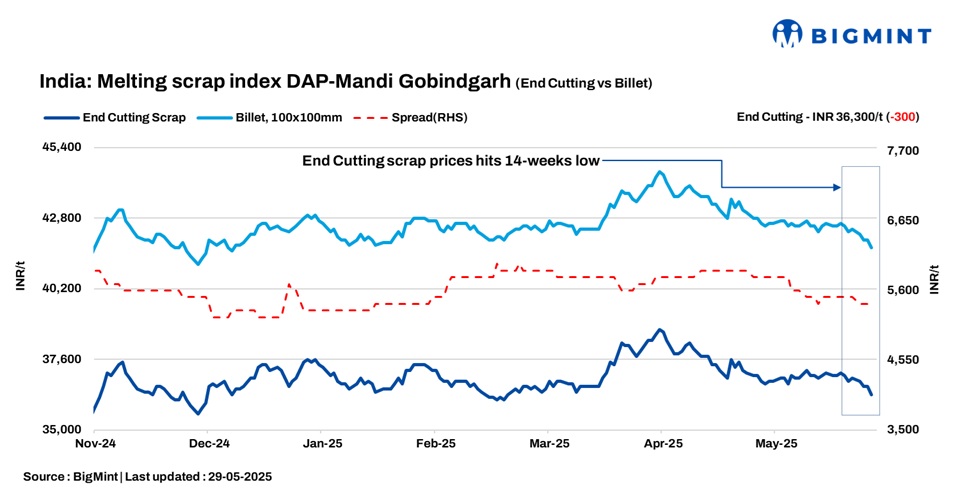

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 300/tonne (t) d-o-d to INR 36,300/t DAP on 29 May 2025. Scrap prices continued to decline to a 14-week low-levels last seen on 22 February 2025. The overall steel market continued to face downward pressure, with demand weakening. Additionally, ongoing labour shortages in the Mandi Gobindgarh and Ludhiana regions are disrupting the routine operations of steel mills, affecting production efficiency and timely dispatches.

A mill owner informed BigMint,”In the Mandi Gobindgarh steel market, trade remains dull, with limited movement in both semi-finished and finished steel. Inventory pressure is increasing day by day, adding to the strain on traders and mills. Raw material auctions continue to see weak activity, with prices failing to gain momentum. Adding to concerns, rising loans are tightening financial conditions for steelmakers, raising risk levels across the supply chain. The near-term outlook stays cautious, with market players closely watching for demand revival.”

Raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh remained stable d-o-d at INR 29,800/t, while in Ludhiana, steel-grade pig iron tags dipped by INR 50/t to INR 35,900/t DAP.

Steel market trends

Steel ingot prices in Mandi Gobindgarh dropped by INR 200/t d-o-d to INR 41,700/t DAP, amid weak demand. Similarly, semi-finished steel prices in other regions declined by INR 100/t to INR 350/t, indicating continued sluggish market sentiment.

Rebar prices in Mandi fell by INR 200/t d-o-d to INR 46,900/t exw. HR strip (patra) prices remained unchanged d-o-d at INR 43,900/t exw.

Overview of Hyderabad market

The Hyderabad steel market continued to face pressure, as demand remained subdued across key segments. Rebars saw limited trade activity, with only some movement in the retail market. No major government project work has been announced recently, adding to the market’s sluggishness. Billet trade was stagnant due to a lack of support from finished steel demand. Sponge iron stocks piled up, as low demand and increased inter-market selling kept material movement slow. Overall, market sentiment was weak, with no immediate signs of recovery.

Rebar (Fe500) prices fell by INR 500/t d-o-d to INR 44,500/t exw, reflecting weak demand. Billet prices remained steady d-o-d at INR 40,000/t exw, while sponge iron(PDRI) tags declined by INR 200/t to INR 25,600/t exw.

Upcoming auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,300-5,600/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $345-350/t, which equates to approximately INR 32,090/t (including freight). Today, local HMS (80:20) prices in Mumbai remained stable d-o-d at INR 32,500/t DAP. Indicative prices of shredded from Europe stood at $365-$370/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,350/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply